Thinking of buying a new vehicle? Then you’re probably asking yourself how much car insurance do I need? Car insurance is a simple enough concept, but once you start considering all the options and types of coverage available, it can get overwhelming. Here is a helpful guide if you want to shop for car insurance and get the best rates possible.

What is Auto Insurance?

The car insurance definition is a contract between a consumer and an insurance provider that protects the former from financial losses in the event of an accident or theft.

But is car insurance required? A basic car insurance liability-only policy is required for all drivers in most states to protect other vehicles on the road. Policies are typically issued in 6-month to one-year time frames and must be renewed periodically to continue coverage.

The average car insurance cost will vary depending on the state and provider. For example, car insurance for new drivers is often higher than for older policy-holders and car insurance prices can also be impacted by the driving history of the customer as well. The purpose of an auto insurance policy is to provide financial protection in the event of an accident or theft. So, the higher the risk of an accident or theft, the higher the rate will be.

What’s Covered/What’s Not Covered By Car Insurance

The exact terms of the coverage will depend on your policy. But in general, auto insurance provides coverage for property, liability, and medical costs.

Property refers to the car itself and the belongings inside it. So this covers the cost to repair or replace the vehicle in the event of an accident or theft. Liability refers to any financial responsibilities you have as the driver to any third party because of bodily injury or property damage related to a car accident. Medical costs include any hospital bills, rehabilitation, or prescription drug costs that came from an auto accident, as well as any missed wages or funeral expenses.

Car insurance will typically cover the driver and anyone else on your policy, which includes spouses and children. A typical auto insurance policy will cover daily errands, commutes, and other regular activities. But it will not cover you while participating in any commercial driving, such as delivering food or driving for ride-sharing apps like Uber or Lyft. Commercial drivers are required to purchase a supplemental policy to protect them while on the clock.

Also, keep in mind that auto insurance only covers repairs related to an accident or theft, not routine maintenance. So, when you take the car to the shop to get the oil changed or the transmission fixed, you’ll have to pay for that out of pocket.

Auto insurance typically provides protection in the event of the following situations:

- Fire

- Theft

- Vandalism

- Weather Event

- Fallen object

- Animal damage

Anything that falls outside of those general categories isn’t likely to be covered by your auto insurance policy unless you elect to purchase special coverage. But, it will protect you from the most common dangers that impact drivers on the road.

What is Recommended for Car Insurance Coverage?

If you find yourself car insurance shopping and want to know what’s recommended for the average driver, it’s wise to start by checking the local laws. Each state has its own unique requirements and will impact what policy you choose.

Almost every state requires at least basic liability coverage. This protects any other drivers on the road if you are at fault in an accident and they are injured or their property is damaged. You can make your car insurance liability only and pay a lower monthly rate, but that comes with its risks. Full coverage typically includes medical and property damage as well as other types of coverage discussed in the next section. So, if you opt for a liability-only policy, you’re on the hook for paying for those other expenses out of pocket in the event of an accident.

It’s recommended that you get as much coverage as reasonably possible. While you shouldn’t bankrupt yourself just to cover every possible scenario, the more coverage you have, the more money you’ll save in the long run if something unexpected happens.

The recommended amount of coverage for most drivers is 100/300/100. This refers to $100,000 worth of coverage per person, $300,000 per accident in bodily injury liability, and $100,000 per accident in property damage liability. If you’re driving a sports car or an exotic vehicle, you may need more coverage, but this is a reasonable policy for the average person.

