Whether you’re looking for a card to improve your credit score, never had a credit card, or just want one that pays off in rewards when you use it, finding the best cards for seniors can be challenging. When choosing the best credit card for seniors, there are many factors to consider, including why seniors may need a new card in the first place.

Best Credit Card for Seniors Reviews

Considering a zero annual fee, high cash back rewards, and no foreign transaction fees, the Capital One Quicksilver Cash Rewards is the best credit card for seniors and retirees. This credit card lets you accumulate cash back as a statement credit while keeping a 0% intro APR on balance transfers.

Whether you’re looking for a welcome bonus, no annual fee, or rewards for other purchases, like drugstore purchases, you can choose from different types of cards. You need to compare their perks and nuances to make the most out of the best credit cards for seniors.

Capital One Quicksilver Cash Rewards

You can’t go wrong with the Capital One Quicksilver Card. It’s a straightforward rewards card that does everything seniors would want. Some important stats:

- $0 Annual Fee

- 0 intro APR for 15 months

- $200 Bonus (if you spend $500 in the first three months)

- 1.5% back on any kind of purchase

Unlike the Chase Ultimate Rewards that reward specific purchases, like EV charging purchases, the 1.5% reward is for any other purchase, including gas stations, charging purchases, select streaming services, or grocery stores.

Put all your spending on the Quicksilver, and you’ll find a nice bonus at the end of the year. Secondly, there are many ways to get your reward back on travel purchased – a check, a credit to your balance, even Amazon combined purchases, and other eligible purchases.

On top of all that, Capital One Quicksilver charges no annual fee and zero foreign transaction fees – a welcome rarity with rewards cards – and 0% interest for a full 15 months after account opening on eligible purchases and balance transfers.

The one downside for seniors building credit – you have to have good credit already to qualify. If you only have fair statement credit, you can get the Capital One QuicksilverOne card instead, which has the same benefits, but a $39 annual fee.

The good news is, that you’ll pay for that $39 in rewards in no time if you use the card regularly. Aside from zero foreign transaction fees, this platinum card has more perks than the Blue Cash Preferred Card, which is a card from American Express. They both have 0% intro APR on other purchases and balance transfers.

Chase Freedom Unlimited

The Chase Freedom Unlimited is another great option for credit cards for senior citizens who want cash back on bonus categories. It’s another rewards card with many more benefits than the Capital One Quicksilver. The Chase Ultimate Rewards is also more predictable than its counterpart from the same credit card issuer– the Chase Freedom Flex.

You can always check the Chase Ultimate Rewards portal for reward information on eligible purchases and cash back on travel purchased through the Chase Ultimate Rewards portal. Here are the basics:

- $0 Annual Fee

- 0% intro APR for 15 months

- $200 Bonus (on $500 in the first three months)

- 5% Rewards on travel (including Lyft), 3% on dining, 3% on drug stores, and 1.5% on all other purchases

With a high reward rate for other purchases and dining, the Chase Freedom is an excellent credit card for retirees wanting to have fun. To get the full 5% back on travel, you must book through Chase Ultimate Rewards via its portal. Any cash back you accumulate can be redeemed as a statement credit.

One little benefit is the 3% back on drugstore purchases, streaming services, and travel purchases. Sure, many seniors are getting their medication online these days, although it’s very likely you still get your prescriptions filled at your local drugstore and spend more money when you go in.

More than the zero annual fee, an excellent 3% back from the drugstore can add up nicely, especially when you redeem from the Chase Ultimate Rewards portal. For foodies and travel lovers, the Chase Freedom Unlimited also offers free DoorDash deliveries (through a DoorPass subscription).

Aside from a welcome bonus, there’s a free trip cancellation and interruption insurance if you get sick, have bad weather, or can’t take a scheduled trip for some other reason. World travelers won’t like that Chase charges a foreign transaction fee of 3%. Not the Capital One Quicksilver, though!

