A personal loan is an unsecured loan that you promise to pay back within a certain amount of time with monthly installments. In return, the lender gives you a fixed rate of interest along with a set time period for repayment. Personal loans come with a higher rate of interest than other sources of funding, but are usually lower than credit cards. They’re used to pay for home improvement projects, consolidate credit cards, finance an important personal event, or fund a big purchase. A borrower’s credit score determines the maximum amount a lender will offer along with the final interest rate. You need to be mindful about the fact that taking out a personal loan is adding to your debt load, but if you engage in good debt management practices, you’ll find a personal loan is a useful financial tool.

Personal Loans 101

People frequently ask “are personal loans bad?” when the truth is, a personal loan is neither good nor bad. It’s a means to an end when you need money, and you don’t have funds available to you. A credit card can be used, but the cost of using the money from a credit card can be punishing in the form of high interest rates. Personal loans rates are typically much lower than a credit card, especially if you have good credit. If you have less than stellar credit, you can still get personal loans with bad credit, but the interest rates are going to be higher. When you need money, and you don’t want to deal with borrowing from credit cards or other forms of lending like payday loans, you should look into how to get personal loans that fit your need for funding.

Finding out where to get personal loans is easy. You can find personal loans at banks and credit unions, and you’ll find plenty of personal loans online. It’s also possible to find personal loans with fair credit and bad credit, and personal loans with no credit check. This type of loan is flexible in terms of how you use the money, but always keep in mind that it’s still a loan. Still wondering how do personal loans work? Here’s how:

Common Uses for a Personal Loan

Personal loans are used for a wide variety of reasons. Sometimes people use personal loans to pay off debt, and sometimes they use personal loans for home improvement. They can also be used to pay for a wedding, get dental work done, pay for funeral expenses, or simply make a large purchase. As long as you have a legitimate need for a personal loan, you can apply and seek funding. Here are some of the common uses for personal loans:

Debt Consolidation

The most common use of personal loans is to pay off credit card debt. It’s easier to get out of debt when you’re paying a fixed rate of interest instead of a variable interest. For example: you have a credit card with 24% APR. You’re paying 2% of the balance in interest every month for a total of 24% annual percentage rate throughout the year. As you use your card, your balance increases and the amount you pay in interest on the principal balance goes up as well. A personal loan has a fixed interest rate that is calculated when the loan is initiated, and won’t change as the loan is paid down.

Emergency Expenses

Life has ways of throwing curve balls and putting you in sudden need of money that you don’t have. A personal loan can help you pay for the emergency and help you get back on track quickly. This is where a personal loan with same day funding comes in handy as it gets you the money you need quickly.

Wedding Expenses

Weddings can get expensive quickly, even when trying to keep to a budget. Taking out a personal loan for wedding expenses helps you pay for every aspect of the wedding or cover a shortfall. The personal loan can be used to pay for the wedding dress, cake, decorations, reception hall, and even tuxedo rentals. You can take out a personal loan for a wedding even if you have savings set aside for rainy days or emergencies.

Buying a Vehicle

Car manufacturers frequently advertise low or zero interest lending on their vehicles, but it’s hard to qualify for those interest rates. If you have fair or bad credit, you’re going to get a hefty interest rate to finance a car at the dealership. A personal loan for buying a vehicle can help you get the car with a lower interest rate, or provide enough for a downpayment that reduces the amount you have to finance at a higher interest rate. You can also use a personal loan to buy a vehicle for a new business that doesn’t have

Vacation

Whether you have a dream vacation in mind, or just want to avoid using your credit cards for a vacation, you can use a personal loan to fund your trip. You can use the loan to purchase plane tickets, pay for car rental, and the hotel room. Make sure to be sensible in your use of personal loans for a vacation so you don’t wind up repaying multiple personal loans for years to come.

How Do Personal Loans Work?

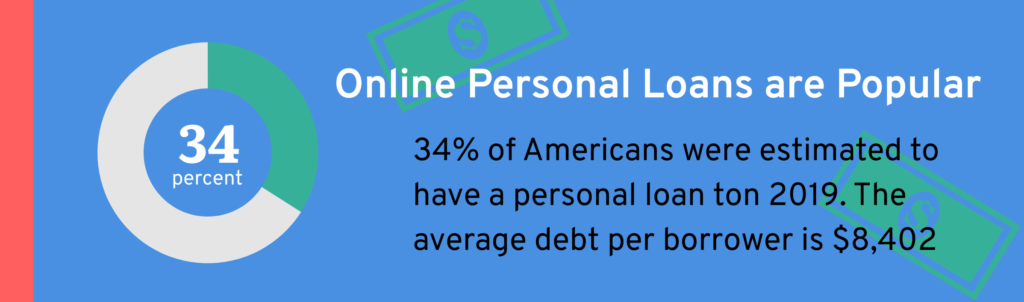

As previously mentioned, personal loans are unsecured loans. They don’t require an asset to borrow against, just your personal guarantee, but the fact they’re unsecured means that the maximum amounts are on the low side. Lenders for personal loans offer amounts that range from $500 to $100,000, but the average personal loan is around $7,000. As part of how personal loans work, you can expect to be asked the reason why you need to borrow money even though you may want to keep the reason private. Lenders for personal loans use the information you provide to make their decision on the loan terms, and your reason for borrowing is one of them. The lender wants to get repaid and your stated use for the loan helps them evaluate the risk of loaning you the money.

