1 Money—What Is It?

Using existing money is simple. Creating money? That’s a different story. This article will explain how money is made and how its creation influences its use and misuse.

First, let’s define money. Money is a medium of exchange. The key word is “medium.” If I have eggs and you have bacon, we might trade a few eggs for several slices of bacon directly, without a medium. This direct trade is “immediate”—no intermediary involved.

But when money enters the picture, it acts as a medium or intermediary, facilitating the exchange. Money often serves as an instrumental good, a tool to get the real goods we want. I can enjoy a $20 steak (a real good), but a $20 bill (an instrumental good) is only valuable for what it can buy, like steaks.

The line between real and instrumental goods isn’t always clear. During WWII, prisoners used cigarettes as money to buy items like bread and butter, making them instrumental goods. But those same cigarettes could also be smoked for pleasure, turning them into real goods. Gold and silver have a similar dual role. As coins, they’re instrumental goods. But as metals for jewelry, they’re real goods.

2 Becoming Money

Defining money as a medium of exchange tells us what money is, but how does something become that medium? This isn’t just about creating money, but understanding why people choose to use something as money. Take cigarettes in WWII POW camps. Why cigarettes and not razor blades or something else? The US Medical Research Centre details what was in American POW relief packages, giving us clues about what prisoners had to trade and what could have been money.

Cigarettes became the prime currency among WWII prisoners. Why? One might think it’s about convenience. Cigarettes are easy to trade, come in handy units, are packable, and light. All good qualities for money. But these features alone weren’t essential for something to serve as money in the camps.

The key was the widespread agreement among prisoners to use cigarettes as money. How did they come to this agreement? A medium of exchange makes trade easier, even in a prison economy. Once cigarettes were seen as a convenient form, the prisoners naturally agreed to use them as money. Other items could have worked just as well. What becomes money in any situation depends on the circumstances. It could have been different.

The agreement that transforms an ordinary item into money is more mysterious than any alchemical change. Jacob Goldstein’s 2020 book, titled simply Money, captures this truth. The subtitle reads, The True Story of a Made-Up Thing. Money is “made up” like the rules of a game invented by children. There’s nothing in nature that makes any item serve as money. We, through social agreement, turn these items into currency.

Goldstein’s view is correct but needs elaboration. Philosopher John Searle expands on this in The Construction of Social Reality. Social realities include marriage, games, property, governments, law, and money. These arise through what Searle calls “collective intentionality.” This is the agreement within a group that brings social realities into existence: we collectively intend for something to serve a social purpose.

Social realities are objective because our collective intentionality makes them so. Goldstein’s view might suggest money is a fiction, but it’s a shared fiction we treat as real. Money as a social reality is more insightful than as a “made-up thing.” It’s fully objective, not a matter of personal taste. The creation of money is an act of collective intention that establishes a social reality for exchange. This is how money is created. The types of money and their justification are where it gets interesting. With the right agreement, anything could be money. But few things do end up counting as such. We’ll explore these types and the features we value in money next.

3 What We Want of Money

Money is any medium of exchange. For it to be useful, it needs certain features. These features aren’t strictly necessary, but without them, money won’t last long. It will be replaced by newer forms that have these desirable traits.

The history of money is filled with failures. Many forms of money have come and gone. Creators of money learn from these failures and try to build safeguards into their currency. Money usually has a kind of inertia; people are reluctant to abandon it unless it becomes worthless, like during hyperinflation.