Compared to the card from American Express, this offers more value since you won’t incur a balance transfer fee. They both have 0 intro APR. Check your Chase Ultimate Rewards portal occasionally to ensure you’re not missing out on any rewards.

Capital One Venture Rewards

The Capital One Venture Rewards Card is a serious investment for senior travelers. This option is for the best credit card if you want to enjoy these benefits as a senior.

- Double miles on all purchases

- 50,000 bonus miles with $3000 in purchases (first three months)

- 100,000 bonus miles with $20,000 in purchases (first 12 months)

- $95 annual fee

Compared to the Chase Freedom Unlimited, the Capital One Venture Rewards card offers a lot of sweet travel deals for travelers, including some nice bonus miles to go with your other purchases. Each dollar spent equals 2 miles, and miles convert to dollar rewards on a clear 1:1 ratio – 1 cent per mile.

It’s the same amount of travel rewards no matter what you purchase, not just on specific things like travel or groceries. Plus, the Venture Rewards card has many perks, such as free concierge services and access to airport Capital One lounges. You can even double miles without tracking varying bonus categories.

Aside from a welcome bonus, travelers can get protections like collision damage waiver for rental cars, accident insurance, and even lost luggage reimbursement. Now, the one downside for seniors may be the $95 annual fee. However, it makes up by being a Mastercard with no foreign transaction fees on other eligible purchases.

After all, you want to spend your money on travel, not the annual travel rewards card fee. It’s not an outrageous fee, but it’s more than nothing. You can even redeem the travel rewards through a check, direct deposit, or statement credit.

On the other hand, if you’re opposed to an annual fee of any amount, the Capital One VentureOne Rewards card provides many of the same benefits but without the annual fee and a 0% interest for the first 12 months.

Compared to the card from American Express, this credit card offers more value. However, the Capital One Ventures Rewards card doesn’t have 0 intro APR on balance transfers and other purchases.

What Should a Senior Citizen Look for in a Credit Card?

So if you’re a retiree looking for the best cards for senior citizens, what should you be looking for – especially if it’s your first card in a long time, or ever?

Rewards

Aside from the lack of an annual fee, the best cards for seniors are rewards cards where you earn travel rewards or a welcome bonus. You don’t want to spend money (and pay it off) without getting a bonus.

There are a lot of kinds of travel rewards cards, but they have some things in common. Certain combined other purchases count toward more reward points, allowing you to earn statement credit card rewards and redeem points. Seniors looking for the best cards for their lifestyle should consider what they spend their money on.

Cash Back

Some cards will give cash-back rewards on groceries and bonus categories, while others will provide airline miles for points on travel purchased through your card. Look for a travel rewards credit card that allows you to earn rewards for other purchases from your credit card issuer, not just something specific.

While a travel card, for instance, might offer 5% back on travel-related purchases, it may also return 1%-2% on other purchases like online grocery store purchases. For instance, the Chase Freedom include gas stations, groceries, or even select streaming services.

No Annual Fee

More specifically, no annual fee. While the average credit card has an annual fee, you shouldn’t have to pay a yearly tax or annual fee for the right to spend your own money. Aside from zero foreign transaction fees, the best cards for senior citizens would include those that do not require an annual fee.

Fair Interest Rate

We all know that interest rates can be astronomical, but if you’re looking for the best credit cards for retirees, a high-interest rate is not in your best interests (rimshot).

Now, there’s no card that changes no interest forever – that’s how they make money. The average over the past year has been hovering right around 16%. But our choices for the best credit cards for seniors start out with a 0% interest rate.

And of course interest rates after the initial 0% offer tend to be variable. Choosing a card that keeps interest rates in the 10%-15% range is still possible, especially as your credit improves.

Can a Senior Citizen Get a Credit Card?

Yes, senior citizens can apply for and obtain credit cards. Credit card eligibility is primarily determined by an individual’s financial situation, creditworthiness, and ability to repay debt. Regarding card acceptance, age is usually not a deciding factor. Card companies are eager to get you on board, provided you meet the requirements.