Once the lender has approved your application, you get the funds in your bank account through direct deposit or via a check. Most lenders for personal loans prefer to deposit the money directly into an account for security purposes and to prevent fraud. Some lenders can fund personal loans same day after processing your application, but make sure that the lender isn’t a payday loan posing as a provider of personal loans.

After you’ve received your funds, you can use the money for your intended purpose. You’ll also receive paperwork that outlines the terms of the personal loan, when your first payment is due, and its length. Terms include the APR, monthly payment, any penalties for paying the loan off before its final due date, and your repayment options (payment by mail or electronically). Some lenders expect to get the full amount of interest as stated in the loan and want to discourage early repayment. To that end, the lender will include a prepayment penalty amount that’s designed to discourage you from paying back the loan early.

A majority of personal loans use a simple interest model where the total amount of interest you pay is calculated by multiplying the principal amount times the interest rate times the time period. The formula for a $10,000 loan at 4% interest for four years looks like this: 10,000 x .04 x 4 = $1600. You’ll pay $1,600 in interest over the lifespan of the loan and wind up paying $11,600 if you make timely payments every month for four years. Paying extra towards the principal loan balance helps you lower the amount of interest you ultimately pay for the loan.

When looking at the queston of “how do personal loans work?”, you’ll find it’s fairly straightforward. A personal loan is like a traditional loan in that you get the money up front, then repay it over time. What you can’t do with a personal loan is borrow against the amount you’ve paid off like a line of credit or a credit card. The principal loan balance diminishes over time as payments are made, and the loan closes out entirely once you’ve made your last payment. If you want to borrow more money, you need to apply for more personal loans online or in-person with your lending institution.

How to Qualify for a Personal Loan

When looking into how to get personal loans, you’ll find that there are a number of personal loan lenders that offer loans to cover a variety of personal needs and financial circumstances. There are personal loans to pay off credit cards, personal loans to pay off debt, personal loans for home improvement, and for just about any reason you need to borrow money. The easiest way to find out what you need to qualify for a loan is to look into personal loans online and find the application criteria a lender requires from a prospective borrower.

Qualifying for a personal loan is relatively simple. You need to have a stated reason as to why you need to borrow money, a reasonable credit score, and be able to demonstrate your ability to repay the loan. The qualification requirements for getting a personal loan is similar to getting a credit card in that both are unsecured debt, but you should at least know your personal credit score prior to applying. You can still get personal loans with bad credit, but you will pay more interest than someone who’s credit score is higher. In the event your credit score is bad, you could look into getting personal loans with no credit check. However, personal loans with no credit check are going to charge interest rates that rival that of payday loans.

Pros/Cons of Personal Loans

Personal loans, just like any other type of loan, come with pros and cons. The most obvious drawback to getting a personal loan is the fact it adds to your debt load, and you have monthly payments for years to come. In contrast, the benefit of a personal loan is one of getting a large amount of money at once to help you make a necessary purchase, home repair, or pay for a personal need. Here’s a look at personal loans pros and cons:

Pros:

One of the biggest advantages of personal loans is the fact that it helps borrowers with their credit rating. Getting a personal loan with bad credit doesn’t mean you’ll always have bad credit. Making payments on-time and regularly are two actions that help increase your credit score over time. They also don’t require collateral to secure the loan, eliminating the need to find an asset with enough value to help underwrite the loan. A personal loan also makes it easier to pay for a large purchase over time without resorting to the use of a credit card. You can buy furniture, appliances, electronics, and more with a personal loan, then pay the balance down and know that you won’t owe more than what you agreed to pay.

Cons:

Taking out a personal loan requires engaging in personal responsibility to repay what’s been borrowed. If you have dings in your credit report, you’ll find that personal loans for fair credit can have higher interest rates that rival that rival that of credit cards. Another issue is the fact that personal loan lenders don’t hesitate to report late payments and nonpayments to credit bureaus, further hurting your credit score. And if you have a credit score of 585 or lower, you may be asked to put up collateral to secure the debt even though personal loans are usually unsecured. Last, but not least, in most situations, taking out a personal loan is taking on debt, an action that needs to be taken seriously due to the impact it can have on your life if you get into a situation where repayment is difficult.

