Work on this article began when Bitcoin was trading at $60,000. Today (6/18/22) it has fallen below $20,000. Ethereum has, proportionately, taken an even bigger hit. And except for some well-backed stable coins, most cryptocurrencies are at the moment cratering. With inflation high and a recession looming, cryptocurrencies are now being dismissed as an example of “the greater fool theory.” Is this therefore the end of cryptocurrencies, and can the article below be dismissed? The article below is still relevant because, as stressed in its conclusion, existing cryptocurrencies do not reflect a mature crypto technology and call for considerable improvement. The article below takes a realistic position, stressing both strengths and weaknesses of cryptocurrencies. Recent market disruptions do nothing to invalidate its analysis. If the article below seems at the moment less timely, it nonetheless remains important, especially as the dust from the current chaos settles.

***

Cryptocurrency matters to the average person even though most people don’t own any of it. Why does it matter? Because crypto(currency) is transforming the world of money and finance, and everyone has a stake in that world. The average person therefore needs a good basic grasp of crypto and why it is important. It’s not enough, however, simply to know about crypto. To really understand crypto, you need sound actionable information about investing in crypto and benefiting from it. This article therefore covers the theory as well as the practice of cryptocurrencies.

Why is so much money chasing crypto? Many people invest in crypto because of the obvious buzz and energy that surrounds it. They don’t want to miss out on the excitement and money to be made. Fear of missing out (FOMO) is these days a big motivator for people getting into crypto. But better reasons exist for getting into it. Crypto is having an enormous impact on our conception of money and its use in society. Crypto has thus become valuable for a variety of tangible reasons:

- Financial access for the un-banked. Many people around the world have very limited, if any, access to conventional financial services and institutions. By downloading a crypto wallet to a smart phone, anyone can start transacting in crypto and assume a place at the financial table.

- Re-banking the de-banked. Crypto can be regarded as a form of free-speech money. People around the world are increasingly being de-banked for political speech. Political opponents can weave false narratives and pressure conventional financial institutions to deny financial services to targeted persons and organizations. Crypto sidesteps financial choke points, especially no-buy lists.

- Bypassing seizure and forfeiture. Police are increasingly authorized to confiscate money, whether residing in banks or sent as cash through third parties (such as USPS or FedEx), so long as they can attach even the most tenuous suspicion to it (“that money looks like it was used in drug trafficking” — no evidence needed). Crypto bypasses this concern.

- Safeguarding freedom and privacy. Crypto functions much like cash, avoiding or minimizing the role of financial intermediaries that can snoop and derail monetary transactions.

- Displacing central banks. Citizens from countries whose central banks are having a tough time maintaining the country’s currency, whether on account of political turmoil or mismanagement, can bypass the country’s currency by using crypto. Some countries, like El Salvador, even endorse this move.

- Funding local government. Local governments can decide to allow tax payments to be made in crypto, facilitating the collection of tax revenues. Miami has made this move.

- Hedge against inflation. Crypto can provide a store of value when conventional currencies lose their purchasing power, especially in times of hyperinflation (this has happened with Bitcoin in Argentina and Venezuela). Unlike conventional fiat currencies, which can be “printed without limit,” cryptocurrencies typically have an upper supply limit.

- Near frictionless transactions. Transacting funds in crypto simply means sending them electronically from one crypto wallet to another, and the computational effort to do that tends to be virtually nil. So crypto promises to make loans and financial transactions quicker, easier, and cheaper.

- High IQ filter. To understand crypto and use it effectively requires some intellectual horsepower. STEM-phobics are at a disadvantage in the crypto world. Cities and countries that embrace crypto are likely to be magnets for smart innovative people. Embracing crypto has become an obvious way to enhance a population. Miami and El Salvador are two places currently seeking such a benefit. More will follow.

- Money as a meme. Crypto is becoming a conduit for big ideas. The various coins convey collective attitudes, dispositions, or visions of a world where money is unleashed from conventional roles. An example is non-fungible tokens, or NFTs.

1 Quick Entry into Crypto Investing

This first section is for those who want to begin investing in crypto right away. But it is also for those who simply want a basic understanding of cryptocurrencies without investing in them. Later sections will present the underlying theory and history of crypto, as well as reasons to take crypto seriously but also to be cautious. Yet it helps to see how cryptocurrencies actually behave in practice, and nothing beats buying some crypto at an exchange, setting up a crypto wallet, and then sending some crypto from one wallet to another. So, in a clearheaded guide to the crypto world, it’s good to start with a practical section like this

To be a successful crypto investor, however, you’ll also need a general grasp of cryptocurrencies, The later sections of this article therefore provide a solid overview of cryptocurrencies. If you want to dig still deeper into the crypto world by investing in or even creating non-fungible tokens, you should also read Expensivity’s companion piece on non-fungible tokens.

1.1 The Bare Basics

In explaining crypto investing, we’ll focus on investing in Bitcoin and Ethereum, the two most popular cryptocurrencies with the highest market capitalization (all the other cryptocurrencies together don’t have the value of these two). Investing in other cryptocurrencies is straightforward, and simply means going to exchanges or websites that handle them, buying those cryptocurrencies there (whether in dollars or other crypto), and then procuring the appropriate (crypto) wallets that allow you to move such currencies from wallet to wallet. Specific (crypto) wallets have specific private keys and are designed to work with specific currencies.

For Bitcoin and Ethereum, the exchange I’m going to recommend is Coinbase. In our Expensivity article on the 10 best crypto exchanges, we rank Coinbase as best for first-time cryptocurrency investors. Hence, to buy bitcoins and ether (note that for Bitcoin the plural is either “bitcoins” or “bitcoin”, but for Ethereum the plural is simply “ether”; note also that these are abbreviated respectively as BTC and ETH), simply sign up for an account at Coinbase and transfer funds to the account with which to buy these cryptocurrencies.

Unlike a few years ago, government regulation and IRS intrusion into the crypto world has since gotten much more extensive, so you’ll need to verify that you are who you claim to be (KYC, or Know Your Customer, is a big deal these days with the exchanges). Once you are signed up and have funds in place, you can buy your first bitcoins and ether. As it is, Bitcoin is at the moment trading around $50,000 per BTC ( a month ago it was at an all-time high of almost $70,000) and Ethereum is trading above $4,000 per ETH, so it’s likely you will only be buying fractional bitcoins and ether.

Next, get yourself a Bitcoin wallet (such as Electrum) and an Ethereum wallet (such as MetaMask). Coinbase will now allow you to transfer cryptocurrency to those wallets and from there you can transfer cryptocurrency to still other wallets. You are now good to go in having these cryptocurrencies available to you for the purposes of buying, selling, and investing.

Using these wallets is straightforward, but do a Google search on these or any other wallets you choose to use if you get stuck. Once you set up a crypto wallet, you’ll be given a sequence that looks like this (which happens to be the one associated with my MetaMask wallet):

0x4f74085dfE2f580BaAb770b0DA9c41E6f38E065F

That’s the public address of the wallet. It’s readily copied to your clipboard. You’ll need such an address for people to send you crypto or to send yourself crypto from an exchange.

Associated with any crypto wallet is a 12-word seed phrase, which you obtain when you set up your wallet. If you lose the seed phrase, you lose your wallet and everything in it. It’s typically advised that you write down the seed phrase on paper and keep it entirely away from digital storage.

Unfortunately, paper is easily misplaced, and reports abound of people losing incredible amounts of cryptocurrency by forgetting or misplacing their seed phrase. I therefore prefer to record the seed phrase in an image file, and then hide the image among a vast horde of other images where it gets tucked away inconspicuously unless you know what you’re looking for.

A word of warning about wallets: unless you build your own crypto wallet, you are depending on a third party to keep the cryptocurrency in your wallet secure. Electrum has a long history, and seems to have escaped unforced security breaches (forced security breaches being those where bad actors steel your wallet credentials). It’s main weakness to date has been security updates subject to denial of service attacks that send users to bogus websites and then substitute a new and falsified wallet that steals your crypto. MetaMask is a bit too much in bed with Ethereum for my taste, and it has had some privacy issues, but it’s easy to use.

I’ve suggested these wallets for convenience. But I would caution against keeping too much crypto in any one wallet associated with any one address. Diversification is probably a good idea with crypto wallets. For added security, you might want to use a hardware wallet like the Ledger Nano X or Trezor T (both available on Amazon). Hardware wallets enable you to get your wallets offline except for immediate transactions. That adds safety, though it’s not foolproof.