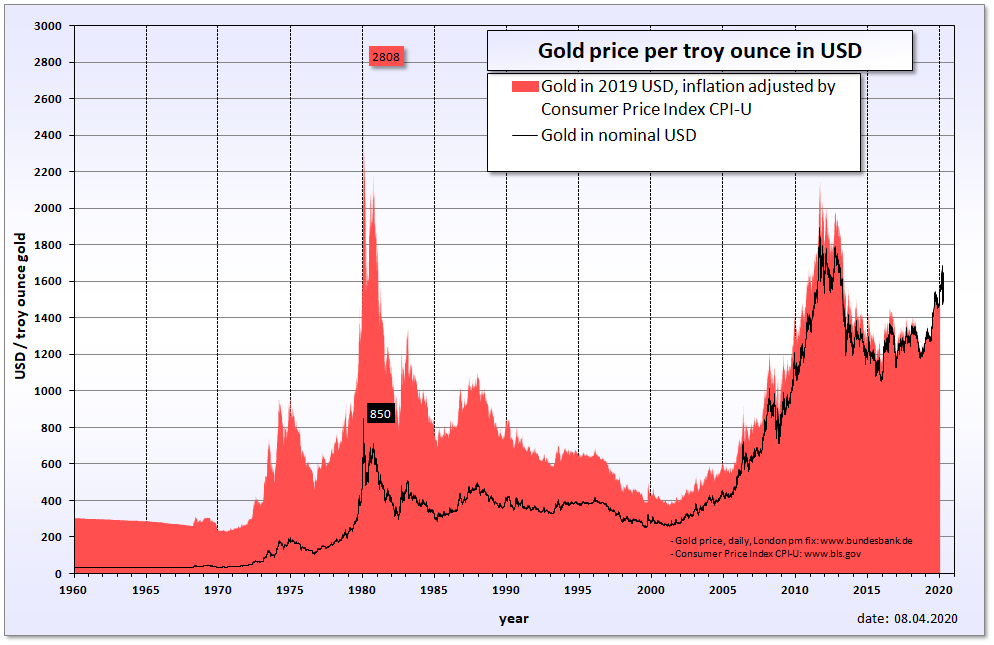

Two key features of money are being a unit of account and a store of value. As a unit of account, money must be countable and divisible. It should be fungible, meaning one unit is interchangeable with another. As a store of value, money should hold its purchasing power over time, unaffected by inflation or deflation. Inflation reduces money’s value, while deflation can discourage spending. Both can destabilize the economy, harming buyers, sellers, borrowers, and lenders. Gold, often seen as stable, can be highly volatile, as shown by its price fluctuations between 1980 and 1982. This instability proves why stable money is crucial for a healthy economy.

There’s a camp of monetary theorists who believe gold is the ideal money. They argue that the best move for a nation’s currency is to return to the gold standard. Perhaps if everyone agreed on gold’s supremacy, the sort of inflation described earlier wouldn’t happen. In that scenario, the U.S. dollar, a fiat currency detached from gold, wouldn’t muddy the true value of gold.

But even in a world where gold is money, it has faced inflation. In 16th century Spain, the influx of New World gold caused prices to rise by 300 percent over the century. Contrast this with the 2,500 percent inflation in the hundred years following the Federal Reserve’s establishment in 1913, under both gold standards and fiat currency.

“Fiat” comes from the Latin for “let there be,” echoing Genesis where God creates by declaration. Fiat money, then, is money because an authority declares it so. Its existence is in its proclamation. My aim here isn’t to argue for or against gold, but to highlight that we seek a store of value in money, one that holds its purchasing power steady. Gold has struggled with this, as have all currencies over time.

Milton Friedman rightly said, “Inflation is always and everywhere a monetary phenomenon,” resulting from money growing faster than output. Deflation, conversely, stems from too little money for the output. The challenge is to balance money creation: enough to prevent deflation, but not so much to cause inflation. The Goldilocks principle of “just right” is tough to achieve.

In our age of fiat currencies, money can be created from nothing. The risk, then, is excess. Thus, an essential feature of money is its scarcity, to preserve its value. Digital currencies, for instance, must avoid the double-spend problem, where the same unit is used in multiple transactions. Physical money avoids this by existing in one place at a time. We’ll explore other desirable features of money as they come up. Next, we’ll look at specific types of money.

4 Money as Something Physical

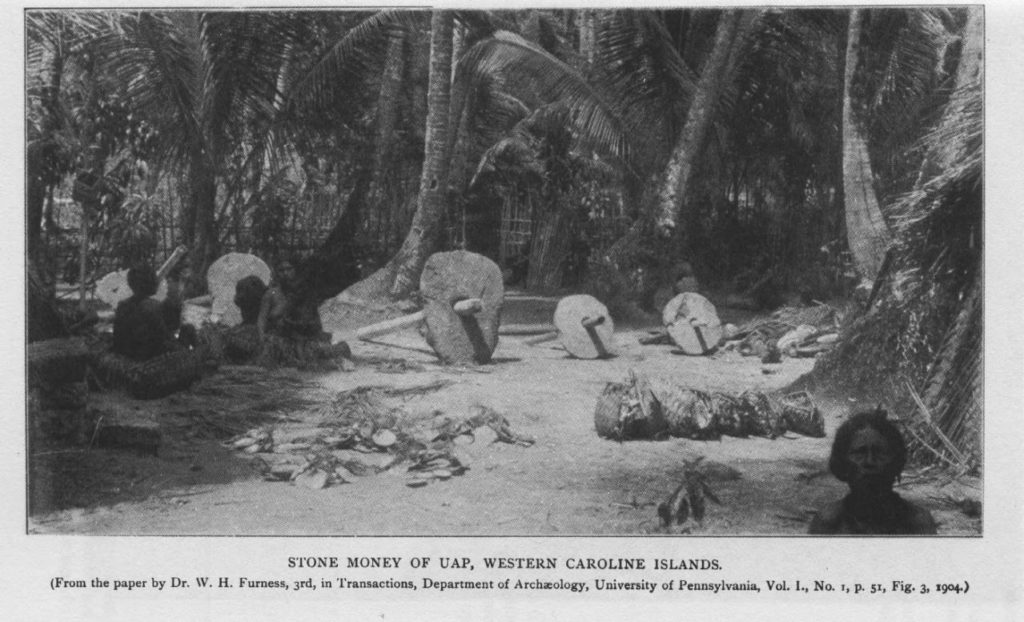

Physical money has taken many forms. Cowry shells served as currency around the Indian Ocean. Cocoa bags full of beans were money to the Aztecs. The Micronesian Yap islanders used circular limestone discs, called fei, as money. These stones were so heavy they couldn’t be moved easily. One even ended up at the bottom of the sea before reaching the island. Yet, the islanders still used it as money, keeping track of its ownership.