In the generations after the Depression and WWII, seniors have been among the Americans in the best financial position. Thanks in large part to the growth in the social security system, older Americans were associated with low levels of debt, solid credit, and relatively stable income from pensions and social security.

In other words, economists didn’t worry about seniors for many decades.

Credit History and Income

Your history and income will be scrutinized when you apply for a credit card. Your retirement accounts, pensions, or other sources of income demonstrate that you have the financial means to manage a credit card correctly.

These are the main factors that determine creditworthiness. You’re in a good position if you’ve been good at paying your payments on time and managing your credit. With solid credit, your golden years can shine even brighter.

Financial Stability

Your secure financial condition is a significant asset. Even if you’re retired, credit card providers want to verify that you have a consistent flow of income. It demonstrates that you are a dependable and trustworthy cardholder. Of course, you must have an account with the provider or go through the account opening process.

How to Get a First Credit Card as a Senior?

If you’re a senior who needs to start a credit history or reestablish credit, you have something in common with 18-22-year-olds – you need credit to build credit! Fortunately, since you’re a responsible adult who presumably worked and paid bills throughout adulthood, you have more options than the whippersnappers.

- Ask a family member with good credit to add you as an authorized user: If you have a sibling, child, or even grandchild with good credit, they can add you as an authorized card user. You do not even need to use the card with no annual fee yourself; having your name associated with their excellent credit already raises your credit score.

- Take out a bank card: By law, banks cannot discriminate because of age. If you have a retirement or savings account with a bank, you should be able to take out a card with a welcome bonus from that bank. It may only be a “secured” card with a low limit and requires you to have that amount in the bank, but it will add to your credit score.

- Get bills you pay regularly added to your credit report: Mortgages, car payments, and credit cards aren’t the only proof of your financial responsibility. You can count other bills toward your good credit. For example, Experian offers the Experian Boost, which can add bills like cell phones, utilities, and other monthly bills to your credit report.

- Look into an AARP card: Barclays issues the AARP Essential Rewards Mastercard and the AARP Travel Rewards Mastercard. These reward cards focus on things seniors value – earn card rewards on travel, gas stations, and medical bills. An AARP credit card is one of the top credit choices for seniors, with no annual fee and low interest.

Every little you can do to improve your credit is a step closer!

What Is Credit Invisibility?

Though middle-class Americans seem obsessed with their score, more than 45 million Americans have no credit score. Understandably, the most significant proportion of unscorable people are aged 18-24 because they have depended on family and have not had time to build up their credit.

According to Experian, seniors have excellent credit scores of any age group, an average of 745. Plus, the older Americans get, the lower their average debt. So why are so many seniors showing invisible credit ratings?

