1 Rat Poison to an Infinite Power?

Poised to radically reconfigure the crypto-asset market, non-fungible tokens, or NFTs, are revolutionizing our conception of money and value, creating not just entirely new markets but even new economies that are able to scale globally and to discover value in undreamt places, relegating to oblivion fiat currencies and old ways of doing business.

Just kidding. The previous paragraph is a parody (if such is possible) of the hype that in the first half of 2021 has come to surround non-fungible tokens. Indeed, the hype has become so overpowering that it may even defy parody. Non-fungible tokens can have legitimacy, and I’ll discuss how that can be at the end of this article. But for now the overwhelming majority of what passes for NFTs is delusion, fueled by the hope of a quick return and the belief that something can be gotten for nothing (or virtually nothing).

Warren Buffett famously remarked in 2018 that Bitcoin, and by implication all cryptocurrencies, was “probably rat poison squared.” That seems unduly pessimistic given that cryptocurrencies provide a way of securely moving around things that at least look like currency and that in some locales are actually being used like currency. In Venezuela, for instance, Bitcoin provides one way around the country’s corrupt central bank and the hyperinflation it has created. And in early June of 2021, the El Salvador government even approved Bitcoin as legal tender.

But non-fungible tokens are very different from currency. Fungible refers to things that can be interchanged without gain or loss. If you and I swap one-dollar bills, neither of us is better or worse off. If we swap equal amounts of bitcoins, we’re likewise no better or worse off (save for transaction fees). And if we swap the same number of fungible tokens (such as gambling tokens, whether these be physically stored behind a casino counter or digitally stored on a blockchain), we’re likewise no better or worse off.

But non-fungible tokens are not interchangeable in this way. They’re essentially digital collectibles. And even as collectibles, they’re nothing like physical collectibles. If I own a physical work of art, there’s no other physical object in the world that is exactly like it. Distinct medium-sized physical objects (such as can pass as a work of art, in contrast to atomic or quantum-scale particles) have the property that they differ in their constitution and structure in some discernible way (perhaps apparent only with the use of a microscope) even if the difference is minute.

This is important. Setting aside science fiction counterexamples (such as that we’re all living in “the Matrix” and so our entire existence is inherently digital), the real physical world can only be digitized by approximation and never exactly. What’s more, our technology can tell the difference. This is not to say that real-world physical objects can’t be faked. Clifford Irving’s Fake and Anne-Marie Stein’s Three Picassos Before Breakfast testify to the gullibility and incompetence of many so-called art experts. The case of Eric Hebborn, considered the greatest art forger of the 20th century, is particularly revealing about the extent to which the art market may be populated with fakes.

Nonetheless, physical collectibles have built-in safeguards against replication. Even a print-run with multiple copies of the same baseball card, for instance, cannot avoid that each card will show minute differences, even right off the press. Moreover, these differences will increase as the cards end up in individual hands and are thus handled and marred. And even putting them in plastic cases will only decelerate the work of entropy. Anything physical never stays the same but gradually transforms, and, because of entropy, typically for the worse. Rust, for example, lightens cars by about ten pounds every year (see Jonathan Waldman’s Rust: The Longest War).

But digital collectibles, whatever else they may be, are—without exception or remainder—digital files. In other words, they’re just strings of bits. As a string of bits, a digital file has a fixed number of bits, with the bit at any location in the string having a definite value of either zero or one. What this means is that digital collectibles can be copied exactly, which in turn means that you’re no better or worse off owning a copy in place of the original (whatever “original” in a digital context may mean).

Compare this to owning an oil painting. If I own a copy of the Mona Lisa, it is a verifiable fact that I don’t own the original (which hangs in the Louvre). Even if my copy is stunningly close to the original, and perhaps more emblematic of Leonardo da Vinci’s technique and brushwork than what’s in the Louvre, provenance (i.e., a thing’s history) will demonstrate conclusively that the painting in the Louvre and not my copy is the original. Moreover, I know that this copy holds vastly less value and influence than the original. That’s just the way it is with physical collectibles, and it applies as well to baseball cards, coins, stamps, etc.

But with a digital collectible, the file anyone owns is indistinguishable from the other copies out there. With physical collectibles, copies are always discernibly different. With digital collectibles, on the other hand, the copies are exact (error correction protocols guarantee as much). So what’s the point in paying extra for a digital collectible that takes the form of an NFT? By Warren Buffett’s logic, if cryptocurrencies are rat poison squared, non-fungible tokens are rat poison to an infinite power.

Not so fast, say proponents of NFTs. The issue is not replication but scarcity. Blockchain technology allows for digital collectibles to be scarce even if they are replicable. Granted, a digital file can always be copied exactly. But a digital file on a blockchain when cryptographically signed by some person or organization of standing (such as Jack Dorsey in tokenizing and then selling his genesis tweet) can be scarce, maintain its scarcity, and thereby achieve value that is negotiable and thus a medium of exchange.

But which blockchain? There are many blockchains. What is to prevent someone from uploading the same NFT on multiple blockchains (less of an issue for now because Ethereum seems to run all the NFTs)? What is to prevent someone, once having uploaded an NFT on a given blockchain, to promise not to upload anymore copies, but then to break the promise and, in effect, increase the print run?

For comparison with real physical objects, consider the woodcuts of Albrecht Dürer. As Dürer produced these woodcuts by repeatedly applying ink to his carved wood blocks and imprinting them on paper, they would become increasingly fuzzy as the wood carving wore away with each successive imprint (real-world entropy again). Even long print runs could therefore meaningfully distinguish earlier from later imprints for Dürer’s woodcuts (the earlier ones being sharper and thus more valuable). Ditto for copies of physical art objects in general.

Digital collectibles, by contrast, can be copied with complete fidelity within and across blockchains. Moreover, they can be cryptographically signed again and again. At best, some sort of social validation can control their proliferation. Thus, in the case of Jack Dorsey’s genesis tweet, it’s not the tweet itself, represented as a digital file, that’s so important in gauging its value as his standing as the founder of Twitter and author of the tweet, and his ability to validate its digital transfer from himself to another party.

But whatever you can do digitally once, you can do digitally again. Unlike physical processes, which typically are irreversible (entropy again), digital processes are generally reversible, and where they are irreversible, there’s often a workaround, such as with a computer game where you simply restart it from any desired point in the history of play. In consequence, we have no technological guarantees that Dorsey’s genesis tweet will not be retokenized by him as an NFT. Instead, the only constraint on proliferation is Dorsey’s promise not to do otherwise and the social norms that would hold him to that promise.

In this introduction, I’ve been unduly negative about non-fungible tokens. There is in fact a core idea underlying NFTs that is potentially powerful and revolutionary. But the devil is in the details, and the details, as they are presently being worked out in the theory and practice of NFTs, are making NFTs into a caricature of what they might be. NFTs such as CryptoKitties, Beeple art, and Jack Dorsey’s first ever tweet are trivial, mediocre, forgettable. Insofar as they aspire to be art, they’re kitsch.

If NFTs are going to have a future, they need to do better.

2 Digital Signatures in Digital Marketplaces

Of course, there’s more to the story. As already suggested, when someone buys a non-fungible token, they’re not simply buying a digital file of some collectible that can be readily copied. So what exactly are they buying? To understand what they’re buying, let’s consider a particular example. Specifically, let’s turn again to the NFT of Jack Dorsey’s first, or genesis, tweet, which he sold for $2.9 million and which back in June of 2021 ranked as the fifth most expensive NFT ever sold. By November 2021 it had dropped to the 20th most expensive NFT ever sold.

Dorsey’s genesis tweet on Twitter, is, like every other digital thing, a digital file. For convenience and ease of display, let’s take his genesis tweet to be the following digital file available here at Expensivity.com: https://www.expensivity.com/wp-content/uploads/2021/05/Dorsey-Twitter-NFT-orig.jpg. Because this is a jpeg file, it can be readily displayed as follows:

Now granted, Dorsey’s genesis tweet was not, at its inception, a jpeg file. It was some sort of Twitter file embedded in the Twitter database. Although he has access to this file, we don’t. Instead, we could focus on the characters that Dorsey punched in on his keyboard to create his genesis tweet. In that case, his tweet could be represented as a text file with a time and date stamp: “just setting up my twttr 2:50 PM Mar 21, 2006.” Any of these digital representations might do. They’re all equivalent for the purposes of transforming his genesis tweet into an NFT.

We now confront the obvious question: what is the magic alchemy that turns any old digital file like this into an NFT potentially worth millions of dollars? You’ve got the digital file that represents the item of interest in its full glory. Indeed, you’ll never find some missing or hidden aspect of that genesis tweet by probing deeper or even getting its author, Jack Dorsey, to reveal some hidden digital layer.

