A good credit score touches every aspect of our financial life. With little or no credit, critical loan applications may be denied. A loan application may be approved with a poor credit score but only with a higher interest rate than you would otherwise have to pay. Those two examples are just the tip of the iceberg.

You’re just building your credit score. Or, instead, you’re exploring ways to atone for past mistakes and repair your credit rating. Either way, it can be challenging to know where to begin, and this list gives options for the best cards to improve credit score.

The Best Cards to Improve Credit Score

After extensive research and careful consideration, the Discover it Secured Credit Card is the best credit card for building or improving your credit score. This card is easy to apply for and offers special perks to help make your credit rating.

In this guide to credit cards for building and improving a credit score, we present three of the very best. Which one is right for you? Keep reading for all the information you need to decide which one of these cards is best for you and your unique financial situation.

However, to provide some important context on our picks, let’s first define a credit score and explain why it is an integral part of your economic well-being.

Best Overall Credit Card for Building & Improving Credit Scores: Discover it Secured Credit Card

Many credit cards for people with little to no credit or working on improving their credit score are secured, meaning a small deposit is required to open the account. This is the case with the first pick in our ranking of the best credit cards for building and improving the score, the Discover it Secured Credit Card.

With a minimum deposit of only $200 — for a higher credit limit, deposits can be as much as $2500 — new cardholders enjoy no annual fee, and Discover matches all cash back earned at the end of the first year.

Being a store credit card, it’s also one of the most accessible cards. However, the credit limit equates to your deposit.

Choosing the Discover it Secured Credit Card requires building your credit or atoning for past financial woes, and you can still enjoy benefits on your spending. It can also be one of the most rewarding student credit cards.

Other benefits to consider include no foreign transaction fees. However, there is no introductory APR, which is a drawback, but the regular APR on the card is 22.99%, which is average. Cardholders also enjoy a 3% introductory fee on all balance transfers, but there is a 5% fee on all future transfers — just something to be aware of.

Credit limits on this card are generally pretty small, so this may not be the best card for making large purchases — not a good idea, anyway, when you’re just building credit. The other generous rewards, however, and automatic account review make the Discover it Secured Credit Card, without a doubt, the best credit card for building and improving your score.

Pros

- After eight months of good financial behavior, Discover automatically reviews your account and, if possible, will transition you to an unsecured line of credit, returning your initial deposit. You can periodically request a higher credit limit with an unsecured card from here.

- What we like about the card for building and improving credit scores is the ease with which Discover helps cardholders transition to unsecured credit as they make or improve their credit rating.

- With the card, you’ll get 2% cashback on gas and restaurant dining on up to $1K in spending each quarter. Aside from having no foreign transaction fees, there’s a 1% back on additional spending in these categories, with 1% cash back on all other purchases.

Best Credit Card for Building & Improving Credit Scores for Students: Bank of America Unlimited Cash Rewards Credit Card for Students

College is when many people begin to think about their credit rating. It’s also a time when many financial mistakes are made. For these reasons, we recommend the Bank of America Unlimited Cash Rewards Credit Card for Students.

Leading off the list of things we liked about this card is the 0% introductory APR for the first 15 billing cycles and 0% APR on any balance transfers made within the first two months after opening the account.

In comparison, Capital One automatically considers cardholders for a higher credit line in as little as six months in exchange for an affordable, refundable security deposit.

Moreover, cardholders enjoy 1.5% unlimited cashback on all purchases across all categories. Spend $1K online with the card within the first 90 days after opening the account and earn $200 in additional cash rewards.

The Unlimited Cash Rewards credit card for students allows cardholders free access to their FICO credit rating. There are also monthly updates and pointers, with other vital information to help improve your score.

All combined, the Bank of America Unlimited Cash Rewards Credit Card is undoubtedly the best credit card for students to build or improve their credit rating.

Pros

- There are also digital account alerts so you’ll never miss a payment, and otherwise, award-winning online and mobile banking services.

- This card also offers the strong security and fraud protection Bank of America is known for, with a mobile banking app helping students stay on top of their payments while keeping tabs on their financial well-being.

- The standard APR on the card is variable, ranging between 13.99% and 23.99%, which is pretty average, and outside the first two months, all balance transfers are charged a 3% fee.

Best Credit Card for Building & Improving Credit Score with Rewards: Capital One QuicksilverOne Cash Rewards Credit Card

Because you’re building or improving your credit rating, you shouldn’t miss out on the strong spending rewards other card users can enjoy. With QuicksilverOne, consumers want 1.5% cash rewards on all purchases, with no rotating categories to keep track of.

A $39 annual fee is associated with the card, but spend enough every month, and those generous rewards more than make up for it. This rate competes with cash-back credit cards aimed at people with excellent credit.

Fair to limited credit are all required to apply for the card, so if you genuinely have poor credit, there may be a better card. Reaching 26.99%, the regular APR is also high. You can also use this as a second car to increase your credit limit.

Customized alerts are available to help you stay on top of your account and make on-time payments, with strong fraud protection if the card is lost or stolen.

That’s precisely what earned the Capital One QuicksilverOne Cash Rewards credit card a spot in our ranking. It is, without a doubt, the best choice for anyone building credit who also wants some easy and convenient cash rewards to enjoy.

Pros

- QuicksilverOne also allows you to monitor your credit with their free CreditWise app. As soon as six months after opening the account, cardholders can be considered for a higher line of credit. Note that most cards require matching your credit line with an equivalent deposit.

- It’s also important to note that paying off your balance in full each month is essential with a regular APR as high as what’s offered with this credit card. However, stay on top of responsible financial behavior like that, and QuicksilverOne Cash Rewards Credit Card will pay off.

- There’s no limit to how much cashback you earn, and those rewards never expire throughout the life of the account.

How to Choose the Best Credit Card to Build Your Credit

Here are the things to consider when choosing a credit card in building credit.

Analyze Your Credit Score

You first need to check your credit score to see where you stand. This way, you can determine whether you qualify for a secured or unsecured credit card. After building credit, you could move to an unsecured card offering a higher credit limit.

People often use secured credit cards as a way to build their scores. However, remember that secured credit cards may require you to deposit cash to secure your line of credit. They also tend to require a credit line that equals your deposit amount.

Decide on Your Preferred Reward Benefits

Determine whether you want a card with rewards and benefits, including cash-back, zero foreign transaction fees, or travel insurance. If you use credit responsibly, you may avoid overspending, hurting your credit score.

Check for Free Credit Scores and Other Credit-Building Tools

The best credit cards should have credit-building systems. Know if the card offers a free FICO score or if you can monitor your credit progress over time. Some banks provide free access to a credit score.

Consider the Fees and Payment Options

Some cards charge annual fees, while others have low-interest rates. There must also be flexible payment options to avoid late fees and credit score damage.

What Is a Credit Score and Why Is It Important?

Nobody is born with a credit score. Over time, however — and as we begin to apply for and use credit cards, seek and make payments on a car loan, or sometimes simply pay our rent and utility bills each month — those good behaviors are reported to one of three major credit reporting bureaus.

Those bureaus tabulate all your on-time and tardy payments and other important metrics related to your financial responsibility, assigning you a credit rating.

- A credit score called a credit rating, is a three-digit number that financial institutions use to judge whether or not they should loan to you. If they do, what a reasonable interest rate on that loan would be: The lower the score, the higher the interest rate.

- Future creditors use that score to evaluate whether or not they should give you a loan and, if so, how much interest they should charge.

- Credit scores can increase over time based on responsible financial choices but also decrease if you miss payments or default on a loan.

- If you have some mistakes in your credit history leading to a bad credit rating — don’t despair! It is possible to repair or improve your credit rating.

What Is a Bad Credit Score?

The fact of the matter is different lenders use different standards to judge whether or not a credit score is good, bad, or just OK. For this reason, it’s difficult to point toward one specific score and call it strong, poor, or somewhere in between.

These standards are similar across the credit scoring industry, however. We’ll use the standard of one of the most well-known credit scoring services, FICO, to give you some idea of whether the number you’re dealing with needs work. Or if, instead, your credit score will open the door to a brighter financial future.

What Is a Bad FICO Score?

So, based on FICO’s rating system — which will get you close to what other credit reporting agencies consider good or bad credit — how’s your score? Does it need some work?

Credit scores between 669 and 850 are considered good credit ratings. Generally speaking, any credit rating below 669 could use some work, according to FICO.

- FICO’s credit rating standard ranges from 300 to 850.

- A score of 580 or below is considered a poor or bad credit rating.

- Ratings between 580 and 669 are considered fair.

It’s also important to note that FICO uses different models depending on the kind of loan that a consumer is applying for. FICO’s Auto Score, just as one example, ranges from 250 to 900. The higher the score, the lower the risk.

How to Improve Your Credit Score?

Here’s what to do if your credit rating needs some TLC:

Pull a Copy of Your Credit Report

The first step to repairing your credit is to find out what your score is in the first place. To do so, check your credit history with one of the three major credit bureaus. This can be done for free once a year through the website Annual Credit Report.