The Yap islanders could transfer ownership of these fei without moving them. By simply agreeing that so-and-so now owned a particular fei, they could facilitate transactions. These stones varied so much in size that they couldn’t serve as a unit of account. But they were still money because they mediated exchange.

Money has always been about more than physical transfer. It’s about the agreement and trust in the value assigned. From shells to stones, the form doesn’t matter as much as the collective belief in its worth.

Paul Einzig, in his classic Primitive Money: Its Ethnological, Historical and Economic Aspects, recounts the many forms physical money has taken. Here is a partial list of the types of physical money he considers, showing how primal the urge in humans is to create money:

- Mat and bark cloth money in Samoa

- Whales’ teeth as currency in Fiji

- Bead currency in Palau

- Feather money in Santa Cruz (Solomon Islands)

- Boar tusks in New Guinea

- Rice currency in the Philippines

- Drum currency in Alor (Indonesia)

- Beeswax as money in Borneo (Indonesia)

- Gambling counters as money in Thailand

- Tea brick currency in Mongolia

- Coconut standard on the Nicobar Islands (India)

- Grain medium of exchange in India

- Reindeer in eastern Russia

- Iron currency in Sudan

- Salt money in Ethiopia

- Livestock standard in Kenya

- Calico currency in Zambia

- Gold dust currency in Ghana

- Fur currency in Alaska

- Maize money in Guatemala

- Sugar money in Barbados

- Tobacco money in Bermuda

From this list, it becomes clear that people create money from what they have on hand, regardless of the size of their group. The island of Yap, with just over 10,000 inhabitants, is a small place but had its own currency. You don’t need to be a country to have a currency. Local moneys, existing in small communities and independent of government control, even exist in the U.S. The idea that money must be the creation of the government, as promoted by monetary theorist Georg Friedrich Knapp in his influential 1905 book The State Theory of Money, goes too far. Money can be the creation of the state, but it need not be.

4.1 Commodity Money

All the physical moneys described above are examples of commodity money. These moneys have intrinsic value because they are reasonably scarce. They are not like air and water, which come in unlimited supplies. As commodities, they have built-in limitations on proliferation. Their scarcity correlates with their value in exchange.

With paper money, the value is supposed to exceed the cost of the paper and ink. This makes counterfeiting a constant temptation. Commodity money, on the other hand, faces issues of debasement or misrepresentation. If salt were money, we might debase it by adding cheaper substances to it. If sea shells are money, we might shape wood or plastic to look like them, misrepresenting our holdings.

Commodity money can’t really be counterfeited like paper money. If a counterfeit is indistinguishable from the real thing, it is effectively the real thing. With commodity money, it’s always possible to determine if it meets the set standard. Gold, for instance, can be tested for purity with a touchstone. Even privately minted gold coins, if indistinguishable from government-issued ones, aren’t truly counterfeit. They are just as legitimate. The biggest challenge for commodity money in history has been debasement. Roman emperors debased their silver coins over time, leading to inflation and economic instability. Constantine understood this and minted the pure gold solidus, which remained stable for 700 years.

4.2 Redeemable Paper Money

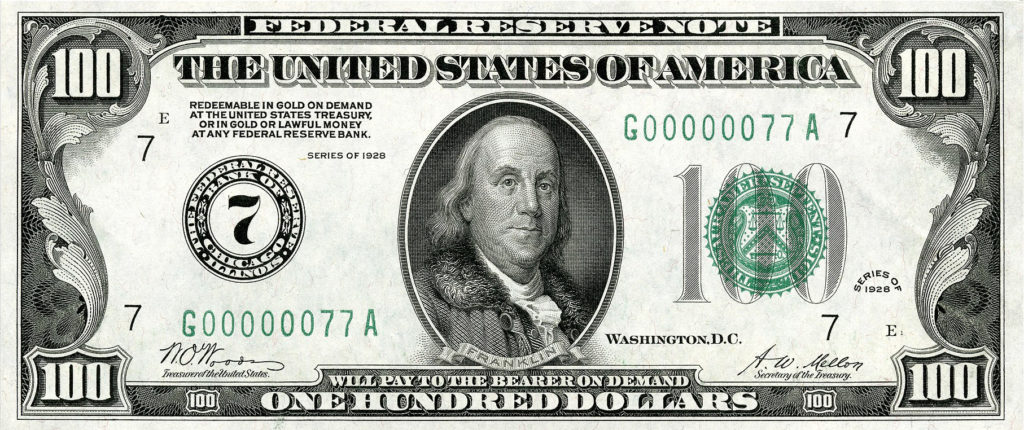

When we think of paper money, we think of fiat money, where the government prints pieces of paper to be used as money. But this isn’t the only way. Paper money doesn’t have to be fiat if it’s backed by something of intrinsic value, like gold. Consider these two $100 bills:

The first $100 bill states, “redeemable in gold on demand at the United States Treasury or in gold or lawful money at any Federal Reserve Bank.” This bill stands in for gold commodity money. The second $100 bill simply states, “this note is legal tender for all debts, public and private,” meaning people in the U.S. must accept it in payment, even though it isn’t backed by anything of intrinsic value.