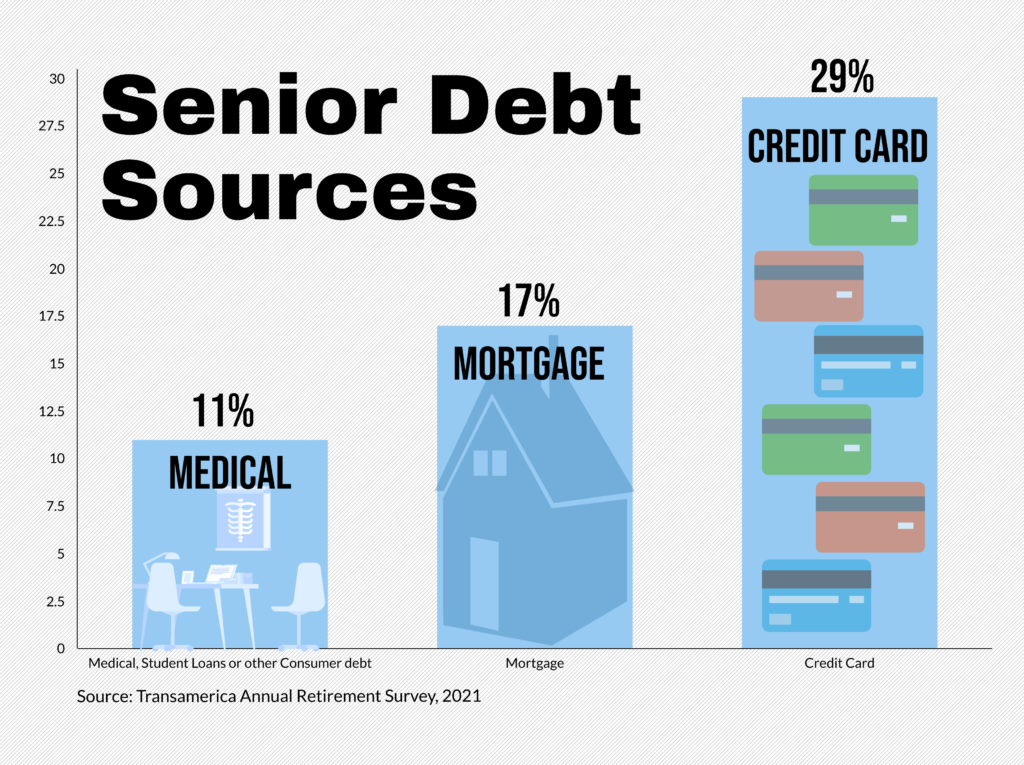

Over recent years – particularly in the 21st century – everything has changed. With the social safety net decaying, seniors now have far more issues with debt and credit than they once did. For instance, according to the Federal Reserve, while less than 10% of seniors still owed on their mortgage in 1989, more than 30% owe around $100,000 today.

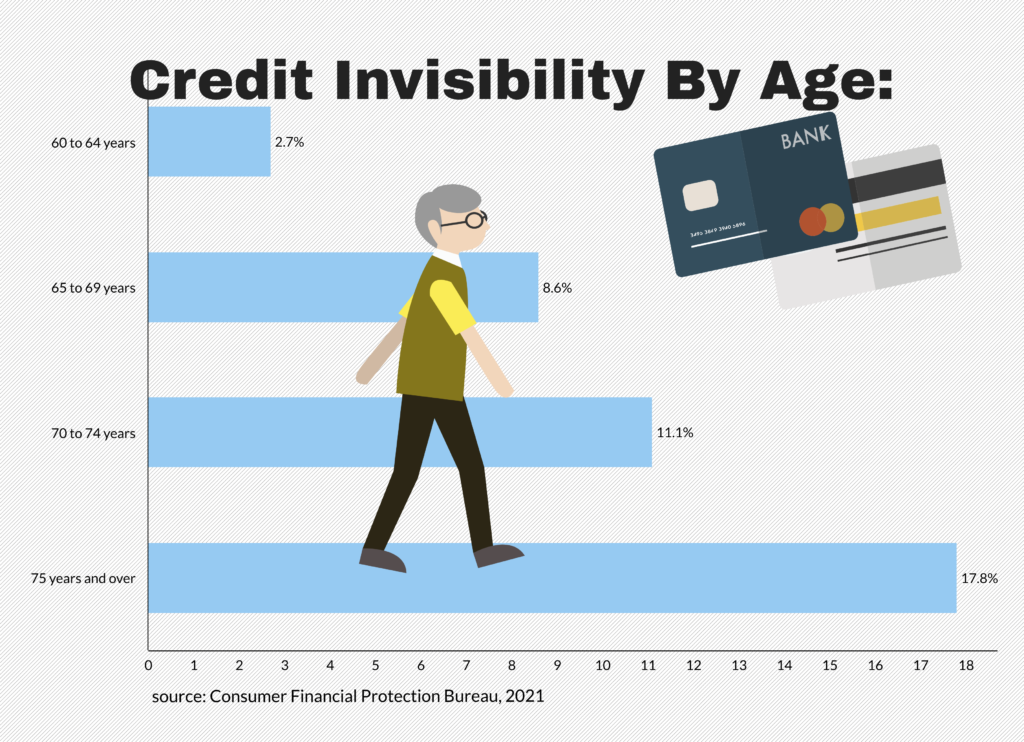

Credit Invisibility By Age

Credit invisibility diminishes for people throughout middle age. Still, according to the Consumer Finance Protection Bureau, that number goes up again at age 60, with nearly 20% of people in their 70s having no credit rating.