Pay Your Credit Card Bill on Time

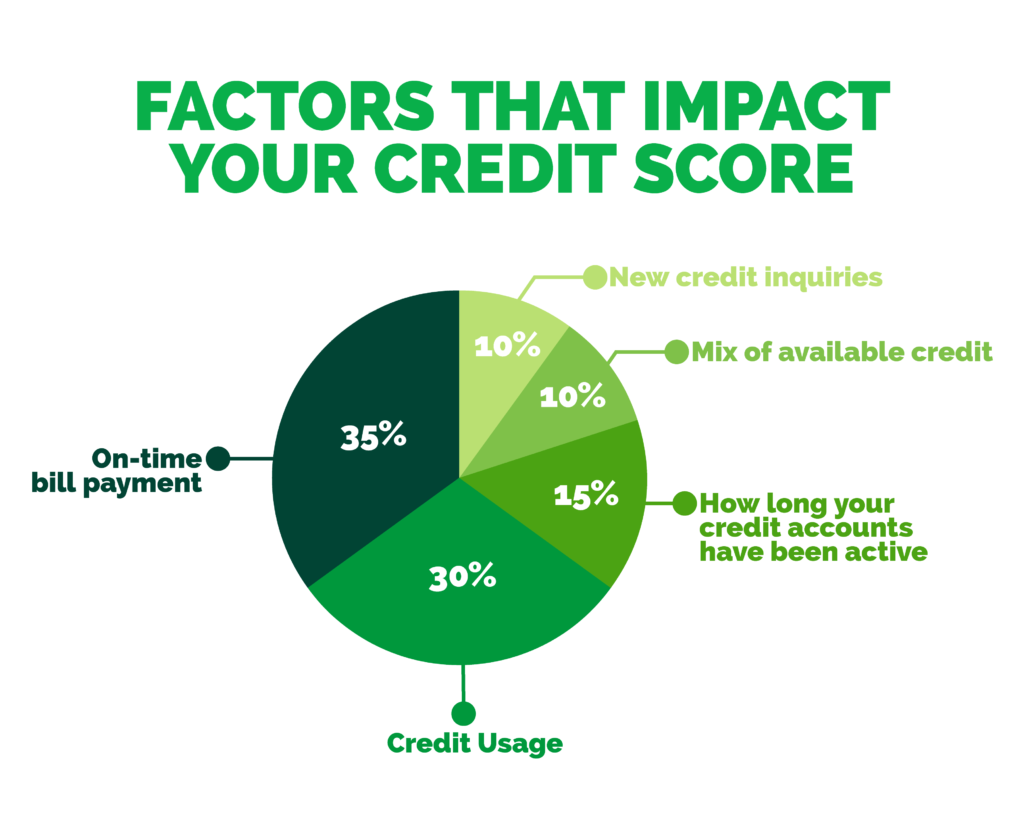

A history of on-time credit card bill payments is the most critical factor in a credit rating. FICO is the most common credit score lenders use when evaluating a loan application. Here’s how their ratings break down:

- 10% New credit inquiries

- 10% Mix of available credit

- 15% How long your credit accounts have been active

- 30% Credit usage

- 35% On-time bill payment

As can be seen, paying your bills on time is the most critical factor in a person’s credit score. If your rating could use some work, it’s a great place to start. On-time payments as a primary cardholder will help you build good credit history.

Manage Credit Utilization Ratio

Your credit utilization ratio is how much credit you have versus how much debt you carry. Keeping your credit utilization ratio, or CUR, at about 30% is generally recommended.

Limit Hard Inquiries

Yes, applying for a credit card can count against your credit score with “hard inquiries.” Among other examples, soft inquiries could include checking your credit or allowing an employer to check your credit.

How will you know when to apply if your credit card issuer doesn’t automatically consider you for unsecured credit cards? Credit card issuers will usually consider your credit history and score information when deciding whether to approve your application.

Issuers may also consider potential credit line increases upon approval. Hard inquiries include credit card applications or applying for an auto loan. Too many of these all at once in your credit history can adversely affect your credit rating for months and sometimes for years.

Keep Old Accounts Open and Address Delinquencies

If you have an old credit card account with a department store you rarely shop at anymore, don’t close the account! The age of your available credit is also essential to your credit history.

- If you do have old delinquencies, however — an account in collections, for example — it is essential to address that right away and keep all your accounts, old or new, in good standing.

- Some additional steps that can be taken to improve a credit rating include consolidating your debt and making moves to expand your “thin credit file.

- Check-in on your progress regularly with a credit monitoring service.

How to Use the Best Credit Cards Responsibly to Build Credit?

We understand what a credit score means, how to improve your credit rating, and how to judge your financial health based on your credit score.

Let’s now turn to one of the most effective means to build or improve your credit: the responsible use of one of the three credit cards listed in our ranking.

- One great way to build or improve your credit is to pay for things with one of the cards in our ranking.

- Charge, make on-time payments, pay off your balance, and earn rewards. Follow this simple formula, and a strong credit rating will follow.

Related Questions

What Is the Fastest Way to Rebuild Credit in Cards?

There fastest way to rebuild credit in cards is to have good financial behavior. Pay dues on time and address any errors on your report.

What Is the Importance of Building Credit?

Building credit is essential in seeking financial help, especially when taking out a mortgage or getting car insurance. Having a good credit score is crucial to avoid paying higher interest rates on credit cards.

Can I Check the Progress When Building Credit Scores?

Yes, you can monitor credit progress depending on the bank. There are credit bureaus that can provide annual reports. Additionally, store credit cards report payment history to credit bureaus every month.

Final Thoughts

A good credit score opens many doors in life. No one is born with good or bad credit, however. Instead, credit ratings are built over time through responsible financial behavior.

From our ranking of the best credit cards for building credit, the responsible use of a credit card is not the only way to build or improve your credit. Take any steps outlined in our article, and you’ll see your credit rating improve, sometimes much faster than you ever expected.