In 1928, the U.S. dollar was still backed by gold. In 1933, Franklin Roosevelt made the dollar unredeemable in gold and had all U.S. citizens turn in their gold. The government paid $20.62 an ounce, only to raise the price to $35 an ounce, devaluing the dollar and causing inflation. For years, countries could still redeem dollars in gold, but individuals could not. With France redeeming many U.S. dollars for gold around 1970, Richard Nixon closed the “gold window” in 1971, severing the dollar’s last ties to gold. The dollar became a pure fiat currency.

Redeemable paper money’s value should match what it can be redeemed for. Governments or monetary authorities printing redeemable paper money should be able to circulate it directly, buying things as they would with the commodity itself. Transactions that once used $20 gold pieces could now use redeemable paper money. The question then is how much of the backing commodity, like gold, is on hand. Fully backed paper money is safe, as every note can be redeemed. A government printing money with 100 percent backing can spend it freely.

But what if the backing is less than 100 percent? If it’s 25 percent backed, the government effectively quadruples its purchasing power. This feels like a free lunch, where someone ends up holding the bag. A concern with less than 100 percent backing is a “run on redemption,” leaving some people with unredeemed notes. Yet, partial backing is common. The Federal Reserve Act of 1913 required only 40 percent backing in gold. People don’t typically redeem the entire money supply at once, making paper money convenient.

Even with partial backing, there’s a risk of running out of the commodity, but governments often provide assurances to secure more if needed. However, if the backing percentage is too low, the currency becomes suspect. There’s no magic number, but the concern remains that partially backed paper currencies offer a free lunch, much like fiat currencies. They can be seen as a hybrid of redeemable and fiat currencies. Good faith in the monetary authority to guarantee redemption adds value, as does the government’s willingness to accept the currency for taxes.

Though the U.S. dollar is no longer backed by gold, it’s interesting to consider what percentage of the dollar would be backed by gold today. In January 2021, there were just over $2 trillion in paper and coin money. The U.S. government’s gold reserve totaled 258,641,878.085 troy ounces, valued at around $475 billion at $1,850 per ounce, or just under 25 percent of total paper and coin money. Including checking and savings deposits, the total money supply was about $20 trillion, making the gold backing of the dollar, if it were redeemable, around 2 to 2.5 percent.

4.3 Fiat Paper Money

Fiat paper money, though unbacked by any commodity, is never just paper with ink. It comes from a monetary authority, usually the government or a central bank. Issuing this money isn’t just about printing it. It’s about getting it into circulation with incentives for people to use it, like paying taxes and making it required for payments. Safeguards against counterfeiting and hyperinflation are also crucial.

Creating fiat money isn’t as simple as firing up a printing press. If it were, it would be no different from Monopoly money. But our fiat money is “legal tender for all debts, public and private,” by law. This makes it real money, not play money.

Most government-sponsored fiat money today isn’t printed. It’s issued as electronic bank deposits. We’ll explore the creation of fiat money in general, including both paper notes and electronic deposits, in the next section.

5 Money as Credit

A myth persists in economics textbooks that money arose from the limitations of barter. If Alice has eggs and Bob has bacon, they can trade only if there’s a “double coincidence of wants.” Alice must want Bob’s bacon, and Bob must want Alice’s eggs, in the right amounts and at the right rate of exchange. Textbooks tell us money arose to solve this problem, facilitating transactions where Alice wants what Bob has, but Bob doesn’t want what Alice has, or they can’t agree on the terms.

David Graeber, in his book Debt, and Felix Martin, in his book Money, argue that this story of barter evolving into money is a fabrication with no basis in history or anthropology. Barter has always been limited and often ritualized. What facilitated exchange were systems of credit, where debts and obligations were carefully tracked.

Some of the first human writing, 5,000 years ago in Mesopotamia, consists of receipts and invoices. These ancient records are not myth or poetry but accounting ledgers, indicating a system of credit. Credit signifies a relationship between a creditor, who gives something of value, and a debtor, who promises to repay it in some agreed form. An IOU can simply read, “I, Alice, owe you, Bob, 30 shekels of silver.” Notarized by Alice’s signature or the city elders, it becomes binding. A deadline for repayment is often set by convention.

Alice’s IOU mediates the exchange of Bob’s plot of land to Alice. Is this IOU money? By our definition, yes. It serves as a medium of exchange. The use of credit as a medium of exchange has a long history. Debt becomes money. One might argue that the debt itself isn’t the money, but rather the item offered in repayment. This argument doesn’t hold up.