- 60 to 64 years – 2.7%

- 65 to 69 years – 8.6%

- 70 to 74 years – 11.1%

- 75 years and over – 17.8%

However, at the opposite end of the spectrum are a growing number of seniors with little or no credit – the “credit invisible” or “unscorable” according to the three main credit reporting agencies: Equifax, Experian, and TransUnion. Credit invisibility can be as destructive, ultimately, to a senior’s finances as debt.

What Are Some Causes of Unscored Credit?

While there are many arcane reasons your credit could be unscored, for seniors, there are some specific things that credit reporting agencies balk at:

Gender

Credit invisibility is, at least in part, a gendered problem. Consider that women were not even guaranteed the right to a credit card, by law, until 1974.

While Baby Boomer women made great strides in the workforce and financially in the1980s and 1990s, they still suffered disproportionate financial damage (versus men) by divorce, job loss, and professional years lost to child-rearing.

Furthermore, many women of older generations were content to be left off the mortgage, cards, and other lines of credit, trusting their husbands to take care of those things – only to find themselves with no credit to their name after divorce or widowhood.

Debt-Free

Ironically, being debt-free as a senior can also hurt your statement credit score. Seniors fortunate enough to have paid off their home mortgage, to have no auto loan, and to have relieved themselves of credit card debt can slip into the “unscorable” category.

That’s because credit agencies like you have some obligation aside from no debt on the annual fee– not too much. So if you have no mortgage, car loan, or card debt, congratulations – you just might have no credit.

No Job or Fixed Income

Most seniors are retired or semi-retired, but that’s a tad more complicated than it sounds.

Some older seniors may have traditional pensions, although since the advent of 401Ks, those have become a rarity. That leaves Social Security to pick up the slack, and the program has taken more than its fair share of damage in recent years.

Well, it doesn’t take much to realize that a low, fixed income and no job doesn’t look promising to credit reporting agencies or companies. By no fault of your own – because you’re just making enough to live – your credit can tank or disappear simply because you’re retired.

Low Credit Utilization

Another common reason for unscored credit is low utilization of credit; if you avoid debt, you get demerits from credit reporting agencies. A related issue is a poor mix of credit, meaning you have only ever used one form.

The agencies like to see both “revolving” credit – such as:

- Credit cards, which are not a fixed bill every month

- Installment credit – a consistently paid debt like a mortgage

- Only had a mortgage, but no cards

- Only had cards but no mortgage or car loan?

You have a poor mix, and credit reporting agencies think they can’t trust you to be able to handle the other. However, you don’t have to give up on your retirement dreams because of unscored credit. You can build your credit with these, Expensivity’s best cards for senior citizens.

Why Retirees Should Consider a New (or Additional) Credit Card

Retirement is a time to absorb life’s pleasures, engage in new adventures, and enjoy the results of your labor. Amid your newfound freedom, you may wonder why you need another card, such as a platinum card, or perhaps more than one. After all, you already have one that does everything it should.

Whether you’re interested in exotic vacations, hoping to stretch your hard-earned funds farther, or simply enjoying the simplicity of cashless transactions, a new or additional card could be the key to unlocking a world of possibilities.

The world of cards has evolved, and certain cards now offer customized advantages and privileges that can enhance your golden years. Here are some reasons to consider getting a new (or additional) credit card.