In answer then to the question about what turns any old digital file into an NFT, it is this: what’s needed additionally is a digital signature applied within a digital marketplace. To see what’s at stake with digital signatures, which is the key concept here, it helps to go back a generation or two when people and banks were much more comfortable in signing over checks to other people. I recall about forty years ago having a friend who worked with gang members in the inner city, trying to help them break free of drugs and violence. I happened to have a check that was made out to me when we met one night at church. Rather than cash it and give him the cash for his work with the gangs, I simply signed the check over to him by endorsing it on the back.

Given the signature on the back of the check, my friend was able to cash it, which he did. But if he wanted, he could have signed the back of the check under my name, and given the check to someone else, who could then have cashed it or else signed it to still someone else. Such signing of the check over to others could have continued until room on the check ran out. These days, checks have a horizontal line on the back and an explicit statement that nothing written below that line is valid. But back in the day, you could keep signing the check over to others, in effect turning it into a negotiable instrument.

Digital signatures on a blockchain work in the same way. The blockchain functions as a digital marketplace in which ownership of digital items is transferred from one party (usually called “Alice”) to another party (usually called “Bob”) by Alice applying a digital signature to it and designating Bob as the recipient (assign and sign: Alice is the assignator, Bob the assignee). In a blockchain-based digital marketplace, Alice, Bob, and any other commercial agents each use a public/private cryptographic key. The public key serves as the address to which digital items are assigned, the private key as the way to sign these digital items, authorizing their transfer from one party (or address) to another.

Thus, if Alice wants to sign a digital item over to Bob, she takes the digital item, attaches to it Bob’s address (from his public key), and then signs it with her private key. By signing with her private key, she authorizes the change in ownership of the digital item from herself to Bob, making clear to all members of the blockchain-based digital market that Bob now owns the digital item. And because the digital market is a blockchain, it is a secure, untamperable ledger that reliably records the transaction (at least it’s supposed to be secure; Bruce Schneier argues persuasively that the security of distributed peer-to-peer networks that run blockchains is less than ironclad).

In this account of digital signatures within a digital marketplace, there’s an interesting irony. Even though medium sized physical objects can never be perfectly copied, physical signatures that get attached to such physical objects can often be convincingly faked. Yet conversely, even though digital files of whatever size can be perfectly copied (error-correcting codes ensure faithful copying even for humongous files), cryptographic signatures can get attached to such digital files in ways that uniquely identify the signer and thus cannot be faked (except by a vastly improbable lucky guess of a private cryptographic key, a guess less likely to succeed than the sun failing to rise).

In this account of digital signatures within a digital marketplace, there’s an interesting disconnect between digital ownership and real ownership. When I own a physical item, often it’s close by me and transferring ownership simply means moving it from my hands into someone else’s hands. If it is particularly large, bulky, and valuable, such as a piece of property, transferring ownership will involve signing paperwork with an official recording office, thus ensuring that the transfer has the full endorsement and power of law behind it.

In a real marketplace, even if the property is intellectual property (such as a patent or copyright, whose form can be entirely digital), there will likewise need to be a contractual transfer of the rights to that intellectual property to a new party, with the transfer again having the full endorsement and power of law behind it. For instance, if in making an intellectual property purchase, I acquire the copyright to a picture, even a digital picture, the real market that operates in our society ensures that the transfer is subject to its laws and strictures. Through my purchase, I will own the picture in a real sense and can take legal action against anyone who tries to infringe on my copyright (such as by posting it on a blog without my permission).

By contrast, the concept of owning an NFT on a blockchain is specific to the blockchain with no legal force in the society at large. Suppose I snap a digital photo. Because I’m the one who snapped the photo, US law agrees that I own the copyright to it. Within the real marketplace of our society, I can sell the photo, license it, or just keep it. But suppose I decide to take it, as a digital file, upload it onto a blockchain, and then “sell” it to another party as a cryptographic transfer in a cryptocurrency that runs on that blockchain. This party signs over to me a certain amount of the cryptocurrency and I sign over to that party the digital file, all on the cryptocurrency’s blockchain.

Now answer this: in what sense did I “sell” the digital file? Within the marketplace of that blockchain, as a matter of convention, it could be said that I no longer own the digital photo and the other party now does. So in that sense I sold it. But such conventional reassignments of ownership within a blockchain ecosystem mean nothing as far as the real marketplace and real legal system of our society is concerned. I could, for instance, put that digital photo as an NFT on the Ethereum blockchain, get paid handsomely by you in ether, and then, when you use that photo on your website, sue you and try to collect damages for copyright infringement.

Unless my signing over of the digital photo on the Ethereum blockchain is combined with a parallel signing over of actual copyright in the real marketplace of our society at large, all you can do is negotiate/trade this digital photo (i.e., NFT) on the blockchain where it was uploaded and signed over to you. So you’re in effect stuck on the blockchain where the NFT resides.

Perhaps laws will at some point be changed so that points of sale in the virtual marketplace of the Ethereum blockchain are treated as points of sale in the real marketplace of the society at large, conferring all the rights and guarantees of the real marketplace. But no such transfer of real ownership happens for now in these virtual marketplaces, and there’s no prospect for that becoming the case anytime soon. Even worse, nothing prevents people from uploading the work of others as NFTs and claiming or implying them as their own. One such marketplace, Cent, even shut down because almost all so-called “sales” had become fraudulent: “’bad actors’ had been using Cent to ‘mint’ counterfeit NFTs, which generally involved selling copies of NFTs that didn’t belong to them or creating NFTs of content they didn’t own.”

It’s time to wrap up the review of Jack Dorsey’s genesis tweet and its transformation into an NFT. Since that tweet was essentially a short text with a time and date stamp, there’s nothing here to copyright. Short texts other than poetry can be regarded as having educational value, and thus can be represented and copied at will with no copyright infringement, as a matter of what is called “fair use.”

Specifically, then, here’s what actually happened: Dorsey uploaded his genesis tweet onto the Valuables platform, which served as an auction house for it. The auction house then handed over Dorsey’s signed tweet to the highest bidder, namely, the Malaysian businessman Sina Estavi. The transaction was run over the Ethereum blockchain, with Estavi in early March 2021 paying 1630.5825601 ETH (about $2.9M at the time), 5 percent going to the Valuables platform as a commission and the remaining 95 percent going to Dorsey, who in turn gave his portion to people in Africa impacted by COVID-19.

Anyone besides Dorsey could have taken his genesis tweet and likewise put it up for auction on the Valuables platform or one equivalent to it. Anyone can still do this. Dorsey can do it again, putting his genesis tweet up for sale a second time. What if he did it a second time? Would the second signed version of his genesis tweet sell for a lot less than the first time around? Probably. Would putting it up again devalue the version that Estavi bought? Probably. While NFTs are new, the debasement of value by proliferating copies whose marginal value is close to zero has a long and ignominious history (compare the debasement or Roman coinage in the first centuries A.D.).

3 The Do-It-Yourself Minting of NFTs

The process of creating NFTs, along with buying and selling them, is simple and straightforward. All that’s required is

- setting up a crypto wallet that handles Ethereum cryptocurrency (ETH),

- loading it with some of that currency,

- visiting an NFT marketplace (a third party that accesses the Ethereum blockchain),

- connecting the crypto wallet to that NFT marketplace, and

- create/upload/sell or else buy an NFT by spending some cryptocurrency at the marketplace.

Since it’s always better to actually see how something is done than merely to describe it, I’m next going to provide two helpful YouTube videos and then walk readers through the creation, sale, and purchase of an NFT by me.

3.1 Two How-To Videos on NFTs

The following two YouTube videos lay out “how to do it.” The first is a bit more general, the second gets more into the nuts and bolts of turning art into NFTs. The videos are about 15 minutes each. They’ve had many views. They’re worth watching carefully, not only for the how-to instruction but also to understand the motivations underlying the creation and monetization of NFTs:

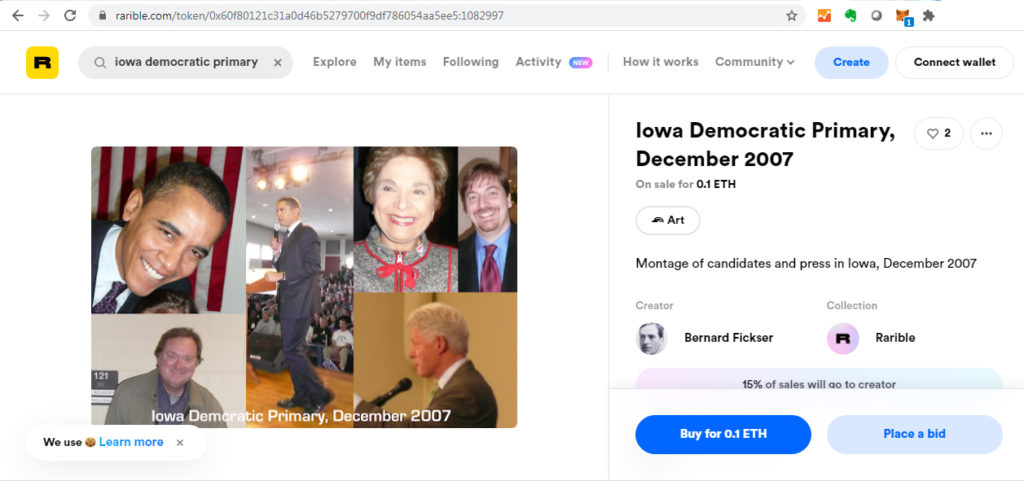

3.2 A Selective Montage of the 2007 Iowa Democratic Primary

The NFT that I’m going to create, upload, and put up for sale will be a montage of the Iowa Democratic primary for the US presidency from over a decade back. As it is, my family was in Iowa in December 2007, and it was a wild time in the lead-up to the 2008 presidential election. My wife and daughter attended numerous rallies and got some great pictures of candidates and press. Here’s a montage of some of the pictures my wife took (many of them were with the candidate or journalist next to my daughter, whom I cropped out for privacy reasons). The associated png source file on this website is given in the caption.

3.3 Turning This Montage into an NFT

Let’s now go step by step in turning this montage into an NFT:

3.3.1 GET CRYPTOWALLET

Get yourself a cryptowallet that can handle ether (ETH). I already had an Electrum wallet for Bitcoin. For ETH, I went with MetaMask: https://metamask.io/. This wallet seems to have a large following. It’s also got an app that works well with my iPhone. Additionally, it integrates readily into Chrome, which is my go-to browser (a point of ambivalence for me given my misgivings about surveillance capitalism).

Using the MetaMask wallet is reasonably straightforward, but do a Google query if you get stuck. For instance, I ran into a problem when it wasn’t clear whether I needed to get into Chrome settings or the MetaMask settings (the latter are not clearly marked and are accessed by clicking on the top right icon).

Once you get your wallet set up, you’ll see a sequence that looks like this (which happens to be the one in my wallet):

0x4f74085dfE2f580BaAb770b0DA9c41E6f38E065F

That’s the public address. It’s readily copied by hovering over it and hitting “copy to clipboard.” You’ll need this address for people to send you ether, to send yourself ether to load onto the wallet, and to pay for setting up an NFT.

Two caveats regarding the MetaMask wallet, and crypto wallets in general, are worth bearing in mind:

- All this convenience with the MetaMask wallet comes at a security cost. For instance, in this age of unbridled surveillance, easy integration of the wallet into Google Chrome seems hardly a recipe for privacy (Google being second in surveillance perhaps only to the National Security Agency). I’m therefore leaving just enough ether in my MetaMask wallet to cover the costs of this exercise of showing how to work with NFTs. So if I lose everything in this wallet, I can live with that. But if you put a serious amount of ether into a cryptowallet, I would probably work exclusively with the Brave browser (given its commitment to anti-tracking) and a VPN. I’d also get a crypto hardware wallet (such as the Trezor or Ledger, available on Amazon). The advantage for security with these hardware wallets is that it keeps you offline as much as possible, limiting attacks from cybercrooks (although not eliminating all attacks because you still need to get online to work with cryptocurrency).

- Be sure to keep good track of your 12-word seed phrase when you set up your wallet. If you lose it, you lose your wallet and everything in it. It’s often suggested that you write down the seed phrase on paper and keep it entirely out of digital reach. But paper is easily misplaced, and the news is filled with people who have lost a lot of cryptocurrency by forgetting or misplacing their seed phrase. Here’s one 2021 headline from Business Insider: “People have lost roughly $140 billion in Bitcoin because they forgot their passwords or got locked out of accounts, and would-be millionaires are struggling to access their wallets.” I therefore prefer to record the seed phrase in an image file, and then hide the image among a plethora of other images where it gets hidden from view unless you know what you’re looking for.

3.3.2 BUY ETH/ETHER

The next thing to do is buy some ETH/ether. The MetaMask wallet tries to make this convenient by allowing you to buy ether directly through Wyre. But Wyre was not supported in my state. So the surer course will be to work through an exchange, buy some ether there, and then transfer the ether to your wallet using your wallet’s public address.

Coinbase.com is the most popular exchange, and I’ve got an account there. But I bought some Bitcoin and Ethereum there in 2016 when the cost of both was ridiculously low compared to today, and I didn’t want to generate a “tax event” by using that account in this exercise of NFT creation. Other exchanges exist and also work well. Kraken.com is solid, but you have to wire money into your account there before you can use it.

Gemini.com (run by the Winklevoss twins) has higher transaction fees, but works quickly with a debit card. I used it in this exercise. Buying and moving the ether from Gemini.com to my MetaMask wallet took maybe two minutes. I had, however, confirmed my debit card beforehand with Gemini.com. For confirmation, Gemini.com made two small reversible deposits into the bank account of the debit card. I then had to verify those amounts with them. This was also handled quickly (minutes, not hours).

3.3.3 VISIT NFT MARKETPLACE

In connecting to an NFT marketplace, you have a range of choices. Popular NFT marketplaces include:

- AsyncArt

- AtomicMarket

- BakerySwap

- Enjin

- Foundation

- KnownOrigin

- Mintable

- MythMarket

- Nifty Gateway

- Open Sea

- Portion

- SuperRare

Some of these marketplaces cover the full range of NFTs, such as Open Sea. Others are more specialized. MythMarket, for instance, focuses on trading cards. SuperRare, as the name implies, strives to be more selective, listing NFT creators only after first accepting them to its platform via an artist profile submission form.

I would urge readers of this article to browse all these sites to get a feel for how these marketplaces work and what NFTs are really like. For me, the overwhelming impression I get from browsing these platforms is that they make a virtue out of promoting ugliness, triviality, insipidness, sensory overload, and unoriginality (notably the kluging and repackaging, via photoshop and similar technologies, of existing digital items).

For a revealing contrast, I would urge readers also to visit the art auction houses of Sotheby’s or Christie’s. Granted, NFTs are now being sold at these auction houses as well, but have a look at this Sotheby’s auction of American art or this Christie’s auction of 19th century European art. Not only are you at these auctions buying unique items of art that cannot be replicated, but once you buy them and take delivery, you own them in every conceivable sense. For instance, once they’re in your possession, you can take photos of them, and the photos will be under your copyright.

In any case, to create my NFT from the montage of photos taken in December 2007 at the Iowa Democratic Primary, I decided to go with Rarible. Rarible is large as these NFT marketplaces go. It requires no invitation to use their services, and set up is straightforward.

3.3.4 CONNECT CRYPTO WALLET

Once at Rarible.com, connect to your crypto wallet by clicking on the “connect wallet” button in the upper right. If you’re using Chrome, MetaMask will be the first option you see. Connect to this wallet if you have it. Otherwise use a different wallet. If you’re in another browser such as Brave, Rarible will give you options for connecting a non-MetaMask wallet. Use one of those options.

First time around, you’ll be asked for a MetaMask password or you may be asked for your entire seed phrase. Once you get your wallet connected, set up a profile in your name with Rarible. The profile requires just a few items, and you can edit it later at your convenience.

3.3.5 CREATE OR BUY NFT

With your wallet connected and some ether in it to cover costs, now either create a new NFT at Rarible or else buy an existing NFT. We’ll do both.

To create an NFT, I’ll use the png above that’s the montage of politicians and press at the 2007 Iowa Democratic Primary. The image file is about 2MB. To turn this png into an NFT, hit “create” in the upper right menu at Rarible. You then need to hit either “single” or “multiple” depending on whether you want a one-of-a-kind NFT or one that has a fixed number of copies. For my NFT, I chose “single.”

Next, upload your image or other digital file. I uploaded my png, and then filled out the requested information. I chose “fixed price” and set the price for this NFT at .1 ETH, or by today’s exchange rate at about $230. You could also have gone with a timed auction in which you set a minimum price and time for the auction (much as at eBay). You could as well have chosen an unlimited auction (which is unexplained on the site but means an auction that simply runs until you call it). And finally, you have the option of uploading the NFT but not putting it up for sale.

Title and description of my NFT were at my discretion. I titled it “Iowa Democratic Primary, December 2007.” I went with a 15 percent royalty, so that whenever the NFT is sold subsequently, I’ll see 15 percent of the selling price (10 percent seems to be the default). With regard to choosing the collection (ERC vs. RARI), I went with RARI since it was the easier option (the ERC option required some additional identifiers for putting the NFT on the Ethereum blockchain).

Finally, there’s the issue of lockable content. For simplicity, I went with not activating the “unlock once purchased” option. By not activating this option, I made the full png of my NFT available at Rarible, as you can see here (the png that Rarible exhibits is thus identical with the one on this website given above):

https://rarible.com/token/0x60f80121c31a0d46b527

9700f9df786054aa5ee5:1082997?tab=details

But I could also have gone with the option to “unlock once purchased.” The result of doing so is explained on the Rarible FAQ page:

As a content creator, you can add unlockable content to your collectibles, that only becomes visible after a transfer of ownership (i.e. selling or gifting your NFT). Artists use this feature to include high res files, making ofs, videos, secret messages, etc.

By uploading the digital file that’s being transformed into an NFT and then answering the other questions, you now just need to hit “create item.” From there it’s simply a matter of telling your wallet to authorize three steps: 1) mint, 2) approve, 3) set fixed price. The first two of these will debit your crypto wallet, which for me came to about $23 in ETH given the exchange rate that day. Once you complete these authorizations, your NFT will be created. Mine is at the Rarible link given above. Here is a screenshot:

That’s all there is to creating a new NFT. So long as you have a compatible ETH-based wallet with sufficient ether in it, and so long as the digital file that you are turning into an NFT is readily available for upload, creating a new NFT is straightforward and takes but a few minutes.

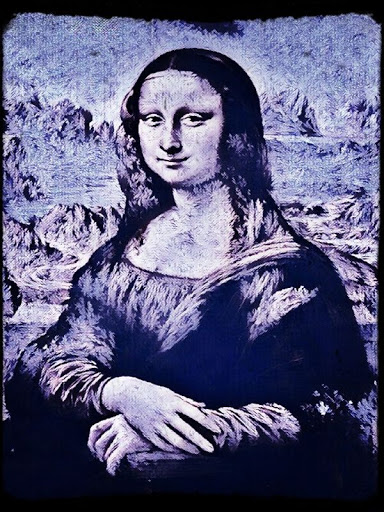

Finally, buying an NFT is even simpler. Because I’m deeply skeptical of what ownership of NFTs on the Ethereum blockchain even means, I decided to go with the cheapest NFT I could find at Rarible. This was the following image of the Mona Lisa:

The stated cost was .003 ETH, which at the rate of exchange at the time came to about $7. But there was also a .0063 ETH “gas fee,” which is the service cost paid to Ethereum miners for inputting transactional information onto the Ethereum blockchain. By the exchange rate at the time, that came to another $15, so that buying this NFT ended up costing me three times its asking price ($22). For the time being, I’m not putting this NFT up for sale.

In one respect, creating an NFT proved more straightforward than buying an NFT. Once I hit “create item,” the NFT I created (the Iowa montage) got registered under “my items” on the Rarible site almost immediately. On the other hand, when I bought the Mona Lisa NFT, I saw an animation with confetti congratulating me on the purchase, but when I looked under “my items” on the Rarible site, I didn’t see anything related to the NFT until about half an hour later, at which point my ownership was finally acknowledged.

So in the interim between attempting to buy the Mona Lisa NFT and actually taking possession, there was nothing I could find on the Rarible site to indicate that my purchase had gone through or that my possession of the NFT was pending (thus causing me to wonder if the purchase was successful at all). So, presumably, it wasn’t until the Mona Lisa NFT was fully transferred to my address on the Ethereum blockchain, about half a hour later, that my purchase appeared under “my items” at Rarible. Be aware, therefore, that purchases of NFTs may experience a lag of the sort that we’re not used to with conventional vendors (such as eBay or Amazon).

4 What Just Happened?

The creation and purchase of an NFT as described in the last section raises a lot of interesting—and troubling—questions. It’s easy enough to go with the flow and simply load a crypto wallet with the ether needed to create or buy an NFT, and then do what you need to get the NFT you want. But NFTs are supposed to impart some sort of ownership, whether it be full possession in a real-world sense or even a partial claim that nonetheless has real traction.

In fact, ownership of NFTs is much more tenuous than such conventional understandings of ownership suggest. I therefore want next to reflect on what the creation and purchase of NFTs as outlined in the last section reveals if we probe beneath the surface. On the surface, a site like Rarible looks like eBay (though not nearly as extensive or sophisticated). But in fact, something very different is going on.

4.1 No Limit on Proliferation, No Guarantee of Scarcity

If I put up a real physical item for sale at eBay, I can only put up as many items as I actually possess. For instance, if I’ve got three items of the same widget, then I can sell no more than three of them. But with the NFT that I created (i.e., the montage of photos from the Iowa Democratic Primary), I can retokenize it at will and ad nauseam. I can go to Rarible and simply re-upload the png of that montage, pay the service fees, and have it reappear as an NFT. I can keep doing this at Rarible as many times as I like. And so I can put up for sale as an NFT the same png as many times as I want to repeat this exercise.

I can also redo this NFT not as a “single” but as a “multiple” NFT where I specify the number of copies buyers can purchase of it. The analogy here is with a limited edition of baseball cards, where buyers can only buy so many copies until they’re gone. But just as with baseball cards, where you can always do a second print run, you can always do a second print run with such “multiple” NFTs. In fact, it’s even easier with NFTs because it’s all digital. And because Rarible imposes no limits on what its users can upload as NFTs (short of pornography or hateful content that violates clear guidelines), I could hit “multiple” in retokenizing my NFT multiple times. I could also mix and match “single” and “multiple” any way I like.

And, of course, I don’t have to stay with Rarible. Having saturated Rarible with my NFT of the Iowa Democratic Primary, I could go to any other NFT marketplace that requires no prior approval of its users, and do the same exercise there, uploading the png of the Iowa Democratic Primary there as an NFT. Granted, word of my unbridled proliferation of the same NFT might get around and ruin any chance of turning a profit with it. But that’s not the point.

The point is that such unbridled proliferation, with its assault on scarcity, has no technological solution (though it may have a sociological solution—see subsection 4.4). Note that I don’t have to be so wooden-headed in approaching the proliferation of my NFT as in simply replicating the NFT with no plan or purpose. Suppose my NFT, with just one copy in existence, sold for a good price. There’s nothing to prevent me as its author from then retokenizing it in an effort to get a better return but thereby ruining the market for it. From a technological or feasibility standpoint, the only constraint on my retokenizing an NFT is the service costs.

4.2 Where Is My NFT?

In his book Cybernetics, the mathematician Norbert Wiener remarked that “information is information, not matter or energy.” True enough, but information that makes a difference in the real world is not disembodied information; it is digitized data that resides on real physical hardware run by software written by human programmers.

So where is my NFT? The usual answer is: On the Ethereum blockchain. But although all Ethereum-based NFTs (which includes just about every NFT at this time) have some toehold in the Ethereum blockchain, to say that they’re on the Ethereum blockchain is almost never the complete answer, and can be highly misleading. Some NFTs do reside entirely on the Ethereum blockchain, such as CryptoKitties, for which ongoing expenditures of ether are needed “to fuel transactions, which include purchasing and breeding CryptoKitties.”

But the fact is that the Ethereum blockchain, even though it can function as an all-purpose computer (i.e., Turing machine) and thus act as a database, it is not adapted for large-scale storage. “Gas,” the intermediation fees to do anything on the Ethereum blockchain, can mount quickly, and there are also limits to how much gas can be spent in a transaction block.

One calculation suggests that it would require 66 blocks, given an average block time of 13 seconds, and thus 14 minutes to upload one megabyte onto the Ethereum blockchain. My NFT of the Iowa Democratic Primary was about 2 megabytes, and thus would have required almost half an hour to upload, along with large gas fees. Accordingly, one comprehensive guide to NFTs remarks, “most projects store their metadata off-chain simply due to the current storage limitations of the Ethereum blockchain.” (Metadata here would include my png montage of the Iowa Democratic Primary.)

As a consequence, all the actual content of an NFT—in other words, what makes it collectible, artworthy, or of any interest—will typically reside off the Etherium blockchain. But where? In the case of the NFT I created at Rarible, it will reside (big surprise) at Rarible, with what’s on the Ethereium blockchain simply registering the NFT and pointing to Rarible for the png that’s at the heart of this NFT.

So my NFT, to exist at all, must reside in two places, namely, the Ethereum blockchain AND the Rarible website. If either fails, I lose my NFT.

4.3 How Secure Is My NFT?

Not very. Most NFTs, as just noted, have to reside in two places at once and face the danger that if either place of residence fails, the whole NFT fails. If the entire NFT could be uploaded onto the Ethereum blockchain, despite its storage limitations, that would be better. But even leaving aside that NFT metadata may reside off the Ethereum blockchain, the long-term prospects for the health of the Ethereum blockchain, considered in and of itself, don’t inspire confidence.

4.3.1 Why Trust Ethereum?

Ethereum’s history of hard forks, including the one that caused the split into Ethereum (ETH) and Ethereum Classic (ETC), is troubling, suggesting that a cadre of miners, and especially Ethereum’s founder Vatalik Buterin, far from democratizing and decentralizing the Ethereum blockchain can, when push comes to shove, do anything they like with it. Additionally, there’s the worry that miners will lose motivation and no longer service the blockchain. That seems unlikely for now, given current enthusiasm for Ethereum, but if you’re thinking of NFTs as a long-term store of value, the prospect that the peer-to-peer distributed network that runs Ethereum may at some point run out of steam (or should I say gas) needs to be taken seriously.

Perhaps the biggest concern for me personally with tying NFTs to the Ethereum blockchain, or indeed any blockchain running a cryptocurrency, is that it presumes that blockchain technology is the final point of evolution in cryptocurrencies, and that Bitcoin and Ethereum will never face displacement by newer and better technologies. To hear some enthusiasts of blockchain describe it, blockchain is the greatest invention since the wheel. But a blockchain is simply a ledger that resists tampering. Ledgers have been around for centuries, and securing them against tampering has likewise been a point of concern and redress for centuries. In any case, securing them by blockchains, though useful, does not constitute an infinite value-add, as it’s often portrayed.

So what happens if a better technology comes along for doing cryptocurrencies? I have some ideas, and I’ll offer some possible directions at the end of this article in attempting to put NFTs on a firmer foundation. But even if my proposals hold no water and if the prospects for a replacement technology remain for now completely murky, the concern that we’ve not reached the final technology for cryptocurrencies should give us pause. In the history of technology, paradigm shifts are common. Many tech companies that were behemoths a generation or two back have gone the way of dinosaurs.

One last point about blockchain technology: the ability of create novel blockchain-based cryptocurrencies at will and ad nauseam ought also to give us pause. Bitcoin and Ethereum for now have a prime-mover advantage. But what can be digitized can be redigitized. As of April 2021, there were 10,000 blockchain-based cryptocurrencies. Even if individual cryptocurrencies can build scarcity into themselves by limiting the total supply of coins (such as Bitcoin’s 21 million upper limit), the proliferation of cryptocurrencies by simply building new blockchains knows no such limitation or scarcity. If you haven’t done so, scroll down the cryptocurrencies listed at CoinMarketCap to appreciate how readily blockchain-based cryptocurrencies have proliferated.

4.3.2 Why Trust NFT Marketplaces?

Perhaps you have good reasons to think that my worries about Ethereum are unfounded. In that case, you should still be concerned about the NFT marketplaces that help “host” your NFT. (The word “host” here should set off alarm bells. We don’t think of a bank, for instance, as “hosting” our money. But NFT marketplaces, as we’ll see momentarily, host NFTs with no obligation or liability.) So, even if your NFT remains unproblematic insofar as it resides on the Ethereum blockchain, because your NFT is a dual resident that also resides at an NFT marketplace, you want some assurance that it is secure there as well. Unfortunately, no such assurance is forthcoming. Quite the contrary.

As emblematic of the security concerns you face at NFT markeplaces, I’ll focus on Rarible, which is where I created and bought the NFTs described in the last section. Although we’ve grown accustomed to automatically approving the terms and conditions required to use an online service, in fact you need to carefully read the “Rarible Terms and Conditions” if you are serious about preserving your interests there in creating and purchasing NFTs. In fact, once you’ve read these terms and condition, there’s no way you can be serious about preserving your interests there in creating or purchasing NFTs.

The crucial thing you’ll find in reading these terms and conditions is that Rarible is a platform, much like Facebook or YouTube. You can put stuff up on these platforms, but the platform assumes no liability (repeat, NO LIABILITY, NADA!) for what can happen to your stuff once there. What’s more, at its discretion the platform can entirely remove your stuff. Here’s one relevant passage:

Rarible Company may from time to time remove certain Collectibles from the Rarible Apps or restrict the creation of Collectibles on the Rarible Apps in Rarible Company’s sole and absolute discretion, including in connection with any belief by Rarible Company that such Collectible violates these Terms or the terms and conditions or privacy policy of the Rarible Apps. Rarible Company does not commit and shall not be liable for any failure to support, display or offer or continue to support, display or offer any Collectible for trading through the Rarible Apps.

Later, the Rarible terms and conditions document makes the same point even more starkly:

Rarible May Deny Access to or Use of the Offerings. Rarible Company reserves the right to terminate a User’s access to or use of any or all of the Offerings at any time, without or without notice, for violation of these Terms or for any other reason, or based on the discretion of Rarible Company. Rarible Company reserves the right at all times to disclose any information as it deems necessary to satisfy any applicable law, regulation, legal process or governmental request, or to edit, refuse to post or to remove any information or materials, in whole or in part, in Rarible’s Company sole discretion. Collectibles or other materials uploaded to the Offerings may be subject to limitations on usage, reproduction and/or dissemination; Users are responsible for adhering to such limitations if you acquire a Collectible. Users must always use caution when giving out any personally identifiable information through any of the Offerings. Rarible Company does not control or endorse the content, messages or information found in any Offerings and Rarible Company specifically disclaims any liability with regard to the Offerings and any actions resulting from any User’s participation in any Offerings.

These are essentially the terms and conditions of a Facebook or YouTube. Only with Facebook or YouTube, you’re not plunking down any cash. You’re simply uploading material to your account, and there’s the danger that this material may get removed or that your account may get terminated. Ditto with Rarible. Only at Rarible, you are creating and buying NFTs for serious money. Check out, for instance, Beeple Round 2 Open Edition at Rarible (as of June 2021), with offerings valued in the six figures (in US dollars given the current ETH spot price).

Now it’s true that Rarible could not stay in business long if it willy-nilly started taking down or taking over its customers’ NFTs. But it can legally do with NFTs what banks would be held criminally liable for if banks attempted the same thing with their customers’ money. You may be able to profitably wheel and deal in NFTs at Rarible for a while. But for how long? Rarible gives all appearance of a game of musical chairs in which everything proceeds happily until the music stops. Or, to change the metaphor, it’s like Russian roulette. You may enjoy the excitement for a time. And perhaps getting caught up in the excitement is all that matters to you.

A final point to consider about the instability of NFT marketplaces is link rot. Even if an NFT marketplace guaranteed that your NFTs would remain on its site forever, the fact is that such marketplaces are businesses, and businesses can fail. Even with the best of intentions, an NFT marketplace may simply not be able to make good on its intention to keep your NFTs alive. The Wikipedia definition of link rot is pertinent:

Link rot is the phenomenon of hyperlinks tending over time to cease to point to their originally targeted file, web page, or server due to that resource being relocated to a new address or becoming permanently unavailable.

The problem of link rot is real. The average lifespan of a web page as of March 2021 is 2 years and 7 months. Hence the emergence of such organizations as the InterPlantetary File System (IPFS). Addressing the short average lifespan of web pages, and its efforts to prevent them from being “gone forever,” IPFS states on its about page: “It’s not good enough for the primary medium of our era to be this fragile. IPFS keeps every version of your files and makes it simple to set up resilient networks for mirroring data.”

IPFS has therefore identified a legitimate concern and is attempting to redress it. Rarible is not only aware of this concern but has even contracted with IPFS to store its collectibles. So Rarible is on it, yes? Unfortunately, there’s still a problem. Here’s what Rarible writes about IPFS in its terms and conditions document:

The Collectible Metadata for Collectibles created through the Rarible Applications are typically stored on IPFS through an IPFS node operated by Rarible Company. The Collectible Metadata for Collectibles created outside the Rarible Applications may be stored in other ways, depending on how such Collectibles were created.

So far so good. But later in the terms and conditions document is not so good:

Collectibles created on Rarible have their Collectible Descriptors stored on the IPFS system through an IPFS node operated by Rarible Company, but Rarible Company cannot guarantee continued operation of such IPFS node or the integrity and persistence of data on IPFS.

So good luck ensuring the permanence of your NFTs.

=====ADDENDUM, LATE FEBRUARY 2022=====

Since this article was first written half a year ago, NFT marketplaces have seen an increasing rise in fraud. Because these marketplaces use proprietary software that runs on servers outside the crypto blockchain supporting their financial transactions, thieves have become increasingly clever and successful at stealing NFTs by hacking such software. One common ploy is to gain access to the ability to list for sale a prized NFT, relist it for virtually nothing, buy it for that ridiculously low price, and then sell it at full price (it’s like changing the price tag of an item so that it sells low, and then reselling if for its actual price). One victim of this scam, Timothy McKimmy, is now suing Open Sea (an NFT marketplace mentioned earlier in this article) for $1 million, claiming it knew of the bug that allowed his NFT to be bought and resold in this way but did nothing to fix it. Because hackers were able to exploit this bug, McKimmy was relieved of a “Bored Ape” NFT (a comparable one sold to Justin Bieber for $1.3 million).

=================================================

4.4 Does Creating/Buying NFTs Make Business Sense?

For NFT users with a large social media following and a short time-horizon, I can see NFTs making business sense: get in and cash out; pump and dump. But for an NFT Joe Schmoe like me, NFTs make little business sense. We’ve already seen that the service fees needed to do anything, whether in creating NFTs or in buying them, entail a cost of about $20 given the current spot price of Ethereum. That just seems out of hand given the absence of such service costs at conventional vendors like eBay or Amazon.

True, one might argue that credit cards impose a hidden service cost, so conventional vendors are always handing us those costs without making it obvious. But then again, there is also the service cost of simply loading one’s wallet with cryptocurrency. And then there’s just buying the cryptocurrency at an exchange (before transferring it to your wallet): there’s always a cost in exchanging one currency into another, and that includes changing fiat currencies into cryptocurrencies.

I also saw the price of Ethereum drop about 8 percent from the time I bought it to the time I created and purchased the NFTs described in the last section (in line with cryptocurrency volatility, it’s gone way down and way up since). Maybe I would feel more positive had the price of ether gone up from the time I bought it to the time that I completed this exercise, but at every point in the 5-point process for creating NFTs described in section 3, I had the sense of being bled.

And then there are the commission costs. Conventional vendors like eBay and Amazon charge commission costs. But commission costs also exist at NFT marketplaces, on top of the service costs simply to upload a new NFT (create one) or move one to your items (buy one). For instance, Rarible’s Must Read Guide for People New to NFTs states that for each transaction “Rarible takes a commission at the very end; it’s 2.5% on each end, so 5% of final sale price.” Ouch.

Laying aside all these costs, what happens once you upload and create an NFT, putting it under “my items”? What about buying an NFT and putting it under “my items”? Good luck with any potential buyer finding it. Take my montage of the Iowa Democratic Primary. Its exact title at Rarible is “Iowa Democratic Primary, December 2007.” Suppose I punch in “Iowa Democratic Primary” and hit enter using Rarible’s search feature. A panel of NFTs at Rarible appears, and you’d think that my NFT should get pride of place, situated in the upper left as the first thing that users making that search should see.

But my montage is nowhere to be found on this search output panel. The very first NFT that appears is titled “Crypto Drinks” and shows an iPad displaying a bottle of beer. There’s an NFT titled “Crying Assange.” There are a bunch of NFT with representations of Bitcoin. Everything I see in response to my search is irrelevant to it. There’s absolutely nothing in the search panel that even hints at my NFT.

The only way that I’ve been able to get to my NFT at Rarible is by punching in the title “Iowa Democratic Primary, December 2007” or some portion of this phrase into the search bar and then, instead of hitting enter, I need to be attentive enough to see that the search bar has dropped down and is suggesting my NFT. I then have to click on that drop down link to get to my NFT.

Perhaps it’s just that search in these NFT marketplaces is primitive right now and that down the line it will get better and be able to compete with the mature search capabilities of an eBay or YouTube. But I’m not holding my breath. I suspect the inadequacy of search at Rarible is baked into the system to promote NFTs that are likely to sell and thus lead to more commissions for Rarible. Rarible’s homepage highlights the NFTs they want to highlight: “top sellers,” “live auctions,” “hot bids,” “hot collections,” etc. Leaving aside the merits of my NFT (minimal as they are), my NFT never had a chance. In fact, it’s only chance is that someone will read this article and want to buy it.

=====ADDENDUM JULY 26, 2021=====

The searchability of my NFTs at Rarible has improved since I wrote about it last month (see immediately above). But the searchability there is still not great. Presently, searching on my name and on the name of my NFT does show the right items on a search results page, but still not at the top, where it should be. One still gets the sense that my NFTs are being buried among the NFTs that Rarible is trying to promote.

=====================================

But, someone may retort, people are making good money creating and selling NFTs. Just because Joe Schmoes like you, who create NFTs in an uninspiring exercise, can’t make any money with them doesn’t mean there isn’t a business model here that can’t thrive. Such optimism about NFTs is misguided. Certainly, the other concerns raised earlier in this section should dampen such optimism. But let’s examine this optimism more closely and see why it is unjustified.

The premier NFT marketplace for now is SuperRare. This is the place to be if you’re an artist who wants to put your NFTs up for sale and get the best prices for them. So, what does it take to be an artist at SuperRare? To answer this question, SuperRare’s Help Center is particularly helpful and revealing. Unlike Rarible, where anybody can create and trade NFTs, SuperRare is by invitation only. Artists in SuperRare’s stable need to fill out an application form and then be approved. What is SuperRare looking for in the artists it accepts into its stable? The answer is found on the SuperRare page titled “Tips for Getting Accepted as an Artist on SuperRare.” The tips include the following (these are all direct quotes):

- Be able to prove your identity as original artist. [SuperRare wants] to make sure we are protecting our collectors by ensuring all artworks tokenized on the platform were actually created by the artist that tokenized it.

- Promote your art on social media! We’ve seen very clearly that the artists doing a good job of promoting themselves and their art on social media sites like Twitter/Instagram/Cent are the ones that attract the most collectors on SuperRare.

- Have an original, consistent style. [T]he artists that do the best on SuperRare are the ones that focus on being original and having a consistent look & feel.

- Scarcity Scarcity Scarcity. We take scarcity very seriously, and we’re strong believers that the artists spending more time on creating the best possible works of art do far better with collectors, rather than flooding the market… Are you tokenizing multiple artworks every day? Or are you spending more time creating and tokenizing better artworks less frequently? … We’re more inclined to accept artists with a lower total supply of existing artworks than artists that have already tokenized hundreds of works across multiple platforms.

The things that SuperRare is looking for and desiring in its artists make perfect sense. In fact, if NFTs as currently structured at NFT marketplaces are to have a future, then NFT artists will need to address and satisfy the concerns raised in these points.

The interesting thing to note about these points, however, is that they don’t admit technological solutions. Where is blockchain here? A big motivation for Satoshi inventing blockchain was to allow for anonymous transactions, but here we find SuperRare wanting to prove identity. To the second point listed, promoting art effectively on social media likewise feeds into this anti-anonymity. So too, the question of style and branding is personal, reflecting the artist’s work and not its technological implementation.

The last point about scarcity goes to what I’ve been saying right along in this article, which is that NFTs can be proliferated at will. The technology allows such proliferation. In fact, the only thing that can disallow it is integrity and trust, integrity on the part of the creator of the NFT (especially the commitment not to proliferate it) and trust on the part of the buyers (that the creator and marketplace will stand against proliferation and thus ensure scarcity).

If NFTs are to make any business sense, the question of proliferation and scarcity needs to be addressed in earnest, especially as these relate to value and ownership of NFTs. We turn to these topics next.

5 Digital Scarcity

When jumping into the world of NFTs, one finds a certain breathless awe in the face of blockchain technology. One even hears that blockchain has for the first time made if possible to create digital scarcity, as though scarcity of physical goods is the only type of scarcity that existed before blockchain was invented. Such a claim is both misleading and ludicrous.

First off, it bears repeating that blockchain is a ledger security technology. In other words, its whole point is to keep ledgers secure from tampering. But ledgers have been kept secure by various means for centuries. Notarization using time-date stamps along with attestation by witnesses is old and well proven. It is still used to set up bank accounts and to buy and sell property. Independent accountants who keep parallel books provide another form of security (if the books don’t match, there’s been a mistake or tampering). I’m not saying these are best or foolproof, or that blockchain may not be better. I am saying there are alternatives.

The use of peer-to-peer distributed systems to implement blockchain should not be regarded as a magic bullet. Such systems constitute third parties, and the claim that they don’t require trust (i.e., that they’re “trustless”) is naive. Blockchain technology is consensus based, which in practice means majority rule (the slogans “decentralized” and “democratic” supposedly providing legitimation). But the problem with majority rule is that the majority can do anything it wants.

What, then, is digital scarcity? In the physical world, scarcity is obvious and looks like this: There are only a fixed number of items answering to a given criterion or specification. Take, for instance, barrels of crude oil. There are only so-many-so many produced on a given day. There are only so-and-so many that can be produced on a given day given maximal production. In the state of California or Texas there are only so many barrels that can be extracted to the end of time. Note that scarcity for physical items comes in degrees and admits numerical comparisons. If the criterion for scarcity is weight, then diamonds are scarcer than crude oil.

What, then, does digital scarcity look like? Given that a digital item is just a file consisting of bits that can be copied with complete fidelity once the full file is in hand, digital scarcity cannot mean a limit on the number of such copies, since there can be no such limit for digital files. Scarcity must therefore mean some limitation on the digital file in question, limiting access to it or the ability to make certain changes to it. Moreover, such limitations can only arise as the originator of the file by bakes in such limitations from the start. Digital scarcity therefore can only mean one of three things (these are exhaustive though not mutually exclusive):

- Partial Availability. The full digital item is unavailable but instead only a partial form of it is available, whose copying or use is regarded as unproblematic. The partial form of the digital item thus constitutes an approximation of or limited access to the full item, the full item being kept inaccessible except to certain authorized parties.

- Digital Marking. The digital item is marked in such a way as to identify the author of the mark or otherwise distinguish it. The mark can be hidden, invisible to people viewing the item, though becoming plain once it is pointed out. Or the mark can be evident from the start. Scarcity of the item may consist of the presence of the mark or its absence.

- Algorithmic Immutability. The digital item is the output of an algorithm whose operation has followed a clear and verifiable path, and there’s no way to change the output given the history of the algorithm’s behavior to that point.

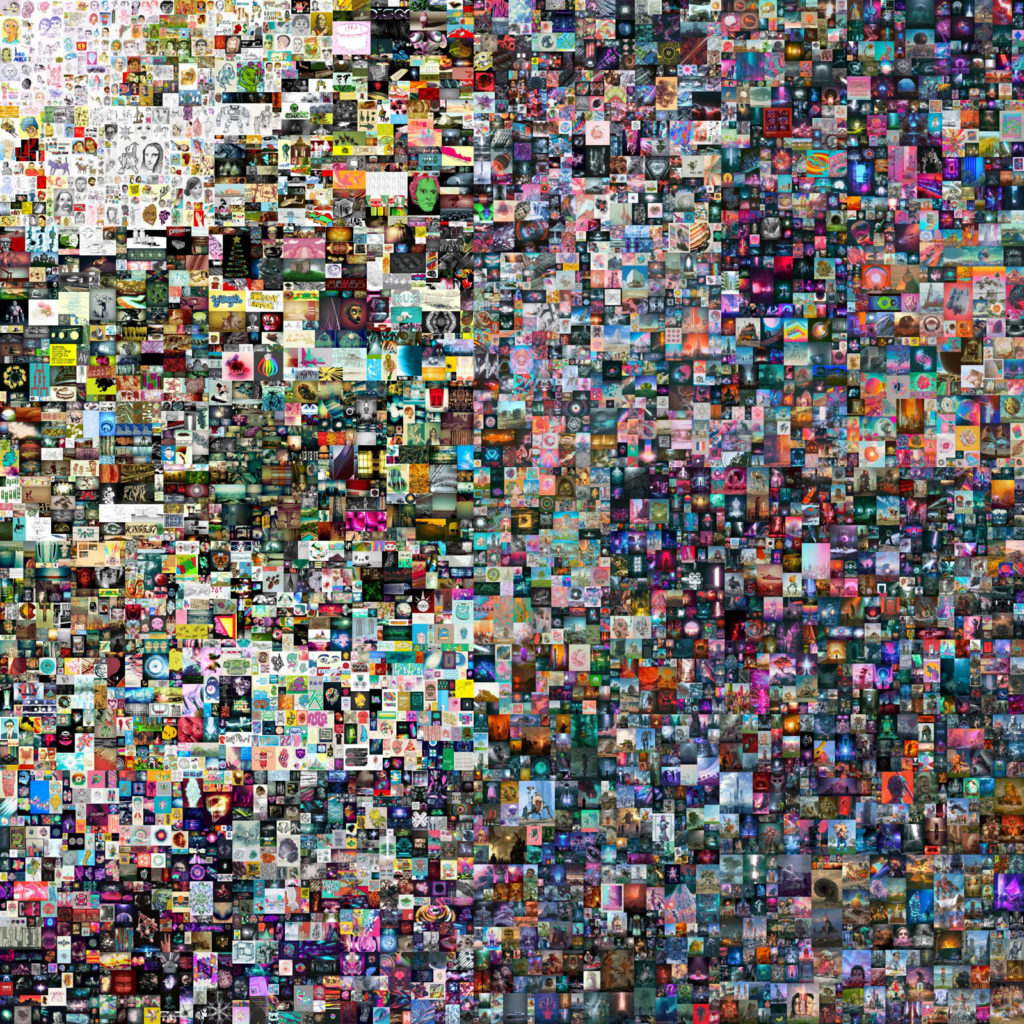

To illustrate these three points, I’m going to review the sale of the artist Beeple’s (aka M.J. Winkelmann’s) NFT titled Everydays: The First 5,000 Days. This is the highest priced NFT ever sold, selling on March 11, 2021 at Christie’s auction house for 42,329 ether, which at the time amounted to over $69 million.

The above representation of Everydays: The First 5,000 Days is a 1,600 x 1,600 pixel jpeg image. As such, it is a low-res partial image of this digital work of art. The jpeg above is just a little over 1 megabyte. The full image that was on sale at Christie’s came to 21,069 x 21,069 pixels and weighed in at over 319 megabytes. This full image was part of the Christie’s sale and went to the winning bidder, namely, Vignesh Sundaresan (aka MetaKoven).

This disparity between a partial jpeg image of Everydays, which was used by the auction house to represent the work of art to potential bidders, and the full image that constitutes the actual work of art, illustrates the partial availability form of digital scarcity. The full image also raises some interesting questions of its own. It’s certainly large as jpeg images go (over 319 megabytes). But as a collage of 5,000 images (one created everyday by Beeple since 2007), it actually does little justice to the original images.

If you visit Beeple’s website, you will find individual jpeg images of the sort that Beeple used to populate the Everydays collage—the types of images that he produced one a day over 5,000 days. These images are on average about 3 megabytes. So if Everydays fully represented each of the images in the collage, the file size should have come to 3 megabytes x 5,000, or about 15 gigabytes, or about 50 times the size of the image that was put up for sale. As it is, each image making up the collage can have only about 319 megabytes ÷ 5,000 on average, or just under 64 kilobytes. The purchaser of this collage might therefore have insisted on including in the sale all the individual images making up the collage.

If the winning bidder Vignesh Sundaresan was only interested in acquiring the 21,069 x 21,069 pixels jpeg image of Everydays, and if that’s what he paid $69 million for, he would be playing a dangerous game. Individual self-contained files are easily hacked and copied. For his purchase to be safe and make any sort of sense, there had to be more to it than simply this large jpeg file, and there was.

This takes us to the second form of digital scarcity listed above: digital marking. The purchaser of Everydays, in addition to receiving the full high-res jpeg of this digital work of art, had it signed over to his Ethereum address by Christies once he paid for the work in ether. It’s that cryptographic signature consistent with Ethereum protocols that’s the value-add here and what Sundaresan ultimately paid for.

Because the actual work of digital art was too storage-intensive to put on the Ethereum block chain, storage of the work had to be put in one place and its signature on the Ethereum blockchain in another place, with a pointer connecting the two. But conceptually, what the Sundaresan purchased was a signed version of Beeple’s Everydays, signed by Christie’s and assigned to Sundaresan. This signed assignment of the work constituted a digital marking. Only Christies could impose that digital marking with itself as the assignator and Sundaresan as the assignee.

Note that digital marking is not confined to cryptographic digital signatures. The field of digital data embedding technologies (everything from watermarking to steganography, which introduces hidden messages into digital files having a clear surface meaning) also answers to this form of digital scarcity. Thus via steganography one might adjust pixels in a jpeg image so that they spell out some message (e.g., “this is not the original file”) or one might watermark it as a sign of authenticity or inauthenticity. This is well trodden territory and it predates blockchain.

The final form of digital scarcity to be considered is algorithmic immutability. It obviously calls to mind blockchain, where a well-defined peer-to-peer software implementation of a blockchain protocol (which constitutes the algorithm) can only produce outputs consistent with prior blocks. Cryptocurrencies clearly need algorithmic immutability because you can’t just have new coins emerging from nowhere.

At the same time, it’s hardly the case that blockchain is the only way to achieve algorithmic immutability. The current state of a system may be reliably determined without blockchain technology (perhaps by such low-tech means as attestation by human witnesses), whereupon the algorithm operates as it must. Our present banking system, without the aid of blockchain, operates by algorithmic immutability.

Beeple and Christie’s together ensured that Everydays would reside on the Ethereum blockchain, thus also conferring algorithmic immutability as a form of digital scarcity onto this work of art. But as with partial availability, this form of digital scarcity seems less essential to what makes Everydays valuable. If the full 319 megabyte jpeg of Everydays suddenly appeared online, Sundaresan would still own the image in the sense that he would be the winning bidder in the auction for it and Christie’s would be signing it over to him and no one else.

That it was signed over to him on the Ethereium blockchain, or any blockchain for that matter, seems unessential. Christie’s and Sundaresan, for instance, could each have set up a private/public cryptographic key for themselves, and Christie’s could then have signed over Everydays from its key to Sundaresan’s. The public keys and the signing over of the artwork using private keys would have been noted far and wide given all the public attention to this sale, and Sundaresan could have paid for it in any currency mutually agreed upon by the buyer and auction house. Blockchain could thus have been sidelined.

This last point may seem counterintuitive and even absurd given the current hype over blockchain in cryptocurrencies and NFTs, but I’ll justify it more fully in the next two sections. For now, however, it remains the case that all three forms of digital scarcity outlined in this section appeared in the sale of Beeple’s Everydays.

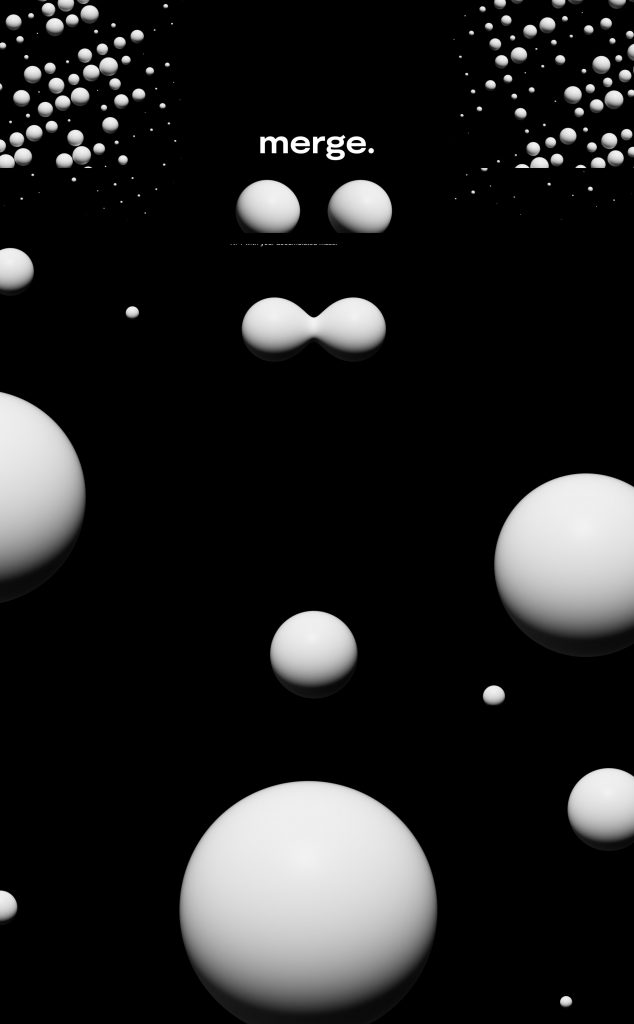

POSTSCRIPT: The world of NFTs moves quickly, and since this article was published at Expensivity in June of 2021, new high-priced NFTs have sold. The current record on Wikipedia’s list of the most expensive NFTs now puts anonymous artist Pak‘s The Merge ahead of Beeple’s Everydays. Thus, on December 4, 2021, The Merge was sold by Pak on the Nifty Gateway marketplace for $91.8 million, exceeding Beeple’s Everydays by over $22 million. But this sales price for The Merge needs elaboration, and by any conventional understanding of the sale of collectibles, Beeple’s Everydays may still rightly be regarded as the most expensive NFT ever sold.

Pak, through a device he called “mass,” in essence sold equity stakes in The Merge. Unlike Everydays, which had a single buyer and a single NFT owner (ownership in the sense of blockchain rather than real legal ownership), The Merge had 28,983 investors (or collectors), with each owning on average ten units of mass. Pak, through this device of “mass,” was pushing the envelope of NFTs. Each owner of mass got some variant of The Merge, so NFT ownership here was not of a static collectible but of a dynamically changing collectible that adapts itself to the amount of mass purchased (in the spirit of hucksterism, Pak even offered a “buy ten units of mass and get one free”).

An uncharitable reading of what happened here is that Pak put the word out to this 250K Twitter followers and asked them to buy a piece of his NFT, to which they complied. And just to be clear, The Merge is not a masterpiece of ingenuity and aesthetics. It is a grey scale dynamic image of whitish balls and blackish backgrounds that merge and pull apart:

6 Value and Ownership of NFTs

In this section, I want to answer two key questions that have been touched on throughout this article: What makes NFTs valuable? And what does it mean to own them? Let’s start with the question of value. Leaving aside partial availability as a form of scarcity to confer value on NFTs (this omission seems advised because anything digital that’s partially available can be made fully available with a single upload or download, and thus constitutes an open temptation to hackers), the question then becomes this: What turns a publicly available digital file, one that is complete, into something of value?

I’ve said before that the crucial element in this alchemy that turns a digital file with no clear value into an NFT that can be monetized and transacted is a signature. To understand how digital signing produces value in NFTs, it helps to consider what physical signing does to produce value in physical things. In practice, physical signatures create value for physical things in two ways (these need not be mutually exclusive):

- AUTOGRAPH VALUE-ADD. The signature is an autograph by a notable person whose notability is captured by the signature and thereby adds value to the thing. (Think of sports memorabilia signed by hall-of-fame athletes.)

- AUTHORIZATION VALUE-ADD. The signature is an authorization by a person of standing that confers rights and privileges over the thing. (Think of documents signed to buy or sell physical property.)

Digital signatures can perform the same function. We’ve seen digital signatures operate as an autograph for Jack Dorsey’s genesis tweet and Beeple’s Everydays. Even if for Dorsey’s tweet the signature was technically by the Valuables platform and for Beeple’s Everydays by Christie’s auction house, because these services were acting as official representatives for Dorsey and Beeple respectively, the autograph value-add of the signatures on these digital items nonetheless took effect.

With autographs, it’s the notability of the person that adds the value, and the signature need have no intrinsic connection to the thing that’s signed. Anything that’s signed by the notable person becomes more valuable simply in virtue of the signature, and this applies as much to physical as digital signatures. Of course, if the notable person signs too many things (with digital signatures it’s possible to go crazy with signing by automating the signing process), the value of the autographs will go down.

The other task of signatures is to authorize rights and privileges over the thing signed. The ultimate right and privilege to authorize with a signature is ownership, thereby ceding all one’s rights and privileges over it and giving them to another. Unlike the autograph value-add, which requires only a signer, the authorization value-add requires both a signer and an assignee. The signer signs the item over to the assignee. The authorization value-add therefore implies a transfer that takes place on account of the signature. The autograph value-add, by contrast, requires no transfer. Of course, these two value-adds can be combined, so that the autograph and authorization value-adds operate in concert.

Unfortunately, when it comes to the authorization value-add for digital files, confusion is widespread over what is actually being authorized by a digital signature. It’s widely reported that what is being authorized is a transfer of ownership. But as we’ve seen, in the case of NFTs on the Ethereum blockchain, actual ownership with legal standing is never in fact transferred for the underlying digital file. The NFT literature is filled with equivocations about the meaning of the word “own” as it relates to NFTs. Consider the following highlights from a brief article at SuperRare titled “If Anyone Can Download the Art File, Why Would I Buy the NFT?”

The creation of the internet made it nearly impossible for digital artists and creators to 1) prove they created a digital work and 2) monetize these digital creations because everything could be freely downloaded. Ethereum, and the non-fungible token standard (ERC-721) has made huge strides towards solving this problem. For the first time ever, digital creators now have the ability to tokenize their digital artworks as 1 of a kind assets that can be bought, sold and traded, with the provenance of ownership and previous sales/bids being forever recorded on the blockchain…

Yes, anyone can download and view the image for free, but they don’t own it and they can’t gain any value from it without owning the NFT as well. As a collector you want as many people as possible to be downloading and enjoying the artworks that only you provably own because this is how the artwork gains value. Imagine if one million people around the world were featuring an artwork that only you owned on digital frames in their houses. THAT is a piece of art that has real value.

Hackatao, one of SuperRare’s most successful artist duos said it best — “Everybody sees it, only one owns it”.

This is the state-of-the-art argument for legitimating NFTs, and it is absurd. First off, proving that one is the creator of work that exists only digitally is straightforward. Photographers do this all the time, and photo banks such as Getty Images would be out of business except for this fact. Usually, Getty Images applies watermarks to images, which get removed when people download the images for use (the watermarks providing a form of digital scarcity). It’s possible to track unauthorized uses of these images on the web, and some disreputable characters even make a business of putting images out there and then suing people who use them online, often inadvertently, without permission (it’s actually quite a racket).

Proving creation of digital work these days usually requires having a clear web identity, such as with a blog, and then posting the digital work on it. This is what Beeple did for years, and no one questioned that he was the creator of the digital art that appeared on his website (see Beeple-Collect.com). Provenance is also straightforward and simply amounts to identifying a point of origin (usually the first place that a digital work appeared) and then tracking its history across the web.

But perhaps the point of the previous quote is not that digital artists cannot prove that they created a digital work but that they cannot simultaneously prove that they created it and also monetize it. But again, watermarking and digital data embedding technologies, to say nothing of copyright laws and a digital artist’s willingness to enforce them to protect one’s own work, make it possible to prove that one is the creator and to monetize one’s creation. It’s done all the time. Photo banks such as Getty Images are money-making enterprises.

If there is a valid point in the previous quote, it is that NFTs promise to take digital art and allow its creators to turn it into a negotiable instrument, which is to say that the NFT becomes something like an IOU that can be serially signed over to other people as a thing of value and paid for in currency. The Ethereum blockchain is supposed to provide a vehicle for turning NFTs into negotiable instruments, at once recording the digital art and, through the underlying ether cryptocurrency, allowing NFTs to be paid for as they are traded.