Credit is indeed a form of money. Consider Alice making her IOU to Bob negotiable: “I, Alice, owe to the holder of this note 30 shekels of silver.” This note, if trusted, can circulate among people, trading for goods worth 30 shekels, without any shekels changing hands.

Credit money carries risks because it’s based on promises, and promises can be broken. Societies form legal structures to enforce debt repayment. Money is credit.

Does credit money presuppose real money for the underlying debt? True, credit money depends on some basic form of value. Yet, this “real money” need never appear in a transaction.

Imagine Alice, Bob, and Carol: Alice gives Bob a negotiable IOU for 30 shekels. Bob gives Carol a similar IOU. Carol gives Alice a negotiable IOU for 30 shekels. If Alice gets 30 shekels, she can pay Carol, who pays Bob, who pays Alice. This clears the debts, and Alice has her 30 shekels again.

But all three debts could be cleared by canceling each other, without any shekels changing hands. In a system of credit and clearing, very little real money is needed. Indeed, increasing the velocity of money can vastly reduce the need for it.

6 How Money Multiplies

Credit in the form of negotiable IOUs is money. Does credit create money, then? It’s one way to make more money from existing money. But credit money still depends on some more basic form of money, even if it’s just a single penny. We still need to explain the existence of that penny or whatever form of money we start with.

Credit money expands existing money. The inventor of a widget creates it, but the one who makes copies multiplies it. Both are part of the creation process. Think of a flock of sheep. The initial pair is creation; the rest of the flock is multiplication. Existing money can be multiplied, and credit money is one way. Another is through bank loans.

When money is deposited in a bank, the bank can loan out most of it. This is fractional reserve banking. The reserve rate is the fraction the bank must keep. For U.S. banks with $125 million in assets, the rate was 10 percent until recently. This rate determines the money multiplier. A 10 percent reserve rate means a multiplier of 10. A 5 percent rate means a multiplier of 20.

On March 26, 2020, the Fed lowered the reserve requirement to zero percent. With no reserve rate, fractional reserve banking becomes money creation, not just multiplication. Imagine a non-zero reserve rate. Alice has $10,000 in cash and wants to buy Bob’s $100,000 BMW. She deposits $10,000 as a down payment. Through fractional reserve banking, the bank can loan Alice 90 percent of her deposit.

With $10,000 deposited, the bank can loan $9,000. Alice deposits that, giving her $19,000. The bank can now loan 90 percent of that, or $8,100. Alice deposits that too. This cycle continues until Alice has $100,000 in her account and a $90,000 loan. She buys Bob’s BMW, has a zero balance, and a $90,000 loan to repay with interest.

Learning about fractional reserve banking, I thought, “How do I become a bank?” Banks have an exorbitant privilege, extended by the state. They’re highly regulated. I can’t be my own bank to multiply my cash. Through fractional reserve banking, Alice’s $10,000 becomes $100,000. She buys the BMW but owes $90,000. If she defaults, the bank owns the car. It feels surreal.

The unreality of fractional reserve banking lies in money appearing in two places at once on an accounting ledger. Physical objects can’t do this. When Alice deposits $10,000, and the bank loans $9,000, money multiplies. Alice can claim her $10,000, but the bank can only claim the $9,000 loan. If Alice withdraws more than $1,000 before the loan is repaid, the bank can’t cover her deposit.

This scheme depends on depositors not withdrawing too much at once. If they do, the system collapses. Money multiplication through loans feels like a Ponzi scheme. But as long as loans are repaid, the system works, or seems to. Our banking system relies on this multiplier effect. Much of the money we use comes from it.

7 How Central Banks Create Money

We saw how banks have the exorbitant privilege of fractional reserve lending. But if that privilege is exorbitant, the power of central banks to create money from nothing is even greater. Ordinary banks start with pre-existing money. They can only lend what’s been deposited. Central banks, however, can lend without prior deposits.

When an ordinary bank credits an account, it transfers or loans from another account. A central bank, though, can credit an account without accessing another. Deposits by ordinary banks depend on existing deposits. Central banks can create deposits without prior funds. This is money from nothing.

If this sounds too good to be true, don’t take my word for it. The Boston Federal Reserve’s 1984 booklet “Putting It Simply” explains: “When you or I write a check, there must be sufficient funds in our account to cover the check, but when the Federal Reserve writes a check, there is no bank deposit on which that check is drawn. When the Federal Reserve writes a check, it is creating money.”

7.1 How the Fed Buys Securities to Create Money

Central banks follow a certain logic in creating money. This logic is the same whether the money consists of paper notes, ledger entries, or digital information. For simplicity, let’s focus on the U.S. central bank, the Federal Reserve, or Fed. This logic applies to most central banks.

The only exception is when a central bank loses its independence and creates money with no limits on government spending. This leads to runaway inflation, like we see in Venezuela. It could happen in America if Modern Monetary Theory (MMT) gains traction.

The key restriction preventing unlimited money creation is that every dollar (or peso, yuan, euro, etc.) must be a loan that must be repaid. Failure to repay would be a default. By making new money take the form of loans, central banks impose discipline, further controlled by varying interest rates.

Governments can be tempted to create and spend money instantly, especially during crises. To avoid this, there’s a fiscal-monetary divide. Fiscal concerns what money is spent on, monetary concerns its creation. The central bank (the Fed) creates money, but doesn’t spend it. That’s the job of the U.S. Treasury.

Here’s how it works. Taxes often don’t cover all government expenses, leading to a deficit. Congress and the president agree on the need for more funds, and the U.S. Treasury issues bonds (T-bills, T-notes, T-bonds). The Federal Reserve Act prevents the Fed from buying treasuries directly from the government. Instead, the Treasury sells them at auctions to large banks, the primary dealers.

When the Fed buys treasuries, it does so on the open market. The Fed credits the account of the bank or party selling the treasuries, not the U.S. Treasury. This creates a deposit without needing to debit another deposit. In this way, the Fed creates money.

These bonds become assets on the Fed’s balance sheet. As liabilities of the U.S. Treasury, the Treasury pays interest on these bonds and repays the principal at maturity. Issuing treasuries creates money; repaying them destroys it. Money is loaned into existence and repaid out of existence.

In sum, when the Fed buys securities like treasuries, it creates new deposits, thus creating money. Whether by printing paper money, writing credits in accounts, or authorizing digital transactions, the logic of money creation remains the same.

7.2 Modern Monetary Theory (MMT)

It may seem like a hassle for central banks to create fiat money by loaning it into existence, but what is the alternative? There must be a limit on creating money. Without it, hyperinflation looms large. I’m not sure if loaning money into existence is the best way. But I’m certain that without limits, as proposed by Modern Monetary Theory (MMT), we are on an economically unsound path.

MMT suggests that the government can simply create and spend the money it needs, without needing to tax the people initially or to loan money into existence as we do now. When this freedom to create and spend money overheats the money supply, MMT suggests that the government can cool it down by imposing taxes. Taxes would then become a correction to an overheated money supply.

It’s remarkable to see this proposal taken seriously. History shows that governments under stress, especially during wars, will do anything to increase their spending. Runaway inflation is a clear danger with MMT. By the time taxes are imposed to remove excess money, the damage from inflation will already be done.

MMT also carries an ideological charge, providing a way to advance socialist policies not by confiscating production means but by buying them, as the government prints as much money as it needs. MMT is not ideologically neutral: capitalism doesn’t stand a chance since the public sector, with unlimited funds, can overrun the private sector.

MMT advocates might argue that I misrepresent it and that safeguards can prevent undue competition with the private sector. But without the fiscal-monetary divide to slow money creation and discipline spending, the private sector should worry about MMT-driven policies. The private sector should already be worried. According to the Cato Institute’s Downsizing Government website, since the 1990s, federal workers have enjoyed faster compensation growth than private-sector workers. In 2018, federal workers earned 80 percent more on average than private-sector workers. And federal workers earned 47 percent more on average than state and local government workers. The federal government has become an elite island of secure and high-paid employment separated from the ocean of average Americans competing in the economy.

With MMT in control, this trend would not only continue but worsen. Private sector workers might demand that the government supplement their income to match that of federal workers, given that the government can create and spend money freely. All such payments would have strings attached, with the public sector eventually capturing the private sector. This encroachment is already visible in health care. MMT would universalize this trend.

MMT economists claim that the U.S. can create unlimited money because its debts are in U.S. dollars, and it can never default. MMT distinguishes the U.S., which owes debts in its own currency, from countries that owe debts in foreign currencies. But guarantees against default are not guarantees against runaway inflation. It’s the inflation that will kill you, even if the defaults don’t.

7.3 Central Bank Digital Currency (CBDC)

When a bank makes a deposit, the amount is simply added to the account. If the U.S. Treasury gives me a $2,000 tax refund and I have $3,000 in my account, it looks like this:

- $3,000 [previous total]

- $2,000 [U.S. Treasury tax refund]

- $5,000 [new total]

When the Fed created the money for the U.S. Treasury’s account to pay my tax refund, it just added a number to the Treasury’s account.

But what if the Fed added serial numbers to these amounts, like those on paper dollars? These numbers would identify our digital currency just as serial numbers identify physical cash.

With each deposit, there would be not just a number but a unique serial number. These digital serial numbers would trace the currency from the Fed, through the Treasury, and across the banking system.

We don’t need physical serial numbers. Tracking pixels could follow each unit of money from its creation by the Fed. These pixels would allow a complete history of any transaction. Users wouldn’t see these serial numbers, but the banks would. In the digital age, these could be called “tracking numbers.”

This is central bank digital currency (CBDC). According to Bloomberg, the Federal Reserve, with MIT, plans to roll out a digital currency called “Fedcoin” in 2021. China is ahead with its digital yuan, already piloting it in several cities, aiming for the 2022 Winter Olympics. Josh Lipsky of the Atlantic Council asks what tensions might arise if American athletes must use a currency the Chinese government can track.

The point of CBDC is to create money with a tracking device. Why do this? Money is a medium of exchange. If I wire money from my bank to someone else’s, the banks act as intermediaries. But if I hand over cash, there’s no intermediary, making the exchange private.

Digital money always requires a third party, making “digital cash” an oxymoron. Physical cash eliminates intermediaries. Kenneth Rogoff, a Harvard economist, wrote The Curse of Cash, arguing that cash enables crime and spreads disease. But I’ll take my chances with cash over a government that tracks every transaction.

Imagine the slippery slope of such tracking. In a cashless society, privacy ends. Tracking could lead to controlling behavior. If I buy a Big Mac, I might get a pop-up warning about my health. Next, my bank might refuse the transaction, or the government might block McDonald’s from receiving payment.

Governments might argue they act in our best interest. But what if they shift to a punitive role? Late on alimony? Your flight is blocked. Or the government pays your alimony from your account without consent. This power is more dangerous than criminals using cash.

Lord Acton said, “Power corrupts; absolute power corrupts absolutely.” A government with control over all financial transactions has absolute power. This is more concerning than criminals using cash, who will find ways around CBDC, like with cryptocurrencies. But government tracking will compromise individual freedom, a high price for a cashless society.

One more benefit of cash is limiting government confiscation. Digital money resides on servers, making it subject to government control. Banks can impose negative interest rates, reducing deposits over time. Imagine a bank advertising: “Deposit $100, and get $98 back in a year.”

With cash, negative interest rates are a non-starter. You’d keep $100 under your mattress instead of depositing it. Cash protects against the erosion of your savings by negative rates and keeps money out of government reach.

Cash is incompatible with CBDC, which requires a monopoly on all money to be effective.

8 Cryptocurrencies

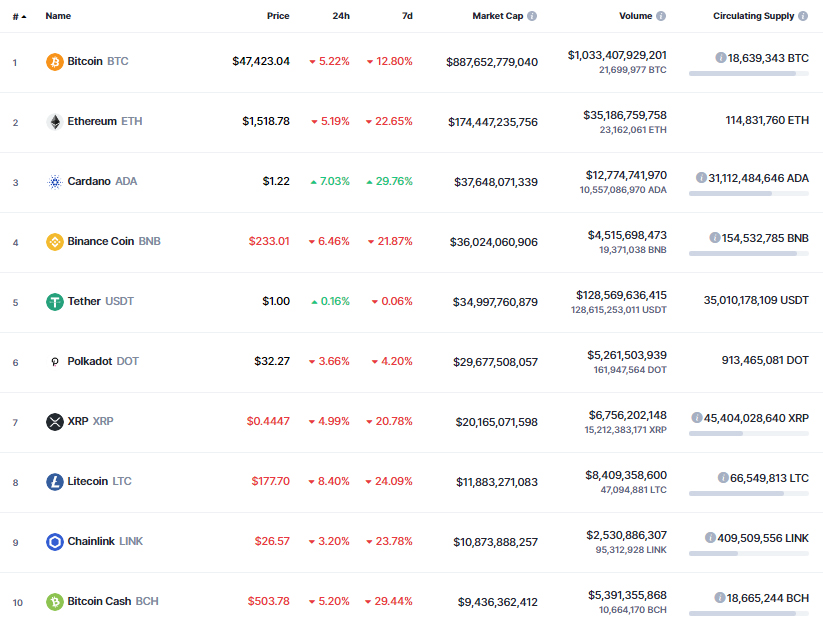

The creation of cryptocurrencies is our final topic. The screenshot above, taken today, 26 February 2021, from CoinMarketCap.com, shows the 10 most highly capitalized cryptocurrencies. Bitcoin dominates the list. Around that time, it came down from an all-time high of over $50,000 per bitcoin, putting its total market value near $1 trillion. In early June 2024 at the time of this update, the value per bitcoin is around $70,000 and the total market value is approaching $1.4 trillion.

Is this a speculative bubble? Reading Charles Mackay’s Extraordinary Popular Delusions and the Madness of Crowds, one might think Bitcoin is the latest public mania, like the tulip mania in 17th-century Holland. Bitcoin and other cryptocurrencies certainly have a speculative feel, but there’s more going on. Bitcoin has been used for exchange in countries like Argentina, where the national currency is unstable. It thrives in the $700 billion plus remittances market, where money needs seamless transfer abroad. It has also been used to buy illegal drugs on darknet markets like the defunct Silk Road.

Given the push among economists to eliminate cash, as outlined earlier, cryptocurrencies might be the next best thing to cash, perhaps even better. Like cash, cryptocurrencies promise to stay out of reach from meddling authorities. It’s no surprise that some of the biggest advocates of cryptocurrencies are deeply skeptical of government control over money. Cryptocurrencies have a lasting appeal, especially to those with an anti-Big Brother streak, and this appeal will likely keep them alive and valuable for some time. How valuable is another matter.

So, what is a cryptocurrency? Cryptocurrencies are digital currencies. Any digital currency uses cryptographic methods. Information packets sent across the internet for transactions with digital currencies must be encrypted to prevent eavesdropping. But merely using cryptographic methods doesn’t make a cryptocurrency. Nor does public-key cryptography alone.

Cryptocurrencies depend on public-key cryptography. The owner of a currency item knows a private cryptographic key, which decrypts messages sent via the public key and authorizes transfers of funds. But using cryptographic tokens to transfer ordinary money like U.S. dollars is not a cryptocurrency.

A cryptocurrency is a self-contained, entirely digital currency protected by cryptographic methods, achieving value without aid from other currencies. Bitcoin and other cryptocurrencies have reached this status. Their market capitalization shows people are willing to spend dollars to buy them, not because they can be redeemed for dollars by some central authority.

Bitcoin, proposed by the pseudonymous Satoshi Nakamoto in 2008, was a huge leap in cryptocurrencies’ power and appeal. Its blockchain gave a complete and unalterable record of all bitcoin transactions. Its peer-to-peer protocol eliminated the need for trusted third parties. Its consensus mechanism using proof of work to generate new bitcoins incentivized people to use the currency and maintain its network.

Bitcoin fulfilled various desiderata for digital currencies: privacy, anonymity, immunity to double-spending, and nonrepudiation. With Bitcoin, prior cryptocurrencies using trusted third parties fell away. Newer cryptocurrencies have built on Bitcoin, modifying some features but not its basic blockchain/peer-to-peer/consensus mechanism infrastructure.

Cryptocurrencies use two consensus mechanisms to create new currency: proof of work (PoW) and proof of stake (PoS). Bitcoin, with a market cap of close to $1.4 trillion today, uses proof of work. Among PoS cryptocurrencies, Ethereum is the highest capitalized (it transitioned from PoW to PoS in 2022), sitting at roughly $450 billion currently.

A consensus mechanism creates money within a cryptocurrency in a clear, defined way. On a peer-to-peer network, users eligible to receive new currency fulfill certain requirements, gaining currency either through certainty or randomization, after a block of trading.

For PoW cryptocurrencies, the user who performs a difficult computational task gets rewarded with new currency. In Bitcoin’s case, this is a competition where only one user gets rewarded after each transaction block. This reward means the network agrees that new currency is added to the user’s account.

PoS works differently. The user’s ownership and interactions with the network over time determine new currency receipt. In both cases, new currency creation is built into the cryptocurrency’s programming from the start.

In conclusion, this article has covered how money has been created from ancient times to now. While the discussion on cryptocurrencies has been brief, I delve deeper into the creation of money within cryptocurrencies, especially PoW and PoS mechanisms, in another article.

References (in order of appearance)

Jacob Goldstein, Money: The True Story of a Made-Up Thing (New York: Hachette, 2020).

John R. Searle, The Construction of Social Reality (New York: Free Press, 1995). Searle followed up this book with Making the Social World: The Structure of Human Civilization (Oxford: Oxford University Press, 2010).

Hyperinflation is the worst type of monetary failure. The link here is to an infographic showing 152 such failures.

Click on “all data” at GoldPrice.org to see how gold has varied sharply in price over the last 50 years.

Milton Friedman, The Counter-Revolution in Monetary Theory (London: Institute of Economic Affairs, 1970), p. 24.

Paul Einzig, Primitive Money: Its Ethnological, Historical and Economic Aspects, 2nd edition (Oxford: Pergamon, 1966).

Peter North, Local Money: How to Make It Happen in Your Community (Totnes, Devon: Transition Books, 2010).

Georg Friedrich Knapp, The State Theory of Money, translated from the 1905 German edition (London: Macmillan, 1924).

David Graeber, Debt: The First 5,000 Years, updated expanded edition (London: Melville House, 2014) and Felix Martin, Money: The Unauthorized Biography — From Coinage to Cryptocurrencies (New York: Knopf, 2013).

Harry Markopolos, No One Would Listen: A True Financial Thriller (Hoboken, N.J.: Wiley, 2010).

Kenneth Rogoff, The Curse of Cash: How Large-Denomination Bills Aid Crime and Tax Evasion and Constrain Monetary Policy (Princeton: Princeton University Press, 2016).

Richard H. Thaler and Cass R. Sunstein, Nudge: Improving Decisions About Health, Wealth, and Happiness (New York: Penguin, 2008).

Image Notes

[top] Cover image is self-explanatory and comes from two images, one signifying Bitcoin, the other Michelangelo’s creation from the Sistine Chapel, Wikimedia Creative Commons.

[sec 2] Image of alchemist is from a painting by David Tenier (1610-1690), Wikimedia Creative Commons.

[sec 3] Gold prices from 1960 to 2020, both nominal and CPI adjusted, Wikipedia.

[sec 4] Image of gold coins from 1st Century under Vima Kadphises, Wikimedia Creative Commons.

[sec 4] Image of fei taken from Wikipedia.

[sec 7] Photo of Federal Reserve headquarters, taken from Wikipedia.

[sec 8] Screenshot from the homepage of CoinMarketCap.com.