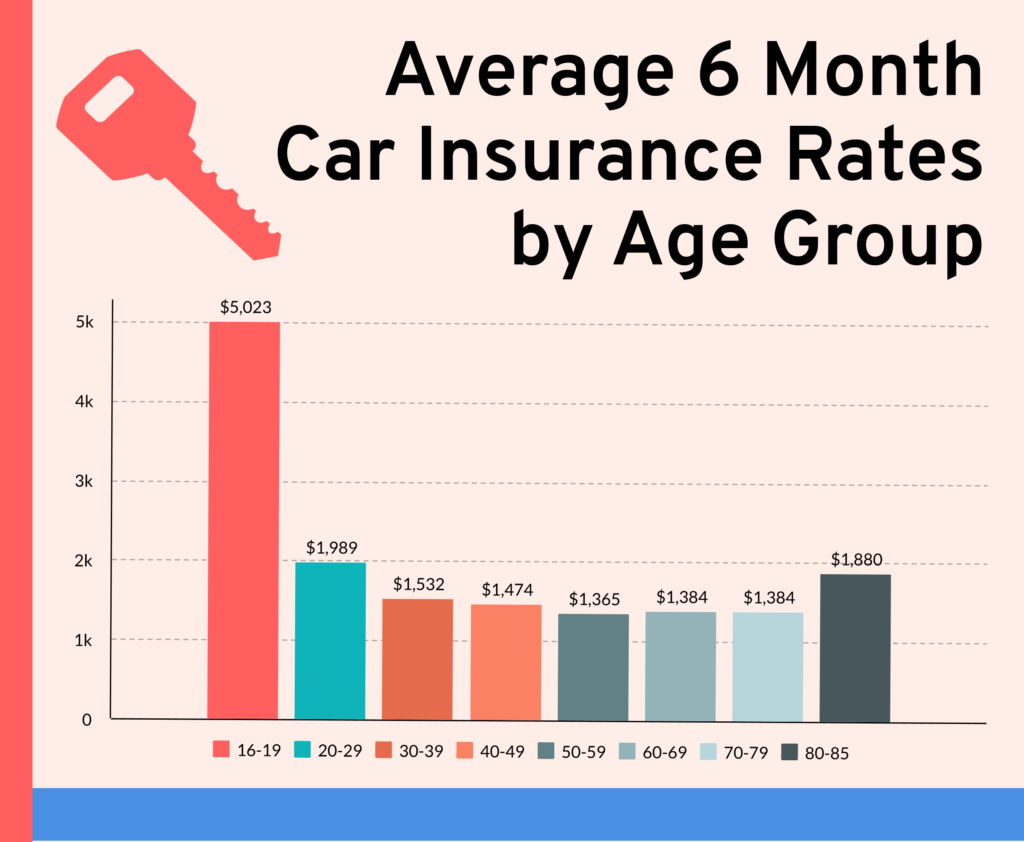

Your rate and financial situation will also impact how much coverage you receive. The cost of your car insurance premium will be influenced by your driving and credit history, as well as the state you live in. When you analyze car insurance rates by state, you’ll notice major differences across the country. The most expensive state for full coverage auto insurance is Michigan at roughly $4003 annually, while the least expensive is Maine at roughly $589.

Plus, your credit and driving history will also impact the amount of coverage you need and the cost of a car insurance premium. For instance, car insurance for teens is more expensive than it is for adults, as is car insurance with DUI. Or if you have a low credit score, you can expect to pay more to insure your vehicle.

If you’re still wondering how much car insurance do I need? then you can use a car insurance estimate calculator to find a ballpark figure. Once you have an educated number in your head, you can compare policies and decide what makes sense for your current situation. It’s important to proceed with caution because there are a lot of car insurance scams out there. But, if you do your homework and shop around, you should find a policy with a car insurance monthly cost that covers everything you need.

What are the Six Basic Types of Car Insurance?