Customized Rewards Tailored to Your Lifestyle

Consider a credit card that knows your retirement goals. Many current credit cards with a welcome bonus and annual fee allow you to earn rewards, some even cash rewards, and bonuses tailored to your unique needs.

Whether you’re a travel enthusiast, a shopper, or a foodie, there’s a card with no foreign transaction fees, that may enhance your travel purchases, EV charging purchases, and other everyday purchases.

Consider it – obtaining and redeeming points, exploring bonuses on streaming services, and cash back rewards for your favorite pursuits while enjoying your retirement to the fullest.

Amplifying Your Financial Flexibility

Retirement is a moment to appreciate the independence you’ve worked hard to achieve. A new card might increase your financial flexibility, especially when you want to avoid foreign transaction fees and balance transfers. It acts as a safety net for unexpected expenses, allowing you to take chances or deal with emergencies without jeopardizing your carefully planned budget.

Navigating the Digital Landscape with Ease

A credit card, whether there’s an annual fee or not, can help you simplify your transactions in an increasingly digital world. Despite balance transfers and foreign transaction fees, online shopping, reservations, and bill payments are no longer a problem.

Not to mention that many cards come with user-friendly apps that allow you to track your transactions and manage your finances while on the road.

Fostering Credit History and Security

Even in retirement, having a good credit history is beneficial, despite foreign transaction fees and balance transfers. A new credit card with an annual fee might help you maintain your score by demonstrating prudent financial conduct. Furthermore, today’s cards frequently include enhanced security features that defend against fraudulent activity and unlawful transactions.

Exploring New Horizons

Retirement is an excellent time to broaden your horizons through travel, interests, and experiences. With a welcome bonus and annual fee, certain cards include appealing travel rewards such as airline miles, hotel discounts or hotel credit, and travel insurance.

Your retirement excursions might be even more pleasant and memorable if you choose the right rewards credit card.

Capitalizing on Cashback and Discounts

Despite paying an annual fee, many cards provide cashback, welcome bonuses, or discounts on daily transactions. This can add substantial savings over time, allowing you to stretch your retirement money further, especially when dealing with foreign transaction fees and balance transfers.

You can enjoy various bonuses, additional cash, or discounts on your favorite indulgences.

Adding a Layer of Protection

Credit cards and financial liberty offer an additional layer of safety for your transactions on foreign transaction fees and balance transfers. If you have a problem with a purchase, annual fee, or a service, some cards provide consumer protections that can assist you in resolving disputes and ensuring you get your money’s worth.

How to Make the Most of the Best Credit Cards for Seniors

To make the most of your cards and ensure that each card in your wallet becomes a vital instrument in your financial arsenal, you must first learn the ins and outs of your card. While using your credit card rewards correctly, you should remember a few things to get the most out of it.

Understand Your Card

Begin by becoming acquainted with your credit card’s terms and limitations. Understand your credit limit, interest rate, welcome bonus exceptions, and the annual fee linked with the card, such as foreign transaction fees and balance transfers. This knowledge will enable you to make informed decisions.

Among the bills you can pay off with your credit card include your annual fee, monthly cell phone bill, car rentals, online retail purchases, drugstore purchases, purchases at gas stations, EV charging purchases, and grocery stores.

Note that there may be exclusions for grocery stores; some cards may exclude Target, for instance, so be sure to keep an eye out for that.

Choose Wisely

Choose the best credit card with an annual fee that fits your lifestyle and spending patterns. If you enjoy traveling, a card gives travel rewards with zero foreign transaction fees. If you like cashback on everyday purchases, look for a card that offers it so that you earn cash and redeem rewards.

Take your time when selecting a statement credit card. Look for ones with reasonable costs, credit limits that are appropriate for you, and bonuses with bonus categories that work just great. Remember that reputed credit card companies are your best bet.

Stay Alert to Avoid Scams

As much as you would like to believe that everyone has your best interests at heart, this is only sometimes true. Be wary of fraud related to the annual fee aimed at seniors. Stick to reliable sources and issuers you know you can rely on.