Choosing a Personal Loan

There are a lot of personal loan lenders on the market, but they’re not all created equal. When you’re looking at personal loans online, you’ll probably notice that there are a lot of lending companies that you’ve never heard of. Sometimes they’re subsidiaries of a large corporation, sometimes they’re a small lender, known as a non-banking financial institution, who is looking to target a specific market. You’ll also find personal loans from credit unions and personal loans from banks as you look at the different financial institutions offering you the opportunity to apply. In the event you have a good working relationship with your bank or credit union, you can look at their personal loans online to find out what they offer, then use your customer status to help improve your chances of getting approved for the loan amount you need along with favorable interest rates and fees. Otherwise, you’ll want to find banks with personal loans with the best possible terms for lending.

Once you’ve identified on how to get personal loans, you need to zero in on the details of the loan. Your biggest concern is going to be finding personal loans with low interest rates in order to save as much money as you can on borrowing the money. A loan origination fee can be as high as 8% and lower the amount you’re able to borrow. For example: You want to borrow $5,000, but the origination fee is 5%. You could pay an extra $250 for the privilege of getting the personal loan, and that’s on top of the interest. This is not an unusual feature of personal loans, but it can make you keep looking to find a loan that has a low origination fee. Other details you need to consider include:

- Fixed or variable interest

- APR

- Monthly payment

- Loan term or length of the loan

- Automatic withdrawal

- Discount or lower interest rate for automatic withdrawal

- Prepayment penalty

- Arbitration

All of these factors should be considered when looking at lenders for personal loans. You may not be able to find the perfect personal loan, but you can find a loan that has enough favorable terms to make it worth applying for. Fees and interest are paid off over time, are predictable, and don’t make a large impact in your monthly payment amount.

Red Flags – Things to Look Out For

Personal loans aren’t what they always seem to be on the surface. Scammers target people looking for a loan, and payday loan lenders are known to misrepresent their loan products in the hopes of catching the unaware. Following are some common red flags that you should pay attention to when looking to take out a personal loan.

Personal Loans With No Credit Check

Personal loans with no credit check aren’t always what they seem. They’re usually predatory in nature and designed to keep you paying off the debt for much longer than a traditional personal loan. You can pay as much as 400% APR on a no credit check personal loan and have a hefty amount for a monthly repayment. There are alternatives to this type of personal loan that won’t trap a borrower with excessive interest, and are worth looking into when you need money fast. You can find personal loans with low interest rates even if your credit isn’t all that great.

High Initiation Fees or Request for Fees Up Front

You may be required to pay an origination fee or pay to have your application processed, but payment for these fees are typically tacked onto the loan. At no time do you have to pay for the fees up front if your application is accepted. In the event the lender is asking you to pay a fee for the application or processing, walk away. No reputable lender is going to ask you for money for the submission and processing of your loan application.

Not a Personal Loan

Payday loan and title loan lenders are known to use language that obscures the fact that they’re offering something other than a personal loan. Payday and title loans are short-term loans that are secured against a paycheck or a car title. They are not, under any circumstance, a personal loan. These loans have exorbitant interest rates, and are short-term in nature. Another aspect of these loans is the fact they’re small dollar amount loans, and won’t offer funding in the amounts that a personal loan can.

Always make sure to look closely at the website offering a personal loan. There are many legitimate lenders that are not well-known, yet have a long history of lending and are trustworthy. Legitimate personal loan lenders are traceable and registered with state and federal agencies. Look for the lender’s information at the bottom of the website and use that to find out more about the lender before you fill out an application.

Website Redirects You

Website redirects used to be a common scam that involved redirecting you to a different website to start or finish filling out information. Nowadays, it’s not as common, but there are operators that still use this tactic to trap the unaware. If you find your browser is being redirected to a new page, close the tab and start over in your search for a personal loan. You don’t lose anything by closing out the tab, but you will save yourself from a lot of hassle.

Personal Loans vs. Credit Cards

On the surface, the comparison of personal loans versus credit cards seems to be something of a coin toss in terms of which option to take. You could use a credit card with a low promotional APR on purchases for a set period of time, and pay off the card before the period expires. But there are issues that come with using a credit card for this purpose in the form of higher payments, short time frame for repayment, and the risk of losing the promotional APR if you’re late with a payment. Credit cards are very unforgiving when it comes to making a mistake and may make you wish you had gone with a personal loan in the first place.

A personal loan tends to be more forgiving when it comes to interest and repayment. The interest rate you start out with stays the same throughout the life of the loan. There are no promotional APR periods that expire and increase unlike a credit card. You can also rely on your monthly payment staying the same for the loan term with no surprises unless you miss a payment and are charged a late fee. In fact, many people turn to personal loans to pay off credit cards because they save a lot of money in interest and can pay off the debt in less time than if they tried to pay off the card itself.

Related Content:

How to Get Started with Investing

Best Credit Cards for Senior Citizens

100 Online Finance Tools To Manage Your Money & Investments