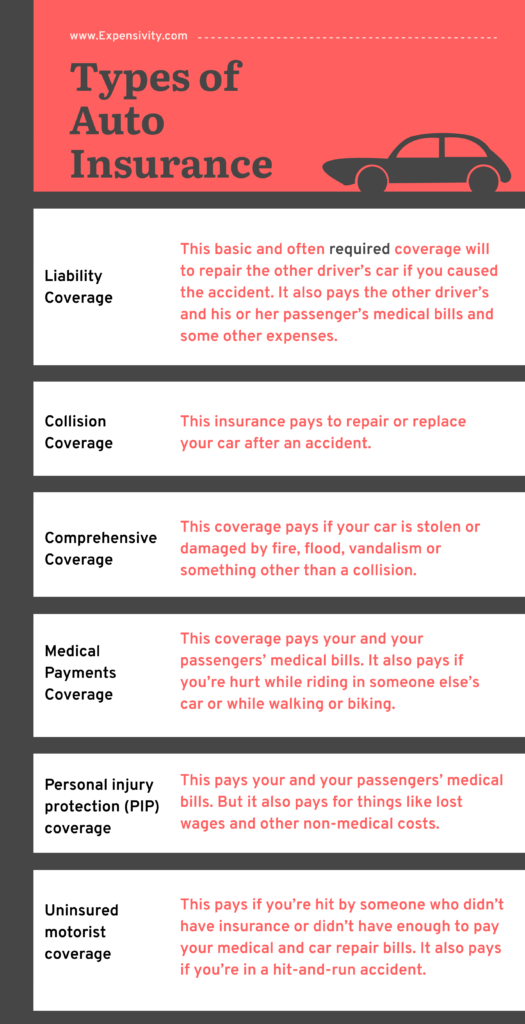

You may still be wondering which car insurance is best? Well, before you can answer that question, you need to understand the basic types of policies available. There are six basic types of car insurance coverage options: auto liability coverage, uninsured or underinsured motorist coverage, collision coverage, medical payment coverage, and personal injury protection.

Auto-liability Coverage: Liability coverage includes two components: bodily injury and property damage liability. This type of coverage is mandatory in most states.

Uninsured or Underinsured Motorist Coverage: This type of coverage helps you in the event that you get into an accident with a motorist who either isn’t insured or doesn’t have enough coverage to pay for the damage.

Comprehensive Coverage: This covers damage caused by conditions other than an accident, such as theft, vandalism, or extreme weather. Comprehensive coverage isn’t typically mandated by the state, but may be required if you’re financing the vehicle.

Collision Coverage: This covers your own vehicle in the event that you hit another car or a solid object that causes damage. It’s typically up to your discretion how much collision coverage you feel comfortable with unless you are leasing or financing the vehicle and it’s required.

Medical Payments Coverage: This covers your medical bills in the event of an accident or the bills of family members included in your policy. This includes hospital bills, surgery, X-rays, medication, and so on.

Personal Injury Protection: This helps you recoup some of the money you’ve lost as a result of your injury. This could include costs like hiring a babysitter for your child, lost wages due to being out of work, or other medical expenses. Personal injury protection is not available in all states and is not required by law.

Your policy will be made up of a combination of those six different coverage options. To understand how car insurance works you need to understand each of these different types of coverage. The types of coverage available and the amount of each option will vary depending on the policy. But those who want the best coverage possible are advised to carefully consider each of them and discuss options with an insurance professional.

What is the Most Important Type of Car Insurance You Should Have?

Still wondering which car insurance is best? Now that you understand the different types of coverage available, you can decide which car insurance is best for you. The most important type of coverage you need to get is state-mandated bodily injury and property damage liability coverage. It’s up to you to decide how much coverage you want for your own personal property and medical expenses. But once you get on the road, you pose a potential threat to other drivers. Therefore, you must have some basic liability coverage in place before doing so.

But, that doesn’t mean that the other types of coverage aren’t important as well. If you plan on financing the vehicle, the terms of the loan may require you to purchase comprehensive or collision coverage. If you live in an area that is prone to extreme weather like hail or constant rainfall, comprehensive coverage is a must. The same is true if you live or frequent an area with a lot of crime. Likewise, if you have a history of getting into fender benders and other accidents, then investing in solid collision coverage is also wise.

You’ll have to consider all these factors and weigh the costs of coverage against the potential losses you’ll suffer if something happens and you aren’t properly insured. This is why it’s smart to have a solid insurance agent to help you decide on a policy that makes sense for your needs and financial situation.

Who’s Needs Auto Insurance and How Much is Required?

Car insurance requirements vary from state to state. Every state in the US, except for New Hampshire, requires some minimum liability insurance. But the amount of coverage legally required changes based on your location. Some states also require more coverage types than others, such as comprehensive and collision coverage. Other states have loopholes that allow you to drive without coverage.

For instance, Arizona allows drivers to provide a bond or cash deposit to the DMV to substitute for basic car insurance and Virginia allows motorists with clean driving records to register as uninsured if they pay an annual fee. None of these methods replace an insurance policy, but it allows drivers to legally hit the road without coverage.

Typically, states with fewer urban areas tend to have laxer car insurance requirements. This is why car insurance rates by state vary so much. A car insurance estimate calculator can help you determine how much insurance is required for your state and personal driving history.