Pay On Time

This is an unbreakable rule. Pay your credit card bill and annual fee on time. Late payments on the annual fee not only entail fines but they can also harm your score. The more consistent you are with your annual fee payments, the better your chances of being able to raise your spending limit.

Spend Responsibly

While having a credit card is convenient, it is critical to utilize it properly. Only spend what you can comfortably pay back. Keeping your credit use low can help your score.

Also, if you want to cash in your account, you can use a direct deposit advance to deposit from your card into your checking account.

Earn Rewards

The best credit cards for seniors provide incentives through cashback, points, or miles, even if there’s an annual fee. Ensure you understand how these rewards work and how to exploit them. It’s like receiving something back for every dollar you spend.

Track Your Expenses

Monitoring how much you spend helps you stay within your budget and avoids surprises when the bill arrives, particularly when there’s a balance transfer due and an annual fee. Many card companies offer online tools or apps that allow you to track your expenses conveniently.

Utilize Discounts and Benefits

Even when there’s a balance transfer rate or annual fee, you can use any discounts or exclusive privileges offered by your card. It’s an excellent method to save money on items you enjoy.

Credit cards provide a convenient way to make other purchases without carrying cash. Despite having to pay for an annual fee, consider the comfort of not carrying cash, the security of having a card for emergencies, and the convenience of online purchasing – all on one card!

Build Your Credit

Responsible balance transfer and card use can help your credit score. A higher score might result in lower loan interest rates and other financial benefits, such as new bonus categories or waived annual fee.

Review the Statement Credit

Check your card statements regularly for inaccuracies or fraudulent charges on the annual fee. Some may require you to pay a balance transfer fee.

It is vital to keep tabs on this because these inaccuracies can significantly hurt your creditworthiness if you don’t rectify them immediately. If you see anything suspicious, contact your card issuer right away.

Communicate with Customer Service

If you have any queries or issues regarding your annual fee or balance transfers, contact the customer service department of your credit card company. If you need help with the balance transfers, they are available to assist you in making the best use of your card.

What Are Some Common Credit Card Traps to Avoid?

Seniors who haven’t had a card before may not realize the many pitfalls to watch out for. Here are just a few things cards for seniors shouldn’t have.

Hidden and Foreign Transaction Fees

We’ve mentioned the fact that you should avoid cards with an annual fee. Even if you get away with that, look out for some other sneaky fees, like:

- Late fees

- Balance transfers

- Increased annual fee

- Foreign transaction fees (especially if you plan to travel outside the US)

- Paper statement fees (yes, they may charge you to send a paper statement – especially a problem for seniors who don’t trust paperless statements)

Hike in Interest Rate

You can expect the interest rate to go up after the 0% introductory offer on other purchases and balance transfers, but look for cards that will hike your rate without warning. Credit companies will typically do this as a penalty for late payment or maxing out, but there may be language in the contract that lets them do it for no reason.

Bait and Switch

Here’s a sneaky one the seniors applying for their first card should watch out for – the old bait-and-switch. You apply for a card that sounds good, but the company says your credit isn’t good enough for that one and issues you a less desirable card – maybe one with a high annual fee or a brutal interest rate.

Read the fine print, or talk to a representative to ensure you’re getting the card you want. You don’t have to accept a card that doesn’t work for you.

Maxing Out

Avoid maxing out your card if you’re trying to build up your credit. Not only will some companies penalize you for maxing out – it will also hurt your score. Experts say the credit reporting agencies prefer that you never go over 30% of your maximum, and over 70% starts hitting your report hard.

So yes, to build up your credit, you must use the card and pay it off. Just don’t use the card to its max.

Conclusion

In summary, as a retiree, you stand to gain more than you may realize with a new or additional credit card. So, if you’re debating whether a new card is perfect for you, consider these persuasive reasons to take advantage of this chance – your retirement might become even brighter with the proper card in your wallet.