NOMENCLATURE: In the crypto world, you’ll see references to “cryptocurrencies” as well as to “tokens.” Cryptocurrencies are encrypted digital currencies that are native to particular blockchains (blockchains are the tamper-proof digital ledgers at the heart of the crypto world). For instance, bitcoins make up the currency native to the Bitcoin blockchain, and ether make up the currency native to the Ethereum blockchain. A unit of a cryptocurrency is typically referred to as a “coin.”

Cryptocurrency blockchains can also allow transactional protocols or smart contracts. These are computer programs that run on cryptocurrency blockchains and allow for the creation of exchange mechanisms that transact units distinct from but also derived from the underlying cryptocurrency. Such derivative units are called “tokens,” and they can act like cryptocurrencies in their own right, but also serve other purposes (as, for instance, vouchers, rewards, or rebates).

The Ethereum ERC-20 standard, at the time of writing, supports 200,000 different tokens. One such token is the Basic Attention Token, which functions like a cryptocurrency but also like an open-source, decentralized ad exchange platform. Although the analogy is imperfect, it can help to think of the relation between tokens and cryptocurrencies as the relation for financial instruments between derivatives (such as options and futures) and underlying securities (such as stocks and bonds). Tokens are thus built on top of crypto.

Even though there’s a valid distinction here, many writers ignore it, describing the coins that make up a cryptocurrency also as tokens. In a sense, a coin native to a cryptocurrency is also built on top of it, so by that token (pun intended), tokens are the more general notion and encompass the coins that make up a cryptocurrency. Thus one will read (in Yahoo Finance) that “Solana’s token is the fifth-largest cryptocurrency by market cap.” The distinction is valid, but it is often breached.

Also, one more bit of nomenclature at this early point in our discussion. In the crypto literature, you’ll often find reference to “altcoins.” These are coins or tokens other than Bitcoin and Ethereum, the latter being the gold standard of the crypto world, other coins/tokens thus being treated as second-class citizens. For now, Bitcoin and Ethereum so dominate the crypto world that the “altcoin” designation seems justified.

1.2 Dangers, Pitfalls, and Snares

How much crypto gets lost or stolen? According to Business Insider, “People have lost roughly $140 billion in Bitcoin because they forgot their passwords or got locked out of accounts, and would-be millionaires are struggling to access their wallets.” That report was issued in January of 2021, when the price of Bitcoin was about half of what it is now. So with Bitcoin sitting at $60,000 per bitcoin, and thus a total market cap of around $1 trillion, total Bitcoin losses exceed $250 billion, which means that over 25 percent of all bitcoins have gone missing. Imagine if a quarter of your bank account simply went missing.

The case of James Howells is particularly poignant. He began Bitcoin mining early in the game (in 2009; Bitcoin was founded in 2008). In 2013 he inadvertently threw away the hard drive with the credentials to his Bitcoin wallet. The hard drive ended up in a landfill and he knows roughly where in the landfill it is. But the city won’t let him exhume the hard drive. On it is the information that will allow him to claim 7,500 bitcoins, valued at half a billion dollars (i.e., $500,000,000) at Bitcoin’s recent peak price.

As you start buying cryptocurrencies and moving them around between exchanges and wallets, it will feel like you are moving money remotely in the same way as with your bank through its smartphone app. But this similarity is deceiving. Crypto wallets are vulnerable to amnesia (forgetting your access credentials, typically referred to as your private key or the seed phrase that allows you to reconstruct the private key). And they are vulnerable to theft (someone stealing your private key and making off with all the crypto in your wallet). Moreover, there are no laws to redress this sort of amnesia or theft. It’s on you to keep your credentials safe and intact. That’s a lot of responsibility. That means there’s no safety net. And people pay the cost.

Working with a crypto exchange offers some safety against amnesia in that an exchange will have reliable ways of identifying and contacting you, such as through your email account or cell number. But theft remains a big problem. A crypto exchange may feel like a bank, but it is not a bank. The big difference is that with a bank, you have a trusted third party that is legally liable for your deposited funds. Moreover, the Federal Deposit Insurance Corporation insures your deposits at a given bank for up to $250,000.

With crypto, whether through an exchange or through a wallet, you are much more on your own. If hackers steal the private key to your crypto wallet, you lose all the crypto in that wallet. Similarly, if hackers break into your account at a crypto exchange, you lose whatever they choose to remove. Even at Coinbase, hackers in the fall of 2021 stole cryptocurrency from 6,000 of its customers (largely through phishing attacks).

If a crypto exchange as a whole is hacked, all the crypto assets of the exchange may be compromised. The hacking of Mt. Gox, an early Bitcoin exchange, stands out to this day. Its bankruptcy almost ruined confidence in Bitcoin. In being hacked, Mt. Gox ended up losing 650,000 BTC, worth over $40 billion at Bitcoin’s recent peak price. People who owned those BTC lost them.

I’ve had a Coinbase account since 2016, and in that time I’ve seen Coinbase’s security measures become ever more stringent. That’s encouraging, and it keeps me from being too worried about losing the crypto that I have in my account there. But the recent theft from 6,000 of its customers is less encouraging.

In any case, banks provide additional safety nets that are lacking in the crypto world. If somebody steals your debit card information and starts unloading the money in your bank account, once you catch it, the bank will stop the fraud and, if you are under the $250,000 FDIC limit, will reimburse you for your loss. I’ve experienced this myself when someone stole my debit card information at an airport, and then started buying large items at Best Buy and Walmart. By the time I caught on to what was happening, $2,000 had been removed from my account. Yet the bank, once I pointed out the theft, restored all those stolen funds. Nothing — and I mean NOTHING — like that exists on a crypto exchange.

If you accidentally wire money from your bank to the wrong account or wire the wrong amount of money, your bank will be in a position to reverse the transaction. With crypto, all transactions are irreversible, so once you send crypto, the only way to get it back is by asking the party that received your crypto to give it back. And often that party will be anonymous, so good luck with that.

If you have crypto in a wallet and somebody learns your 12-word seed phrase or the associated private cryptographic key for the wallet, they can transfer all the crypto in the wallet to one of their own crypto wallets, and you’ll have no recourse for retrieving the cryptocurrency that was transferred. Even the legal system is unclear about what it means to steal cryptocurrency. That’s because cryptocurrency theft simply moves around bits electronically on a peer-to-peer network according to agreed upon protocols, and those bits have no legal standing as claims on property. Cryptocurrency theft is a multibillion dollar a year problem, and there is no system of legal redress.

=====BEGIN SIDEBAR=====

A colleague who is both an attorney and banker, responding to an earlier draft of this article, presses these concerns further: “I’m troubled that there are no legal definitions for the terms in your article such as ‘cryptocurrency’ or ‘token’. There is no governing law defining what we’re talking about, and no law, analogous to the Uniform Commercial Code, governing the rights and responsibilities of the parties to a transaction with these undefined instruments. Maybe the rules are all internal to the cryptocurrency, but who controls those rules and could they be changed?

“As best as I can tell, if one buys a ‘cryptocurrency’ one merely buys a bookkeeping entry on the blockchain and nothing more. I have difficulty conceiving of a mere bookkeeping entry as having any value… My gut is cryptocurrencies are just self-perpetuating Ponzi schemes that could go bust if the Fed ever tightens. We’ve had easy money the entirety of Bitcoin’s existence and I’ll be interested to see how it holds up if the punch bowl is ever taken away.”

=====END SIDEBAR=====

Given these caveats, if you still want to invest in crypto, I’m going to propose two approaches. One is simple (dollar cost averaging), and the other requires more work (trend trading). I’m going to assume that you are investing in crypto because, despite extreme volatility, you see the price continuing to go up. In other words, I’m going to assume you are bullish on crypto, and thus will be going long on it.

The alternative to being bullish on crypto is being neutral or bearish about it. If you are neutral, you may just ignore it. If, on the other hand, you are bearish on crypto, thinking that it is ultimately going to crash and burn, or even if you think it is going to go down significantly in the short term, then you will likely want to sell crypto short. Short selling crypto, especially with its extreme volatility, is, however, a recipe for losing a lot of money.

Short selling requires margin trading, which Coinbase no longer allows because of recent regulatory changes in the U.S. (Coinbase is based in San Francisco.) On the other hand, Binance, based in the Cayman Islands, does allow margin trading and thus short selling of crypto. Here’s a brief video on how to short sell crypto at Binance, but engage in short selling crypto at your own peril.

In this light, it’s worth noting the attitude toward crypto of the hedge fund managers who successfully shorted mortgage-backed securities back during the financial crisis of 2007-08 (such as Michael Burry, played by Christian Bale in the film The Big Short). They made billions when the housing market collapsed in 2008. These same hedge fund managers think that Bitcoin, and crypto in general, is a bubble that ultimately will deflate to zero. Even so, they are unwilling to short Bitcoin on account of its volatility as well as their inability to predict the details of its expected demise.

One final point, which we’ll examine in more detail later, is the inequality with which crypto wealth is distributed. Those who have made the most money off of crypto have gotten in early when the crypto’s valuation was low and have profited as its price skyrocketed. Satoshi Nakamoto, the pseudonymous inventor of Bitcoin, is thought to have mined 1.1 million bitcoins. All these bitcoins have to date gone unused (did Satoshi die and are they forever lost?). Satoshi’s stash of bitcoins represents about 5 percent of all bitcoins that have or will ever be mined (the total being 21 million). At Bitcoin’s peak price to date, that represents about $70 billion. Satoshi’s case is extreme but not unique among crypto founders.

1.3 Dollar Cost Averaging

In going long on crypto, you are taking a bullish attitude toward it, thinking that over time it will, on average, continue to rise. In that case, your simplest strategy is dollar cost averaging (abbreviated DCA). In this strategy, you set aside a fixed amount of money and invest it in equal portions at regular intervals until the amount is used up.

In the limiting case, this strategy involves nothing more than putting aside a fixed amount for crypto and investing it all at once, such as when it has taken a huge dip after a historic high. Thus, after April of 2021, when Bitcoin hit over $60,000, it came down to about $30,000 that July. If you had been fortunate enough to invest in Bitcoin at that time, then you would have doubled your money when in October of 2021 Bitcoin went back up over $60,000.

In actual practice, however, dollar cost averaging means setting aside a sum money, dividing it into more than one equal portions, and investing each portion at regular intervals. For instance, suppose you’ve got $6,000. Let’s say you want to invest that amount in a given cryptocurrency, spreading it out over the next four weeks, and so $1,500 per week. Let’s say that the first week this cryptocurrency is valued at $100 per unit, the next week it goes up to $150 per unit, the next week it is down to $50 per unit, and the fourth and final week it is back to $100 per unit.

In that case, you obtain 15 units of the cryptocurrency the first week, 10 the second week, 30 the third week, and 15 the fourth week. That’s a total of 70 units of the cryptocurrency in the fourth week. Because the cryptocurrency in the fourth week is back at $100 per unit, and because you now own a total of 70 units, the value of the cryptocurrency you acquired over the last month is now $7,000, up $1,000 from what you had to invest at the start.

Note that in this four-week window, the cryptocurrency went up as much as it went down from the starting point, but you ended up gaining because you made back with extra during the low more than you lost during the high. If you’re going long, you always make money by buying low and selling high, and dollar cost averaging allows you to come out ahead as long as buying high doesn’t too much outweigh buying low.

As it is, the consistent pattern, at least for Bitcoin and Ethereum, is that however high these cryptocurrencies have gotten and however much they fall in value, they always eventually rebound and reach new unprecedented heights. If this pattern continues (no guarantees here), it means that dollar cost averaging will make you a return at whatever point you start using this strategy (even if you start at a high because you’ll be making losses back as you invest during the intervening lows and as the currency goes to its next unprecedented high). Or course, dollar cost averaging will make you that much more money the further down in the fall from the last high you start.

One caveat with this strategy: Don’t use this strategy with money that you can’t afford to lose or that you may need to reclaim for some urgent need. If you use this strategy, set aside the money you will use, and invest it according to your plan at the regular intervals specified by your plan. To make this strategy work, you need to stay the course with it.

Even so, recognize that your ability to stay with your DCA strategy may require some courage on your part given the extreme volatility of crypto. This volatility, when it hits a low, may convince you that you’ve invested in a sinking ship, in which case you’ll be tempted to jump ship. To counter this temptation, you may want to automate the investment at each interval and ignore the investments as they are happening in real time. With an investment strategy, it’s also good to have a strategy for dealing with your own psychological reactivity to unpleasant drops that may tempt you to lose heart.

1.4 Trend Trading

In trend trading (aka technical analysis), you try to capitalize on market momentum as the price goes up or as it goes down. You therefore want to buy as the market is low and sell as it is trending up (toward a peak). Conversely, you want to sell as the market is high and buy as it is trending low (toward a trough). Full-orbed trend traders will thus want to have short selling in their arsenal (so that they can sell the asset in question high even if they don’t own it).

Trend trading looks for patterns in the price movement of an asset and attempts to profit by exploiting those patterns. Does trend trading work? Economist Eugene Fama’s efficient market hypothesis suggests that it shouldn’t work because prices of assets are supposed to reflect all available information about the asset. But Fama’s subsequent work suggests that “extreme momentum tilts” of the sort one sees with cryptocurrencies may be exploited through trend trading.[1]

If you are going to be a trend trader, you really need to do your homework and develop for yourself the tools for spotting trends in the momentum of cryptocurrencies that you can exploit for profit. Some of these tools may be off the shelf, others you may need to build for yourself, and all of them will need to be continuously monitored, adapted, and updated. This can easily become a full-time job.

It’s best to start by simulated trading (often still called “paper trading”) to see how well your system for exploiting trends really works and if it is capable of delivering a profit. And even if you are successful with simulated trading (showing a virtual profit), you need to make sure you stay the course with your trading strategy once your own money is on the line (and thus stand to see a real profit or loss).

If you want to do trend trading, you need to do your homework. A good place to start is Glen Goodman’s The Crypto Trader. For a deeper dive into the type of pattern analysis (also known as “charting” or “technical analysis”) that underlies trend trading, the locus classicus is Thomas Schabacker’s Technical Analysis and Stock Market Profits, with the latest understanding of this field captured in Edwards et al.’s Technical Analysis of Stock Trends (11th edition, 2019).

Unlike dollar cost averaging, trend trading is not something you can just jump into. You first need to learn the ropes. In trend trading there are lots of moving pieces to keep track of. You’ll need to be able to get in and out of trades quickly. This will require conditional orders (such as stop and limit orders) where you can automate buys and sells when prices of the crypto in question reach certain ranges within certain time frames.

One final caveat: As with dollar cost averaging, the money you set aside for trend trading should be an amount you can afford to lose, especially in the early going. Even the best trend traders make plenty of mistakes in spotting and timing trends. As a trend trader, you expect to be losing on some trades and then hope to be making it back with more on others. But if trend trading were a magic bullet, you would see a lot more successful trend traders. The fact that you don’t is itself telling.

2 The Challenge of Picking Crypto Winners

How to Gamble If You Must is the title of a classic 1960s textbook by Lester Dubins and Jimmie Savage that used gambling concepts to teach probability and statistics. The title captured the authors’ ambivalence about gambling, namely, that gambling is typically something better to be avoided, but that if it can’t be avoided, you better know what you’re doing.

Most games of chance in the casino are “losing” games in the sense that your probability of winning on any turn is less than 50 percent, guaranteeing that any betting strategy you use will on average end up losing money. Yet even in losing games, if you know what you’re doing, you can stanch the bleeding and bleed out more slowly.

There’s a well-known exception, namely, card counting in blackjack. The competent card counter has a better than 50 percent probability of beating the casino. With “winning” games like this, you also want to know what you’re doing so that you can maximize your rate of return (assuming the casino doesn’t discover that you’re a card counter and bar your from it, or worse).[2][3]

Cryptocurrencies face the same ambivalence as gambling, but on a grander scale and with many more moving parts. A game like roulette or craps has a clearly defined probability associated with each outcome. Even securities (stocks, bonds, derivatives) can have clearly specified probability models that, with varying accuracy, describe the behavior of their prices over time. Such probability models have even resulted in Nobel prizes being awarded (as when Robert Merton and Myron Scholes received the 1997 Nobel Memorial Prize in Economic Sciences for their work on the Black-Scholes Equation).

By contrast, cryptocurrencies live in a Wild West. In August 2021 (and updated November 2021 — things move fast in the crypto world), the New York Times reported that 100 new cryptocurrencies are created daily (though most fizzle out quickly). At the time of this writing in the late fall of 2021, CoinMarketCap.com, which is the most authoritative website for tracking prices and capitalization of the most serious cryptocurrencies, lists data on over 9,000 cryptocurrencies (it was 7,000 two months ago, 6,000 two months before that).

But these numbers, as capricious as they may seem, are nonetheless way too conservative. Token Sniffer, at this time in early December 2021, lists 976,437 tokens in total, at the current rate adding about 100,000 new tokens a month. Because cryptocurrencies are entirely digital, with their implementations and transactions moving across electronic communication channels at close to the speed of light, the creation of new cryptocurrencies can and does happen very quickly.

Nor are quickly created cryptocurrencies any less technologically sophisticated or conceptually inferior to those that constitute the gold standard of crypto, such as Bitcoin and Ethereum. That’s important to bear in mind. It’s not like with Bitcoin (BTC) you are buying a top-of-the-line electric-powered vehicle and with Ripple (XRP), say, you are buying a bottom-of-the-line gasoline-powered vehicle (for fun, and as a pure digression, check out Expensivity’s article on the most expensive electric vs. gas vehicles). The technology and functionality of the two are roughly comparable (Ripple even has a big advantage in transaction speed).

Essentially, what you are paying for is the brand. Bitcoin’s market cap is about 25 times that of Ripple’s, and it has nothing to do with the underlying technology, and everything to do with perceptions and the peer-to-peer distributed infrastructure that underlies the cryptocurrency and constitutes its community of support.

Thus, except for scamcoins (bogus coins with no tech infrastructure, which are designed simply to fleece early investors), the source code for these and other cryptocurrencies is readily available, easily replicated, and quickly implemented, allowing for new cryptocurrencies to be created at will and ad nauseam.

Take Dogecoin, whose market capitalization in December 2021 sits at around $22B, but in May 2021 it hit $85B (for comparison, that’s the same as GM’s market cap; Ford’s is around $60B). It was started as a joke in 2013, and is a minor variation of Litecoin, which in turn is a minor variation of Bitcoin (see the Dogecoin Whitepaper). Even to this day, if you visit Dogecoin.com, you’ll find goofy jokes on the website, such as this quote on the homepage: “Dogecoin is an open source peer-to-peer digital currency, favored by Shiba Inus [a type of dog] worldwide.” And if Dogecoin is a joke, then Shiba Inu, which is also a coin in its own right, is a joke of a joke, with its market cap over the last several months staying neck and neck with Dogecoin (the Shiba Inu Whitepaper is even more goofy than Dogecoin’s).

It’s worth saying a bit more about Dogecoin. Jackson Palmer, a software engineer, in creating Dogecoin essentially took a preexisting software implementation of another cryptocurrency and re-ran it, adding a few tweaks and associating the Shiba Inu meme with it (which is why these are called “memecoins“). He then put it all on a website from which people could download and run the software implementation of this cryptocurrency. As it is, Palmer never made any money off of Dogecoin. He just set up the framework. People, voting with their feet, then became nodes in the peer-to-peer network that became Dogecoin. And as that network matured and interest in crypto soared, Dogecoin became valuable, eventually reaching a fantastical market cap.[4]

Joseph Kennedy, father of President John F. Kennedy, barely survived the stock market crash of 1929. He got out of the market with little time to spare. Happily for him, he reinvested in real estate, thereby make a killing during the Great Depression of the 1930s (billions by today’s standards). But the catalyst to move him out of the market occurred when a shoeshine boy gave him a stock tip. The incongruousness of the advice and of the source convinced Kennedy — if he needed further convincing — that unbridled speculation ruled the stock market, and that it was time to get out.

I had a Joseph-Kennedy moment recently in conversation with an acquaintance. With no evident background in finance, economics, or crypto, he boasted to me how a friend had urged him to buy the cryptocurrency Shiba Inu, and that within a few weeks his $200 investment was worth more than $2,000. “Close your eyes and jump in” seemed to be the take-away. Granted, I don’t think the timing of my Joseph-Kennedy moment suggests that crypto is about to implode as the stock market did in 1929, quickly after Kennedy heard from the shoeshine boy and jumped ship. But it can be hard to make sense of the money chasing crypto.

Dogecoin is emblematic of the proliferation of cryptocurrencies and the absence of market forces to rein them in. Crypto-enthusiasts will often note that individual cryptocurrencies come in limited supplies and thus come with built-in protections against inflation. Bitcoin, for instance, will only allow 21,000,000 bitcoins ever to be created. The total supply of Dogecoin is set at 131,651,445,235.

But even if individual cryptocurrencies can limit the proliferation of their coins (= units of cryptocurrency), there’s no way to limit the number of cryptocurrencies that can be created. This fact alone should concern any potential crypto investor. What this means, practically, is that the crypto world is constantly being diluted with new coins.

So let’s ask the obvious question: Is there a sound rationale for picking winners when investing in crypto? In fact, three rationales readily suggest themselves for picking winners in crypto investing. Note that these need not be mutually exclusive and can even be mutually reinforcing. These rationales are widely in use, motivating investors to put money toward crypto. It’s unclear, however, whether any of these rationales is truly sound.

- FIRST-MOVER ADVANTAGE: Invest in a cryptocurrency that has a first-mover advantage so that even with other cryptocurrencies proliferating, yours will keep a special place and keep growing in value. (Think Bitcoin and Ethereum.)

- TECHNOLOGY ADVANTAGE: Invest in a new cryptocurrency that improves on existing blockchain technology and thereby offers advantages over earlier coins — such as better anonymity, faster transaction times, and easier smart contracts — attracting eager investors and exhibiting rising prices. (Think Solana.)

- HYPE ADVANTAGE: Invest in cryptocurrencies that are being so hyped up that they keep attracting new buyers, with the result that the market cap of the hyped-up cryptocurrencies rises to ridiculous heights. (Think Shiba Inu, but also Ponzi scheme and house of cards.)

Of these, the first-mover advantage seems the best haven for crypto. Thus it would seem that cryptocurrencies like Bitcoin and Ethereum, because they got in on the ground floor, will continue to thrive whatever the vagaries of the rest of the crypto world.

The second rationale, which looks to improvements in the implementation of cryptocurrencies has some merit. But the problem is that any improved implementation can always be reimplemented. Just as Dogecoin was a reimplementation of Bitcoin/Litecoin, so we can imagine some new coin reimplementing Solana. Indeed, the Solana whitepaper is readily available and invites such reimplementation. Of course, one might argue that Solana has a first-mover advantage in implementing its souped-up proof-of-history blockchain technology, and that this may keep copycats forever in its rear-view mirror. Possibly. But how much are you willing to risk on that possibility?

Of these three rationales, the last inspires the least confidence, requiring ever increasing numbers of people to invest in crypto, which at some point must come to an end, as all Ponzi schemes eventually do. Shiba Inu is called a memecoin, but hypecoin might be a better designation. The biggest driver of Shiba Inu’s sudden popularity and surging value (it was started only in August 2020) has been a financial soap opera involving Vitalik Buterin, the founder of Ethereum.

Buterin was “gifted” hundreds of trillions of SHIB (the designation for Shiba Inu coins), and then in turn donated 50 trillion of this currency (worth $1 billion at the time) to Covid relief in India. He then also “burned” his remaining SHIB (i.e., he destroyed the cryptocurrency by sending it to a one-way wallet from which funds are unrecoverable). The total destroyed later came to be worth over $30 billion. Buterin’s stated reason for destroying all that SHIB was that he “doesn’t want the power.”

It could also be argued that by destroying roughly half the all the SHIB in existence, Buterin asserted his power over the crypto world, drew further attention to his role as Ethereum’s guru (SHIB is, after all, an Ethereum-based token), and also enhanced the value of the remaining SHIB (which is one of the main reasons people burn cypto, namely, to enhance the value of the unburned crypto — essentially lowering inflation by decreasing the money supply).

None of these rationales for investing in crypto and trying to pick winners, whether alone or in combination, is all that satisfying. And none seems particularly sound. Individual cryptocurrencies may cap the total in circulation or ever created, but there’s no way to stop the proliferation of cryptocurrencies as such. No probability models convincingly describe the market behavior of cryptocurrencies. Nor are there any reliable valuation methods to estimate their worth.

The first rationale above (i.e., Bitcoin and Ethereum having a first-mover advantage) inspires two helpful rules of thumb:

- BTC AND ETH AS HARD LIMITS: Don’t expect a cryptocurrency to show huge increases if it’s already seen huge increases and its total market capitalization is (roughly) within 3 to 4 percent of Ethereum or 1 to 2 percent of Bitcoin. The fact is, most crypto, when it sees huge hundred-fold increases, is starting at virtually zero (that’s what happened with Solana and Shiba Inu). For often strange reasons, these currencies then take off, growing wildly. If you’ve missed the initial meteoric rise, you are looking at a much slower rise thereafter (which can still be considerable). And once you get even within a few percentage points of the total market capitalization of Bitcoin or Ethereum, the crypto in question has probably roughly maxed out, with any significant rise depending on a rise of Bitcoin and Ethereum. Bitcoin and Ethereum in this way act as hard limits.

- BTC AND ETH AS BELLWEATHERS: Because of Bitcoin and Ethereum’s first-mover advantage, when they go up, all coins tend to go up, and when they go down, all coins tend to go down. I’m writing this rule of thumb in early January of 2022 as Bitcoin and Ethereum have lost about 35 percent of their value compared to their peak in November 2021. At the same time, many of the other cryptocurrencies are showing significant losses. It’s not across the board — there are exceptions. But there are significant dependencies in the market behavior of different cryptocurrencies, which suggests that if there ever is a crisis of confidence, especially in Bitcoin and Ethereum, the losses can be catastrophic.

===== ===== BEGIN SIDEBAR ===== =====

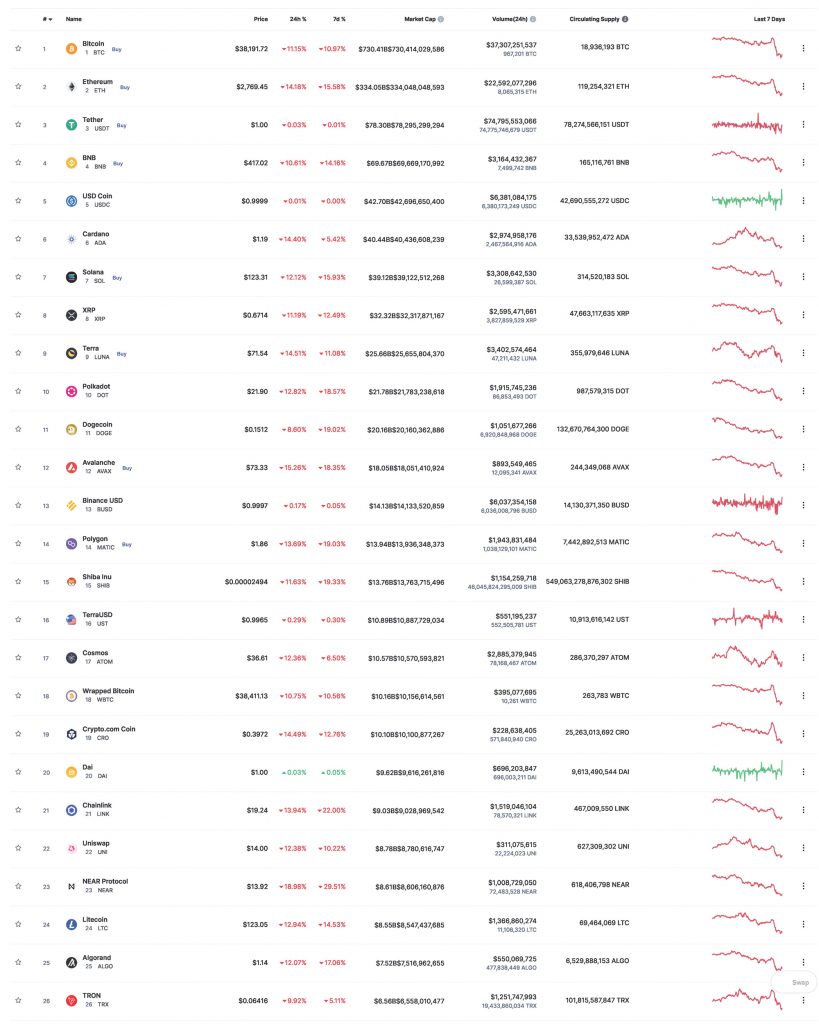

It’s now late January (January 21, 2022 to be exact). Both tech stocks and crypto have taken serious hits. Bitcoin is again below $40,000. All the top 100 cryptocurrencies, except for the stable coins, are showing palpable losses. Here are the top twenty-six cryptocurrencies as of today. Red on the right indicates loss. The only green occurs with the stable coins.

Yet despite these upheavals, with crypto losing half of its value from all time highs in recent days, confidence in crypto remains. As reported on January 24, 2022, Digital Voyager found that “about 64% of Americans surveyed … believe that crypto will gain value in 2022, with 61% saying that they’re likely to purchase some form of cryptocurrency this year.”

===== ===== END SIDEBAR ===== =====

These rationales and rules of thumb are good as far as they go, but they hardly make for an exact science. As it is, white papers for most cryptocurrencies offer nothing so earth shattering as to distinguish them fundamentally from other cryptocurrencies. In consequence, any fundamental analysis of crypto seems impossible. In fact, many in the traditional investment business see putting money toward cryptocurrencies not as an investment so much as sheer speculation, given the violent swings in cryptocurrency prices and the attendant high probability of loss.

“Oracle of Omaha” Warren Buffett remarked in 2018 that Bitcoin (and it’s safe to say here he meant all cryptocurrencies) was “probably rat poison squared.” Buffett’s second in command at Berkshire Hathaway, Charlie Munger, is even more negative about crypto, in 2021 calling it “disgusting and contrary to the interests of civilization.” He adds, “I don’t welcome a currency that’s so useful to kidnappers and extortionists and so forth, nor do I like just shuffling out of your extra billions of billions of dollars to somebody who just invented a new financial product out of thin air.” Munger applauds China for banning cryptocurrencies and wishes this form of currency had never been invented.

Munger raises here the interesting concern whether crypto is not just a bad investment but also a bad thing in general. Munger, in citing kidnappers and extortionists, suggests that cryptocurrency will behave like cash and thus bypass law enforcement. In this he echoes Harvard economist Kenneth Rogoff, who in 2017 published The Curse of Cash. There Rogoff argues that cash facilitates crime, making possible the drug trade, human trafficking, and tax evasion. But Rogoff’s concern about cash applies as well to crypto, which functions very much like cash, allowing for direct transactions away from prying eyes.

Yes, crypto will make certain types of criminal activity easier. Ross Ulbricht’s Silk Road Anonymous Marketplace, whose transactions were conducted in Bitcoin, is a case in point. But criminals operate not just outside but also inside governments, and what happens when a corrupt government outlaws crypto? Cash and crypto can prevent corrupt governments from controlling and monitoring all means of exchange. To the degree that those governments are tyrannical, cash and crypto will seem good and desirable, especially to those who value human freedom. Not coincidentally, the original impetus for developing crypto was to advance freedom and privacy.

So any question about crypto’s inherent goodness or badness needs to address where the greater danger lies, with criminals using it for criminal activities or with governments taking advantage of its absence and thereby curtailing freedoms. It’s an ongoing debate, with advocates on both sides. China, in September 2021, weighed in by banning all cryptocurrencies. China’s aims were clear, especially in light of its social credit system and desire to control all monetary transactions within its borders via its Central Bank Digital Currency (see section 7.3 of our article “The Creation of Money”).

The more important question for this article is not the morality of crypto, but whether in its current blockchain-based incarnation it can withstand efforts of governments to shut it down. So far, governments, China notwithstanding, have tended to give crypto a free ride. But what happens if there’s a universal crackdown? More on this concern in the final section of this article.

Back to Buffet and Munger. As traditional investors, they were slow to embrace technology stocks. Indeed, Buffet neatly sidestepped the Dot-com Bubble of 2001-02 by not investing in internet companies. Moreover, he didn’t invest in Apple until 2016. So their negativity toward crypto is not entirely surprising. On the other side, of course, are those who cannot sing crypto’s praises loudly enough. Elon Musk readily comes to mind. His one reservation about crypto, and Bitcoin in particular, is that the mining of crypto is not environmentally friendly, requiring too much energy consumption. Other than that, however, he’s all in. Except for the environmental cost of Bitcoin (more on that later), he would accept bitcoins in payment for Tesla automobiles.

Despite such strong reactions to cryptocurrencies — positive as well as negative — they don’t seem like manias of the past. I first learned of Bitcoin in 2011 from a computer science colleague when this cryptocurrency was in its infancy. I bought some bitcoins and ether a few years later when the price was ridiculously low by present standards, not as an investment so much as to learn by experience how crypto exchanges and crypto wallets worked (such as by sending myself crypto from one wallet to another). I never sold, and thus made a phenomenal return. The ups and downs that I’ve witnessed as I held onto this cryptocurrency have been as violent as any I’ve seen in any market. And yet I’ve always had the lingering feeling that whatever the ups and downs, these currencies never quite seem to shatter irretrievably but always seem to find new life and reach new unprecedented heights.

The manias of the past seem different. Charles Mackay’s Extraordinary Popular Delusions and the Madness of Crowds details some of these past manias and periods of mass insanity. Mackay focuses especially on economic bubbles, showing just how far off the deep end people can go in driving up the price of things to ridiculous heights where they are unsustainable and come crashing down. For instance, in the early 1700s, the shares in John Law‘s Mississippi Company rose precipitously as public enthusiasm in the venture skyrocketed but then dropped just as precipitously when public confidence evaporated once it became clear Mississippi was, at the time, a malaria infested swamp whose economic prospects were close to nil.

Past economic manias tend to show a sharp rise followed by a sharp fall, with death being permanent after the fall. Holland’s tulip mania of 1637 illustrates the same pattern. But with the Mississippi Company and Dutch tulips, people eventually came to their senses, and the object of the mania came crashing down never to be resurrected. Cryptocurrencies feel different. They inspire a lot of interesting ideas and technologies. A lot of very bright people are working on them. And new applications and implementations of cryptocurrencies are constantly being invented. We’ll discuss some of these innovations in this article. Yet things also feel crazy, so that when a correction some day really shakes things up, it’s unclear what will be left when the dust settles.

Should you, then, be bullish on crypto, thinking it will keep going up in value? But which crypto? The major coins like Bitcoin and Ethereum? These seem to keep hitting unprecedent highs, and so staying bullish on them seems not totally unreasonable. That said, some other coins have in recent days seen much more dramatic increases than either Bitcoin or Ethereum. Take, for instance, Solana and Shiba Inu, both of which have seen several hundred-fold increases in the last year and a half.

But are Solana and Shiba Inu poised to be the next Bitcoin and Ethereum, or are they on their way to becoming more like Filecoin and Zcash, which have seen their best days and are looking at steady decline? Why do some crypto coins keep going up in value, why do some outstrip others, and why do some fizzle out? Such questions admit at best partial answers in terms of the rationales and rules of thumb given above.

Much of the optimism or bullishness about crypto seems to arise from what economist John Maynard Keynes called “animal spirits,” a kind of collective emotional momentum expressed in economic activity. The question you, as a crypto investor, need to be asking yourself is whether crypto constitutes a sufficiently robust economic innovation that it will keep gathering momentum in the long run.

3 A Concise History of Cryptocurrencies

The use of cryptography to make digital financial payments has been around for decades, but that by itself does not make a cryptocurrency. A cryptocurrency is not just an electronic or digital form of money, even if the two are often confused and even though they all use cryptography to secure transactions. For something to be a full-fledged cryptocurrency, it must satisfy the following four conditions. Spoiler alert: Bitcoin, created in 2008, was the first cryptocurrency to satisfy these conditions.

- It must be self-contained, not requiring recourse to some other already existing currency;

- It must allow people to use the cryptocurrency with nothing more than a public and private cryptographic key;

- It must have a mechanism for controlling the proliferation of the currency; and

- It must function without a third party being able to deny transactions for reasons extrinsic to the transaction protocol.

Let’s consider these points in turn. The first point about a cryptocurrency being self-contained instantly separates it from the ecash and digital forms of money that predated Bitcoin. Essentially, all the precursors to Bitcoin were payment schemes denominated in a conventional currency (such as U.S. dollars). Payments would be transmitted using cryptographic protocols, perhaps with tokens, but in the end they always had to be unpacked in terms of the conventional currency.

The only exception prior to Bitcoin was Bit Gold, which typically is written uncapitalized as “bit gold.” Invented by computer scientist Nick Szabo in 1998, ten years before the release of Bitcoin, bit gold limited the proliferation of its currency by, like Bitcoin, requiring computational puzzles using hash functions to be solved in order for currency to be created.

Bit gold was a proof-of-work system, and it drew inspiration from Hashcash, which had been developed in 1992. Perhaps misnamed, Hashcash was never actually a currency or cash but rather a way of compelling internet users to prove that they had done some computational work in order for an electronic communication (such as an email) to get through to an intended user. Without this proof of work, the communication would be automatically ignored. Hashcash’s aim was therefore to control against spam and denial of service attacks by imposing a computational cost on each email or attempt to gain user attention.

In creating bit gold, Szabo repurposed Hashcash’s proof-of-work system to deliver a form of digital cash. Bit gold’s approach to proof of work using hash functions became a key component of Bitcoin. But bit gold lacked the immutable decentralized ledger of blockchain and depended on one computational puzzle to be solved before the next could be solved, rendering it unwieldy. Bit gold was never implemented, but it proved a fruitful conceptual link in the evolution of cryptocurrency — so much so that its inventor Nick Szabo is to this day regarded as the best candidate for the pseudonymous Bitcoin founder Satoshi Nakamoto (despite Szabo’s persistent denials that he is Satoshi).

Compared to bit gold, other precursors to Bitcoin looked a lot less like what we’ve come to expect and know of cryptocurrencies. Back in the 1980s and 1990s smart cards were often used to handle financial transactions. Once the Web really started to take off in the mid 1990s, many worried that credit card transactions over the Web would be too insecure to rule out massive fraud. This led to proposals such as David Chaum‘s DigiCash, which offered greater security than giving one’s credit card over the Web. DigiCash ended up going bankrupt in 1998, but Chaum did introduce a memorable idea with it, namely, the use of blind signatures to maintain anonymity by rendering payments untraceable.

Interestingly, one of the most successful digital payment schemes was developed the year DigiCash went bust: PayPal. With the rise of the smartphone, conducting financial transactions digitally has become ever easier, as we see with services like Venmo (a PayPal subsidiary) and Zelle (owned by some of our big banks such as Bank of America and Wells Fargo). But in the end, conventional money running through a central source must be used to make these systems work. Conventional money needs be front-loaded or guaranteed via a promissory note to ensure that adequate funds are in place, which can then be securely transferred, perhaps via digital tokens, to complete the transaction.

The visionaries responsible for cryptocurrency as we know it today, however, didn’t just want a quick and easy scheme for moving conventional money around electronically. They were cypherpunks, who wanted to use cryptography to ensure privacy, especially in remaining free of government and corporate surveillance. Moreover, they distrusted conventional fiat currency and were looking for an alternative to it, one that was fully decentralized. David Chaum was a key player in this movement, and his idea of blind signatures was designed to ensure anonymity and privacy.

But anonymity in Chaum’s DigiCash applied to buyers, not sellers. Blind signatures were used to keep otherwise trusted third parties (such as banks) in the dark about buyers’ identities. Blind signatures gave buyers anonymity by getting banks to digitally sign and thereby authorize transfers of money, but because the signatures were blind, transactions involving DigiCash would be untraceable back to the buyer.

DigiCash, in giving banks and established financial institutions the authority to transfer money through blind signatures, centralized its digital currency. In the evolution of cryptocurrencies, however, the move was to eliminate such centralized trusted third parties. Blind digital signatures have therefore assumed a peripheral role in today’s blockchain-based cryptocurrencies, though digital signatures as such have remained central. As it is, blind signatures remain of interest to this day in election security (where election workers are able to use blind signatures to authorize voter ballots, thereby ensuring that the election workers don’t see who the voters are voting for).

Before 2008, when the pseudonymous Satoshi Nakamoto published his white paper on Bitcoin, all the digital money schemes that had been proposed either fell flat or merely expanded the transactional range of conventional currency (fiat money).[5] But the cypherpunks always aimed higher than merely making conventional fiat currency more digitally tractable. So what finally happened in 2008 that made Bitcoin the revolution in money that it is?

It’s not that Satoshi invented anything fundamentally new in cryptography or computer science. Rather, it’s that he took items off the shelf and put them together in a novel way to create in Bitcoin a decentralized self-contained cryptocurrency. Satoshi’s abstract in his white paper is worth quoting in full because he lays out there all the key elements that Bitcoin, and its many successors, use:

ABSTRACT. A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution. Digital signatures provide part of the solution, but the main benefits are lost if a trusted third party is still required to prevent double-spending. We propose a solution to the double-spending problem using a peer-to-peer network. The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work. The longest chain not only serves as proof of the sequence of events witnessed, but proof that it came from the largest pool of CPU power. As long as a majority of CPU power is controlled by nodes that are not cooperating to attack the network, they’ll generate the longest chain and outpace attackers. The network itself requires minimal structure. Messages are broadcast on a best effort basis, and nodes can leave and rejoin the network at will, accepting the longest proof-of-work chain as proof of what happened while they were gone.

I’ve highlighted in bold the key elements that Satoshi took off the shelf to build Bitcoin. Let’s say something about each of them.

Digital signatures are essential to all cryptocurrencies in that they enable one party to securely sign over currency to another party. Digital signatures became possible with a crucial breakthrough in cryptography that happened in the 1970s. In 1976, Whitfield Diffie and Martin Hellman proposed the idea of public-key cryptography, which was then followed quickly in 1977, through the work of Ron Rivest, Adi Shamir, and Leonard Adleman, with the first successful implementation of this idea, namely, the RSA public-key cryptosystem.[6]

Before public-key cryptography, encryption and decryption were symmetric operations, so that if you knew how to encrypt a plaintext, you would also know how to decrypt a cyphertext, and vice versa. Consider a Caesar Cipher, where you treat the letters of the alphabet as positioned evenly around a circular wheel, and then move every letter a fixed number around the wheel. If encrypting a text means moving the wheel a fixed number clockwise, then decrypting it means moving the wheel that same fixed number counterclockwise. Cryptographic schemes developed through most of human history have been a lot more complicated than the Caesar cipher, but they all shared this feature of being able easily to reconstruct encryption from decryption and vice versa.

Public-key cryptography eliminated this symmetry so that decryption could for all practical purposes not be reconstructed from encryption. Thus a public key, call it E for “encryption,” could be widely disseminated and people could encrypt messages with it, but only a select few with knowledge of the private key, call it D for “decryption,” could decrypt the messages. Public-key cryptography depends on this asymmetry between public and private keys.

Such a scheme would be useful for spies in the field, who no longer had to worry about their cryptosystem being compromised in case their public key was discovered. But it quickly became clear to cryptographers that private keys could be applied to messages and thereby show that only someone who knew the private key had indeed applied that key to the message. How so? Because the public key would be widely available, and by applying the public key after the private key had been applied, one would not only recover the original message but also demonstrate that the private key had indeed been applied. And who else could apply the private key except its owner? Just as a physical signature is unique to the person writing it, so digital signatures would be unique to the person knowing the private key.

Hashing, or cryptographic hash functions, can be thought of as assigning a digital fingerprint to data. Thus we may speak of “hashing the data” and the output of doing so as producing a “hash.” The analogy to fingerprints is actually quite good (and not original with me). There’s nothing in nature that guarantees that two different people can’t have the same thumbprint, for instance. But as a matter of probability, it’s just extremely unlikely that they will. So too with hash functions, it’s not that two different items of data can’t have the same hash. But as a matter of probability, it’s extremely unlikely that they will. Extreme unlikelihood here is like picking the right grain of sand by chance from all the earth’s beaches and doing so five times in a row!

Bitcoin uses the hash function SHA-256. The National Security Agency released this version of the Secure Hash Algorithm (= SHA) in 2001 and published it with the National Institute of Standards and Technology. SHA-256 maps arbitrary text strings onto strings consisting of 256 bits, or 64 characters in hexadecimal notation (bit to hex conversion: 0000 = 0, …, 0011 = 3, …, 0111 = 7, …, 1111 = f; hex uses all ten ordinary numerals plus the letters a through f) . Let’s apply this algorithm, using an online SHA-256 calculator, to the following text taken from the opening of the Wikipedia entry on double-spending:

Double-spending is a potential flaw in a digital cash scheme in which the same single digital token can be spent more than once. Unlike physical cash, a digital token consists of a digital file that can be duplicated or falsified.

The hash, in hex notation, returned for this text is as follows (line feed and spaces were inserted for readability):

c53d9dd4 1700bb4c db47fe4b 24052d7f

abded201 236e8c5a dece4275 d7fe714d

But now, take the same text as above, the one on double-spending, but substitute a comma for the period at the end following the word “falsified” (in the actual Wikipedia entry, a period appears at the end, not a comma). Do this but make no further change to the text. Now the hash that gets returned is

4b5ea01f c694ab3f 1cd4e5cd 6f7b4ed4

61f41b9e eb297bfd a5e0b11a 1f60d84b

Even though the two texts strings to which SHA-256 was here applied are very similar (semantically as well as by any information-theoretic metric for determining similarity of symbol strings), the outputted hash values are very very different. That’s exactly what we want from hash functions: by being extremely sensitive to changes in inputted values, they can effectively guarantee that if an inputted value outputs a given hash, then that hash was constructed from that inputted value in the first place and not by some other means. Hashing thus guarantees data integrity and data origination.

Digital signatures and hashing represent the foundation pillars for Bitcoin. They are the conceptual breakthroughs in computer science that make Bitcoin possible. The remaining key elements, identified above in bold in Satoshi’s abstract for his white paper, derive from these foundational concepts or had been well understood previously. Let’s turn to these next.

Peer-to-peer networks are well understood, with successful implementations of them going at least as far back as 1999 with the original Napster (not to be confused with the music streaming service previously called Real Rhapsody and renamed Napster when Roxio acquired the Napster brand and logo). A peer-to-peer network is a networked collection of computers, run by people or groups of people, known as nodes, that interact according to certain mutually agreed upon protocols. Protocols are well-defined rule-governed procedures where it’s clear if the procedure is being followed or if it’s not.

Bitcoin introduced peer-to-peer networks to eliminate trusted third parties, such as banks and credit card companies. But in fact, Bitcoin’s peer-to-peer network does constitute a trusted third party, albeit one that is decentralized. Decentralization guarantees that with a large number of nodes, no individual node will be able to subvert the network (in the way that a centralized authority might be able to subvert a payment scheme).

Majority of CPU power in the Satoshi abstract identifies the main potential point of failure for Bitcoin. A majority of CPU power, if cooperating in an attack on the network, could subvert it. Traditional trusted third parties are like monarchies. A competent and benevolent monarch can keep a monetary scheme moving forward happily. But there’s the danger that the monarch will become corrupt, debasing the currency and arbitrarily confiscating people’s money, sending the monetary scheme into a tailspin.

Peer-to-peer networks promise instead a democracy. Yet even though moving to a peer-to-peer network can safeguard against one or a few bad actors, democracies invariably depend on the good will of the majority. And what if the majority turns bad? What if, for instance, governments hostile to Bitcoin start turning up their CPU power to such a degree that they assume the role of the majority and subvert the network (one can imagine cubicle after cubicle at the NSA serving as nodes on the network)?

To call peer-to-peer networks “trustless,” as is often done and as though to suggest “trustlessness” were a virtue of cryptocurrencies, is naive. There’s always trust. The question facing Bitcoin is whether trust in its peer-to-peer network is misplaced.

Blockchain, the key concept associated with Bitcoin, is a term that appears nowhere in Satoshi’s whitepaper. Even so, the term block appears often in the actual paper and the terms ongoing chain and record that cannot be changed appear in the abstract. These all refer to the same idea, namely, a cryptocurrency blockchain, or simply blockchain.

A blockchain is a ledger of transactions that grows in real time and that is validated at the end of each block, so that each existing block as well as the entire chain of blocks to date is validated (in the form of a Merkle tree). Validation takes the form of hashing applied to blocks individually as well as across blocks, and thus ensures that the ledger formulated as a blockchain has not been tampered with (such as someone modifying bookkeeping entries for past transactions).

Cryptocurrency blockchains constitute a complete record of all transactions ever conducted in the underlying cryptocurrency. For instance, to see every Bitcoin transaction ever conducted, go to the “explorer” feature at Blockchain.com.

Proof of work is the final piece of the Bitcoin puzzle. A question that naturally arises is why nodes (and the people working them) on the Bitcoin network should want to maintain the network in the first place, facilitating transactions and keeping a record of them. Bitcoin uses a proof-of-work consensus mechanism where miners (those nodes that maintain and govern the network) engage in solving computational puzzles (recall Hashcash) that calculate the winning hash that validates the most recent block and thereby are awarded bitcoins. Note that nodes are also incentivized to maintain the network because of transaction fees in moving bitcoins from one wallet to another.

The reference to “miners” suggests a digital parallel to mining for gold, and certainly Bitcoin miners expend a lot of computational effort to generate this cryptocurrency. As it is, only one miner is awarded bitcoins in validating any given block, with a new block being validated ever ten minutes. Winning miners are decided by whichever node best solves the computational puzzle (which roughly consists of finding a block hash with the most leading zeros).

When Bitcoin started in 2008, 50 bitcoins were awarded to winning block hashes. This number gets divided by two every four years so that in 2012 it went down to 25, in 2016 it went down to 12.5, and in 2020 it went down to 6.25. The resulting geometric progression ensures that the total number of bitcoins ever produced cannot exceed 21 million.

That’s Bitcoin in a nutshell. It’s clear that Bitcoin satisfies the four defining conditions of a full-fledged cryptocurrency that started this section, namely,

- It must be self-contained, not requiring recourse to some other already existing currency;

- It must allow people to use the cryptocurrency with nothing more than a public and private cryptographic key;

- It must have a mechanism for controlling the proliferation of the currency; and

- It must function without a third party being able to deny transactions for reasons extrinsic to the transaction protocol.

All the blockchain-based cryptocurrencies that have succeeded Bitcoin, from Ethereum to Solana, satisfy these conditions as well. Some use proof of stake or proof of history or proof of something-or-other rather than proof of work as their consensus mechanism and way to incentivize the maintenance and advancement of the underlying blockchain (proof of stake being the most common alternative to proof of work).

The one exception to these four conditions in the post-Bitcoin world is what are know as stablecoins. Stablecoins violate the first of these conditions. That’s because stablecoins, despite having the same blockchain-based transaction mechanism as Bitcoin, are also pegged to a conventional currency, units of which typically collateralize the stable coin by means of reserves. Tether, for instance, is supposedly pegged one-to-one to the US dollar, assuring its owners that “Tether’s reserves [are] fully backed.” The Wall Street Journal, however, recently questioned Tether’s full backing. In any case, stablecoins are there to assist full-fledged cryptocurrencies by allowing quick convertibility into both crypto and conventional currency.

Satoshi Nakamoto, whoever he is, did not invent any fundamentally new concept of computer science or cryptography. Nonetheless, in creatively putting together existing concepts from these fields and thereby creating the first full-fledged cryptocurrency, one that to this day dominates the crypto world (Bitcoin), his influence is enormous. For his impact, he surely deserves the Nobel Prize in economics. Unless he is dead or incapacitated, perhaps awarding him the prize would draw him out of hiding. Or perhaps not: if he’s alive and well, he seems to value his privacy.

4 Crypto’s Revolution in Money and Finance

Cryptocurrencies seem different from mass delusions of the past. They do novel things in the world of finance that many people want, such as allow for anonymous exchanges of digital currency that feel a lot like exchanges of ordinary cash. They promise to bypass intrusive government control. And they’ve attracted a lot of very smart talent that is deploying some very cool mathematics and computer science.

At the same time, cryptocurrencies raise a lot of concerns, some of which I touched on in section 1.2 (“Dangers, Pitfalls, and Snares”), but others that seem more fundamental and may upend cryptocurrencies in the long run (see the later sections of this article).

The biggest concern for me personally with blockchain-based cryptocurrencies as they exist now is that they may in fact represent an immature technology, and thus in the end may give way to a better form of cryptocurrency. Just as the automobile did away with the horse and buggy, such a superior cryptocurrency of the future could do away with cryptocurrencies of the present by greatly devaluing them or even sending them to zero.

Even so, in this section I want to consider some of the features of existing cryptocurrencies that commend them and that even in their present form are making them a revolution in money and finance. At the same time, I want to point out some of the fault lines that may make this revolution less than totally successful.

4.1 Used Like Money

Cryptocurrencies provide a way of securely moving digital items across digital space, These digital items look like currency and that in some places are actually used as currency. In Venezuela, for example, Bitcoin circumvents the country’s discredited central bank and the hyperinflation it has caused. More strikingly, in early June of 2021, the El Salvador government approved Bitcoin as legal tender.

Since then, Bitcoin has become ever more entrenched in the El Salvadoran economy. In October 2021, Bloomberg reported:

Adoption of the cryptocurrency is a way for Salvadorans to access more payment methods in a nation where more than three-quarters of citizens are unbanked, [according to central bank President Douglas Rodriguez]. He called it a means of inclusion for those whom the financial industry deems too low-income or high-risk.

Salvadorans began using the government’s Chivo wallet last month, which came preloaded with $30 in Bitcoin, to buy dips and sell rallies with fractional amounts of the cryptocurrency [thereby allowing Salvadorans even to speculate, on a small scale, with Bitcoin].

Businesses in the capital of San Salvador, from Starbucks and McDonald’s to local electronics stores, have begun to accept it in exchange for goods. Rodriguez reiterated that use of the cryptocurrency was optional and expected it to be used alongside the U.S. dollar.

The next step for the government is providing Salvadorans living in the U.S. with identification numbers, a requisite for opening a Chivo account, he said. Doing so could offer a cheaper way for those living abroad to send money back to El Salvador, Rodriguez added.

The central bank expects remittances to rise to a record $6.3 billion this year, 31% more than in 2020…

Meanwhile, in August 2021, the city of Miami began experimenting with its new MiamiCoin token, based on the CityCoins mining process built on the Stacks protocol. According to the Washington Post, reporting at the end of September 2021, “Since CityCoins unveiled ‘MiamiCoin’ in August, the protocol has sent about $7.1 million to Miami.” That’s over $7 million in crypto-taxes in less than two months. And in December 2021, Jackson, Tennessee, became the first US city to make Bitcoin a payroll option for employees.

The volatility of Bitcoin and other cryptocurrencies means that, at least for now, they are less than ideal as a long-term store of value capable of reflecting consistent stable prices (i.e., prices that don’t swing wildly). But for instant payments where prices can be adjusted on the fly, cryptocurrencies can work like money. Even with their price volatility, cryptocurrencies offer protection against hyperinflation.

Moreover, if the example of Miami in using crypto to pay for city expenses (and thus essentially to act like a tax) is any indicator of things to come, crypto’s volatility may be on its way to settling down, After all, tax levels are usually set a year in advance, stabilizing expectations about tax payments and city expenditures, and thus acting as a curb on volatility. But are we talking crypto in general or Bitcoin in particular? Bitcoin seems to be the go-to crypto for companies and governments that want to use crypto for payments. It will be interesting to see if other cryptos start competing for such payments with Bitcoin.

There’s the old joke that when something looks like a duck, walks like a duck, and quacks like a duck, then it’s a duck. The philosopher Leibniz restated this joke, without the humor, in his principle of the identity of indiscernibles. This principle states that if things resemble each other exactly, then they’re identical. Accordingly, it would seem that cryptocurrency isn’t merely like money — it is money. Whether it can be a sound, universal form of money is the deeper question, and one we’ll touch on.

4.2 The Remittances Market

Remittances are international money transfers. In the previous subsection, Bitcoin wallets were described as making remittances easy for Salvadorans by offering “a cheaper way for those living abroad to send money back to El Salvador. Remittances have a significant place in the global economy. The global remittances market is above $700 billion currently and is expected to top $900 billion by 2026.

Cryptocurrencies are ideally poised to handle remittances. That’s because anybody can download a wallet for any cryptocurrency, and then begin exchanging that cryptocurrency without restriction or borders. Any two people with wallets handling the same cryptocurrency can then send each other cryptocurrency from one wallet to the other. Geography is no obstacle here. All you need is an internet connection. People in different countries can quickly and easily send each other cryptocurrency. In fact, it’s no more difficult to send cryptocurrency to someone across the globe as to send it to someone in the same room with you.