The owner of the vehicle whose name is on the title is the one required to purchase the policy. The policy will also include the spouse and children of the insured who reside in the same household, as long as they are licensed to drive. Anyone driving the insured vehicle is also protected, as long as the owner grants them permission to use the car.

Also, keep in mind that if you are financing the car, your lender may have certain minimum insurance requirements. Many financial institutions’ requirements require full coverage, including comprehensive, collision, and liability insurance.

If you’re still wondering how much car insurance do I need? It’s wise to review the state requirements and then consult with your bank and car dealership. It may also be smart to consult with an insurance professional to verify the advice of these parties so you get the best rate possible.

How to Save Money on Car Insurance?

If you are currently car insurance shopping, you’re probably wondering why car insurance is so expensive? Well, the truth is that it doesn’t have to be.

There are several ways you can save money on car insurance. Many policies require what is called a car insurance deductible. This is a lump sum of money that you pay if there is an accident. The average car insurance deductible is typically around $500. So if you get into an accident and need to file a $2,000 claim, you must first pay the $500 car insurance deductible before the insurance will cover the rest.

If you are looking to save money on your car insurance monthly costs, you can choose a policy with a higher deductible. Keep in mind that this may backfire if you get into an accident and have to file a claim. But if you’re confident in your driving abilities and would rather take the risk than pay a higher monthly car insurance premium, then this is one way to save money.

Other ways to reduce car insurance prices include looking for multi-vehicle discounts, taking defensive driving courses, shopping around to get the best rate, or working on your credit.

There are also certain types of drivers that are more expensive to insure than others. Ways to reduce car insurance for teens include getting good grades, purchasing a safe, practical vehicle, or completing driver’s Ed. When you shop for car insurance, you should always keep an eye out for any discounts available and compare rates to get the best deal possible.

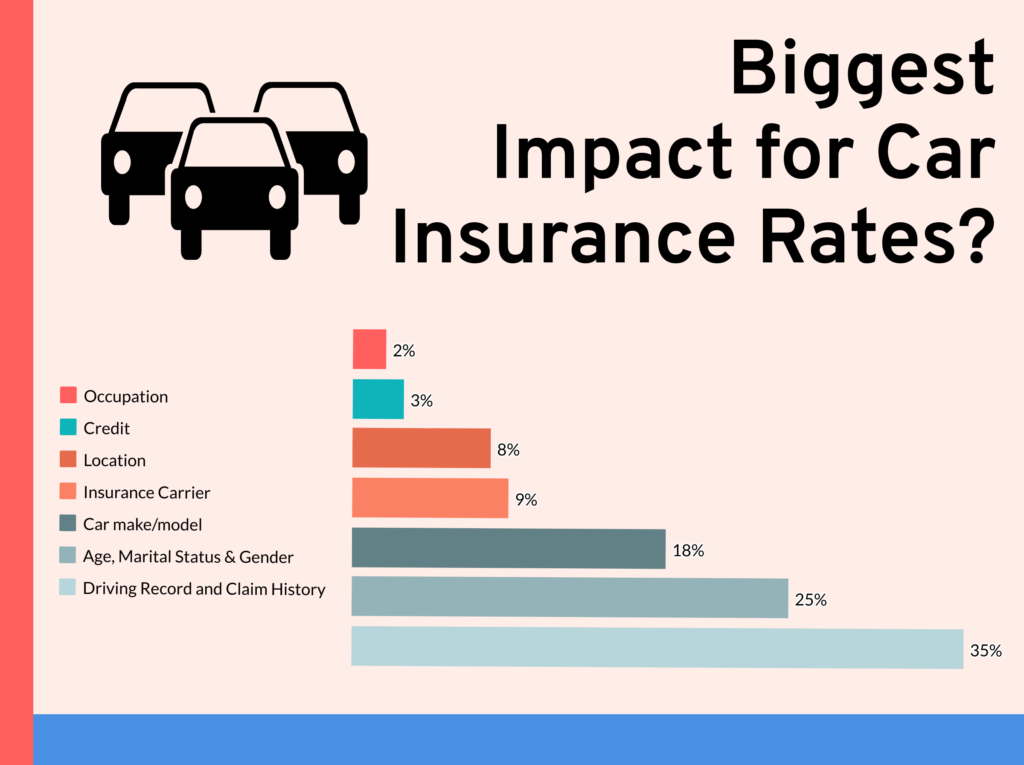

What Factors Affect My Rate?

There are a variety of factors that will impact your car insurance cost, that all relate to your level of risk as a driver. Those who are deemed riskier will pay a higher rate than those who are deemed to be safe drivers. For instance, car insurance for new drivers is more expensive than it will be for those with experience on the road. Likewise, car insurance with a DUI will be more costly than it will be for those with a clean record.

The factors that typically affect your rate include:

- Driving History: Any record of accidents? Traffic violations? DUIs?

- Vehicle Use: Are you just running errands after work or commuting an hour every day?

- Location: Do you live in a city or a suburb? Does your neighborhood have a high rate of theft or vandalism?

- The Vehicle Itself: Are you insuring a comfortable sedan or a sports car? Does the car have the proper safety features installed? How many miles does it have on it?

- Credit History: Do you have a solid record of paying bills on time? Any bankruptcies, foreclosures, or other financial judgments?

- Personal profile: How old are you? What’s your gender?

Men tend to have higher car insurance rates than women because, statistically, they get in more accidents and break traffic laws more frequently. Likewise, teenage drivers are going to pay more than their parents, because they just don’t have as much experience. However, note that your rate should never be influenced by other personal information like race, religion, or sexual orientation. Basing an insurance rate on these factors would be considered discrimination and is against the law.

Understanding Your Policy?

Now that you’ve had car insurance explained thoroughly, it’s important to be sure that you understand your policy. Car insurance shopping can get overwhelming if you don’t understand what you’re looking at, so it’s important to know what you’re getting yourself into before signing anything binding. An auto insurance policy is a legal contract and therefore, you must be sure that you understand your policy before signing on the dotted line.

Declaration Page: This section will state the name of the driver, the period that the policy covers (usually 6 months or a year), the car insurance definition, and the amount of the car insurance premium. This section will also provide a brief description of the coverage provided and the maximum dollar amount that the policyholder will pay for each type of coverage. This includes which of the six types of coverage are included in the policy and how much financial protection the driver has for each.

Insuring Agreement: This is the main section of the policy and features a detailed description of what the insurance company is agreeing to do for the policyholder. This includes what coverage and protection is afforded by the car insurance premium and what is not covered. It’s important to read this section carefully because it will spell out exactly where your money will be going so there isn’t any confusion. If you don’t understand this section from reading it yourself, you may want to consult an insurance expert to ensure that everything makes sense.

Conditions of the Policy: This section describes your responsibilities to the insurance company as a policyholder. This includes how long you have after an accident or theft to file a claim and terms for canceling the policy if necessary.

It’s important to carefully review your policy to avoid car insurance scams. You have to know what is covered by your policy and what is not to know that you’re getting a good deal and avoid any situations that may put you at risk. But once you have the basics of car insurance explained to you, understanding the terms of the policy shouldn’t be too difficult.

What to Do in the Event of an Accident?

If you get into an accident, the first thing to remember is not to panic. The reason you purchase a car insurance premium in the first place is to be protected in unforeseen circumstances.

The first step is to check to make sure everyone involved is OK and seek medical help if necessary. Then, you should assess the damage to your vehicle and others if it’s a multi-car collision and exchange insurance information with the other driver or drivers. Once you’ve taken stock of the situation and gotten yourself and others to safety, you should call the police and file a report. You may need that police report to be able to file a claim with the insurance company.

Even if it’s an emotional situation, you should do your best to document as much as possible and take pictures if necessary. This will help ensure that you receive the maximum amount in the settlement. Once you’ve filed a police report, you should contact your insurance company and file the claim as soon as possible. The longer you wait, the tougher it will be to prove your side of the story, and the more difficult the process will be.

Once you file a claim, the insurance company will launch an investigation to determine what happened and who was at fault. They will also provide you with an estimate of how much repairs will cost, which you can use to bring your vehicle to a mechanic.

If everything goes smoothly, they will finalize the investigation and send you a settlement check to pay for repairs and anything else covered by your policy. In some instances, the case may be brought to court if there is a question about who was at fault. But these cases typically are settled before going to trial, unless drivers are disputing each other’s version of events.

Related Content: