Offshore accounts: they’re not just a tax reduction strategy for the rich. They can be useful for anyone concerned about their financial future. Rich or not so rich, then, let’s explore some of the possibilities and complications of moving money offshore.

[NOTE: This article is a chapter in our

Comprehensive Guide to Tax Havens.]

The complexity of the tax system in developed countries, the United States in particular, has led many high net worth individuals, their families, and the companies owned by them, to make use of offshore financial centers and instruments to reduce the income they must report for tax purposes, especially their capital gains tax liabilities. While offshore bank accounts must be declared in the home country of the person who holds the account, some foreign countries do not levy capital gains taxes, so the possibility of growing the account without overly burdensome tax consequences can be attractive. Furthermore, if there is political instability or a high probability of inflation or devaluation of the currency in a person’s home country, holding investments in foreign currencies in an offshore account can serve as a hedge and be a very reasonable thing to do.

This strategy is available to anyone with even very modest resources. Some foreign banks will let a foreign customer open an account with as little as $300. Others, of course, will not do business with foreign customers at all because of compliance requirements imposed by the Organization for Economic Cooperation and Development (OECD) and the World Trade Organization (WTO), and by the U.S. through the Foreign Account Tax Complince Act (FATCA) legislation. While FATCA is mostly aimed at the financial fatcats, it does have ramifications for every American doing business abroad and every foreign business handling American finances, so let’s start by exploring some of the legal and tax ramifications of offshore accounts before moving into a more upbeat consideration of their benefits.

Table of Contents

Contents

The Legalities of Offshore Banking

Having an offshore bank account is perfectly legal and can make sense from the standpoint of running a business, minimizing capital gains taxes, and diversifying currencies and assets because of political or economic instability in a person’s home country. With the prospect of inflation and higher taxes looming in the United States because of out-of-control government spending and general fiscal insanity, American citizens and foreign nationals may wish to include the benefits of foreign bank accounts and foreign investments as part of their financial planning.

The important thing to note, if you are an American citizen or foreign national, is that holding money abroad does not exempt you from U.S. taxes. If you hold over $10,000 in the aggregate in foreign bank accounts, you are required to declare it on an FBAR form (Foreign Bank Account Report) when you file your income taxes. While there is a foreign-earned income tax exclusion for foreign income up to $100,000 for those whose tax home is in a foreign country and who have been out of the U.S. for at least 330 days in a period of 12 consecutive months, the rest is taxable. Keep in mind too that multiple Tax Information Exchange Agreements (TIEAs) that the American government has coerced with other nations require banks around the world to report to the IRS on the account balances and financial activities of American citizens and foreign nationals or face fines and financial withholdings.

Of course, it’s not just the IRS that wants to get into as many pockets as possible. There are a lot of countries around the world equally eager to impose tax burdens on residents and non-residents alike, so much so that the OECD has established Common Reporting Standards for the exchange of financial information among well over 100 countries, and it is working to add new countries to this list every year.

- The OECD Common Reporting Standard (CRS)

- OECD Portal for the Automatic Exchange of Financial Information for Taxes

- OECD List of Countries Committed to the Automatic Exchange of Information for Taxes

Foreign Financial Accounts: The Tax Implications

Offshore banking is legal. Even so, the IRS does not like it and they do their best to discourage it. They want their pound of flesh and they are afraid that U.S. persons with foreign accounts may have made their money inaccessible. This fear has made the IRS hyper-aggressive: failure to file an FBAR form declaring foreign assets cumulatively exceeding $10,000 is subject to a $10,000 fine for each non-willful violation and penalties over $100,000 or confiscation of half the value of the foreign account for willful violations. Willful violations can also incur criminal penalties and prison sentences of up to 10 years. In short, the IRS is intent on scaring you into compliance: give us the money we demand or, if we catch you, we’ll take even more of your money and lock you up. While it is hard not to regard these threats and the need to comply with them as a kind of blackmail, extortion, and plunder, such is the price of American citizenship, or permanent residency for foreign nationals.

With this in mind, let’s take a closer look at the tax implications of being an American expat and of the FBAR form itself, also known as the FinCEN (Financial Crimes Enforcement Network) Form 114, and also of the FATCA legislation.

The primary concern for American expats is the possibility of double taxation. As mentioned, unlike almost any other country in the world, the U.S. taxes its citizens and foreign nationals no matter where they live. Even if they live abroad and conduct all their business on foreign soil with foreign capital and foreign trading partners, the U.S. taxes them as if they were living on U.S. soil and making use of American infrastructure to conduct their business. This means that an expat living in a country that has an income tax will have to pay taxes both to that country and to the United States. If an American deposits his foreign pay check into his foreign bank account, the IRS can grant itself access to that account to collect American taxes. There is provision for partial credit for foreign taxes paid on foreign income, but this is often insufficient to cover all the money the IRS wants. This is why it is imperative that American expats living abroad, if they have a choice, should choose a country that does not itself have income taxes.

Since the IRS wants your money, they make it pretty easy for you to tell them how much you have. Any American citizen or foreign national with foreign bank accounts totaling in value more than $10,000 at any point during the calendar year is required to report these accounts. There is an exception in certain situations for individuals who merely have signature authority over, but no financial interest in, a foreign financial account if that person is an officer or employee of the entity maintaining that account.

It is important to note that FBAR forms require reporting not just foreign bank accounts, but more explicitly all brokerage, securities, savings, demand, checking, deposit, time deposit, retirement, and other accounts maintained with any foreign financial institution, as well as commodity futures and options accounts, any insurance policies with cash vlaue, any annuity policies with cash value, and any shares in mutual funds or other pooled funds. The intended message is that there is no escape and resistance is futile.

To expedite compliance, the IRS modified the Offshore Voluntary Disclosure Program (OVDP) in 2014 to offer assistance to taxpayers that have undisclosed foreign financial assets. These concessions included the elimination of penalties for non-willful violations as long as all the required additional information is provided. Between 2014 and 2016, the OVDP provisions have brought another 45,000 taxpayers into the IRS fold and generated an extra $6.5 billion in taxes and penalties.

Apart from the OVDP, other penalty relief measures have also been instituted. Taxpayers who failed to file required FBARs and are not under IRS civil examination or criminal investigation can e-file the delinquent FBAR forms along with a statement explaining why the filing is late. Penalties will not be assessed in such case as long as the reports are complete and the requisite taxes are paid, provided the IRS has not previously contacted the taxpayer to audit their accounts or to request delinquent tax returns for the tax years that the delinquent FBARs were filed.

The 2010 Foreign Account Tax Compliance Act (FATCA), which was phased in and didn’t take effect until 2014, was a brainchild of the Democratic party many years in the making and, with the addition of multiple coerced Tax Information Exchange Agreements (TIEAs), is designed to force tax compliance on Americans abroad, on American foreign investors, and on foreign banks. It requires non-U.S. banks to report accounts held by American citizens or foreign nationals that contain more than $50,000, or be subject to 30% withholding penalties and possible exclusion from American markets.

By the middle of 2015, the IRS had secured the compliance of more than 100,000 foreign financial entities who agreed to share their financial information. Even Russia and China agreed to FATCA. The only major economy to fight the United States on this matter was Canada, though it was private citizens, not the Canadian government, which did so. They filed suit to block FATCA and make it illegal for the Canadian government to sign an international governmental agreement to turn over private bank account information to a foreign country. Unfortunately, this lawsuit was rejected in 2019 and Canadian financial firms must now comply with FATCA, providing complete financial data on their American clients.

What FATCA gives the IRS, then, is the names, addresses, identification numbers, account numbers, and balances of all American holders of foreign financial accounts. To comply with FATCA legislation, in addition to the FBAR form, American taxpayers must also submit the largely redundant IRS Form 8938.

It is estimated that there are at least 6 million American expats living abroad. There are many more domestic citizens who hold foreign accounts. Despite these figures, each year, less than one million citizens file FBARs declaring their foreign assets. This discrepancy means that a millions of American taxpayers are not in compliance with IRS regulations. One sympathizes with these taxpayers, but they’re playing with fire.

How to Open and Access Offshore Bank Accounts

An offshore financial account is any account that is held by an American taxpayer outside the United States. By this standard, both Canada and Mexico are “offshore.” Some places are well-known for offshore accounts–Bermuda, the Cayman Islands, Switzerland, and so on–but other less-known locales, such as Mauritius and Belize, also conduct a brisk business in offshore financial accounts.

While the IRS casts a long shadow over foreign accounts, making them appear shady in their own right, the fact remains that there are many legitimate reasons for having an offshore account that don’t involve tax evasion. For instance, having an offshore account may be necessary or useful if you run a business in a foreign country, have foreign investments or property, spend considerable time in a foreign nation each year, or want the legal benefits that accompany financial dealings in nations with less egregious tax laws.

To open an offshore account, you will have to provide proof of identity. An offshore bank will need you to provide verification of personal information, including obvious things like your name, address, country of citizenship, and occupation. To supply the requisite documentation, you will need a copy of your passport, driver’s license, or some other official government document confirming your identity.

It is worth noting at this point that if you are an American who has secured a second tax residency in another country and has possession of a second passport through a citizenship-by-investment program or something similar, or if you are a foreign national with an address in your home country, you should be able to establish an offshore account with identification documents and addresses from your second country of residence. This simple solution makes the account you are opening immune to FATCA or TIEA compliance on the part of any agreement the tax haven has established with the IRS. If you’re thinking of doing something like this, however, we strongly recommend you get reliable professional advice on its legal ramifications and make sure you are within the boundaries of reasonable interpretations of the relevant laws.

Because of taxation issues, foreign banks also will commonly want to verify your address through the provision of a utility bill or something similar with your name and address on it. To ensure the authenticity of the copies of the documents you provide, you will probably be required either to have them notarized, or more likely, stamped with an apostille seal for international certifications.

To prevent the international money laundering and fraud that are sometimes associated with offshore banking, various other verification processes may also be required. In particular, an offshore bank may ask for verification documents, usually the last few months of statements, from your current bank to provide them with assurance that you have acceptable minimum balances and an ongoing relationship in good status with a financial institution.

Foreign financial institutions where you are opening an account may have additional questions about the kinds of transactions you expect to conduct through their services and verification of the source of the funds to be deposited with them. For instance, wage statements from your employer in your home country may be required, or the provenance of your investment income may need to be documented, or you may need to provide sales contracts as verification of business or real estate transactions, or a letter from your insurance company if the funds originate with an insurance settlement. If the money being deposited comes from an inheritance, you likely will be asked for legal documentation from the executor of the estate in question. All of this is quite intrusive, but has come about through government pressure on banks with foreign customers in order to prevent illegal international activities.

When you open a foreign bank account, you will be offered options for the currency in which you wish to hold your funds. Choose a stable international currency not expected to fluctuate wildly or depreciate on the world market. Americans might especially want to keep this in mind and take advantage of a stable foreign currency as a store of value. The wanton printing of trillions by the U.S. government, which has flooded the world with U.S. dollars, the prospect of rampant inflation at home, and a growing trade deficit, have created a situation in which a foreign currency and foreign investment hedge is a wise course of action. Just be sure to choose the currency of a country that is politically and economically stable and has not been pursuing monetary policies similar to the U.S. as of late. Swiss Francs are a good bet.

- What Would It Take for the U.S. Dollar to Collapse?

- Goldman Sachs Warns the Dollar is in Peril

- If You Think the Dollar Has Lost Value Now, Just Wait

- The Dollar’s Crash is Only Just Beginning

The only drawbacks in holding a foreign account in a foreign currency are the possibility of acquiring foreign tax liabilities from interest on your deposits and the inevitability of paying currency exchange rates on deposits and withdrawals. Depending on the amounts involved and the fee structures and exchange rates offered by the foreign bank, these kinds of expenses could become a significant liability.

In the last few years another possibility has arisen: having access to funds internationally through cryptocurrencies that aren’t created by any national government and aren’t, as of yet, subject to standard government controls, and storing your cryptocurrency in a private electronic wallet rather than depositing money (or even the cryptocurrency itself) with a bank. There are, of course, some risks associated with trying to take your finances off the grid in this way. But this is a subject for another time. For now, we need to finish our overview of the mechanics of offshore banking.

Once established, offshore bank accounts are usually funded through wire transfers. Unfortunately, when this is done internationally, virtually all banks charge transfer fees for both sending and receiving funds. If you will need to transfer money frequently, you should look for banks (on both ends) that have reasonable fees for this service.

Alternatively, you may wish to use an independent wire transfer service that performs this service in a secure and more cost effective manner. One service I would recommend for international transfers is the Australian company OFX. It offers competitive rates for delivery of funds to more than 190 countries, and it does not charge transfer fees.

When it comes to withdrawing money from an offshore account, offshore banks generally try to make it convenient by issuing debit cards that, for a fee on a per use basis, give you access to your funds worldwide. Since charges add up for frequent use, withdrawing larger amounts less frequently is a possible strategy. Some offshore banks will also provide checks, but this compromises the anonymity of an offshore account and runs into the problem that foreign checks are frequently not accepted as a means of payment. The best solution may be electronic transfers between offshore accounts and domestic accounts, with the use of a domestic debit card.

Setting up an offshore account is not a difficult thing to do if you’re willing to be patient with the paperwork, identification document requirements, and funding source verification processes. The best choice of currency to hold and the most efficient and cost-effective means for transactions will be made clear as you consider the alternatives available to you. And of course, you will want to consult with a tax professional regarding the relevant tax regulations both offshore and at home regarding international wire transfers.

Offshore Brokerage Accounts

An offshore brokerage account, which is an account at a foreign brokerage established for the purpose of handling your investments and trading securities, has the same sort of conditions governing it as offshore banking. If you have an established second tax residency and passport in a tax haven, you can open a brokerage account with this documentation. Alternatively, you may wish to establish a shell company as a foreign business located in the tax haven and have the company open the account, perhaps even utilizing nominee directors for this purpose. We will discuss this strategy next. Whatever you decide to do, make sure you get professional advice and dot all your legal i‘s and cross all your legal t’s.

Should You Create an Offshore Shell Corporation?

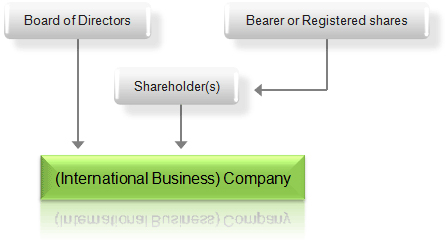

The primary purpose of a shell company is to manage funds on behalf of another entity, often another company, but sometimes an individual. A shell company has financial assets but no significant business activity. It doesn’t create products, have employees, or generate revenue; it simply stores money and engages in financial transactions on behalf of another entity. Shell companies are used as legal and corporate tools for the purpose of providing confidentiality, storing and moving funds, and reducing taxes. All of this can be done legally and, for the most part, is done legally. But shell companies can also be used for illegal purposes such as money laundering or tax evasion, which is why shell companies have a dubious reputation in certain quarters.

A shell company can be set up anonymously and work effectively to conceal the identities of its owners so that financial transactions can be conducted without the participants revealing who they are. This is lawful and can be useful for a variety of reasons: (1) the shell company can be used as a holding company for funds when an established company or an individual is preparing to start a new company; (2) it can be the vehicle for a “hostile takeover” when a company takes over a competitor without the approval of the target company’s management; (3) when established offshore, it can be a useful way to invest in foreign markets; (4) it can be a means of protecting assets from lawsuits; (5) it can hide the money of wealthy individuals for the purpose of safety to protect them from being targeted by criminals; and (6) handled carefully, it can be used as a legal strategy for tax reduction.

Shell companies are often created in tax havens where few or no taxes are imposed upon businesses and banking information is well-protected, though not as well-protected as it once due to the efforts of the IRS, FATCA legislation, TIEAs, and entities like the G-20 and the OECD. Even so, a tax-haven-based shell company can open bank accounts and move funds, have access to foreign markets, engage in financial transactions, manage an investment portfolio, buy real estate, and own copyrights and collect royalties, all while benefitting from the lower taxes it owes as a foreign company in a tax haven.

Every shell corporation must register as a company in the country in which it is created. In the U.S., shell companies register with the Securities and Exchange Commission (SEC). Registered agent services in the tax haven locale will set up the shell company by filing the paperwork and sending the fees to the requisite company register on behalf of the business. Shell companies do not have to be set up in person, they can be created online or over the phone, with incorporation fees ranging from a few hundred to a few thousand dollars.

Setting up a shell company this way generally requires very little personal information—just the identities of the registered agent and the owner—and the latter can be rendered even more secret if the company hires nominee directors, perhaps native to the tax haven itself, to file the paperwork under their own names. An additional layer of security can be added when the shell company being created registers as a subsidiary of another shell company. When the subsidiary shell company is in a different tax haven than the shell company that owns it, the real owner of the subsidiary has an extra layer of anonymity and protection. In particular, the subsidiary is in a gray area and might avoid FATCA legislation and TIEAs because its ownership is foreign-based. If the recorded assets of the shell company owning the subsidiary are kept under $50,000, it too may avoid FATCA/TIEA reporting requirements, something that could be ensured through the utilization of a nominee directorship.

If an individual forming a shell company is financially able to do so, it may also be useful to establish tax residency in the chosen tax haven through a citizenship-by-investment program, though it is worthwhile to keep in mind that the OECD has recently been working to clamp down on citizenship-by-investment programs being used to avoid the reporting of income and assets in the tax refugees’ home country.

- OECD/G-20 Clamp Down on Common Reporting Standard Avoidance through Citizenship-by-Investment

- OECD: Preventing Abuse of Residence-by-Investment Schemes to Circumvent the CRS

Needless to say, we are not committing to any recommendations here. Such matters are complicated and the legality of the corporate structures and their proper implementation for tax purposes need the guidance of well-qualified tax lawyers and accountants at home and abroad. Please exercise due diligence before making any decisions.

Shell companies can be created pretty much anywhere, but certain locations are more popular than others. Switzerland has been a standard location for such entities, with estimates that as much as sixty-percent of the money in Swiss bank accounts belongs to shell companies. Other popular locations for shell companies are the Bahamas, Bermuda, the British Virgin Islands, the Cayman Islands, Jersey (Island), and Luxembourg. Within the United States, Delaware, Nevada, and Wyoming are the most popular states in which to create shell companies because they have easy-going incorporation requirements and strict privacy laws. In fact, using shell companies based in such states, foreigners gain easy access to the U.S. real estate market. Much of the real estate in major American cities is owned by such shell corporations.

Summary: The Pros and Cons of Offshore Investments

Let’s consider the benefits of investing offshore. Offshore investments, even securing a second tax residency or citizenship in a tax haven, holds the prospect of many advantages. There is no shortage of offshore strategies that are legal and that offer a broader range of investments, tax benefits, privacy, and asset protection.

One of the most common ways an offshore investor makes arrangements to handle their offshore financial activities is to create a shell company in a tax haven for their accounts and assets that shields them from the higher tax burden in their home country. As a foreign-based company, a tax-advantaged status is enjoyed when investments are made in U.S. markets, so channeling investments through a foreign corporation can have distinct advantages. Furthermore, through trusts, foundations, or shell companies, individual wealth can be transferred to protect family wealth from lawsuits, criminal interests, and egregious taxes.

In establishing an offshore trust, for instance, if the trustor remains a U.S. resident, his trustor status enables him to make contributions to the trust to reduce his taxable income. Of course, the trustor of an offshore asset-protection fund will still be taxed on the trust’s income, even if it is not distributed. But the tax paid because of the growth of an offshore trust fund is offset by the reduction in taxes achieved by transferring domestic income to the trust.

Confidentiality is intended to be the watchword of tax havens. Most of them have instituted laws establishing strict banking and corporate confidentiality regarding the identities of investors. Autonomous nations are not required to respect the laws of other nations—though they can be coerced to do so—and are thus not bound by the laws of their investors’ home countries. For instance, some countries stringently regulate international investment opportunities that limit access to international markets, whereas offshore investment accounts have unlimited access to the world’s markets and exchanges where securities are traded. Unless coerced to do so, tax havens are under no obligation to provide tax information to the home countries of their investors. As noted, though, this has been changing through the efforts of the OECD and the WTO, and has changed considerably for Americans and American foreign nationals because of FATCA legislation and TIEA reporting requirements between the IRS and foreign tax havens the U.S. government has negotiated using coercive tactics.

This brings us to the cons of offshore investment. One of the primary drawbacks is the increased government scrutiny that holding offshore accounts catalyzes. Regulatory scrutiny is not just the nemesis of every illegal actor—money launderers and drug traffickers, for instance—but also the bain of every legitimate investor. Secondly, there is the cost of setting up offshore accounts and creating any companies needed to take advantage of the benefits of offshore investment and asset protection.

Let’s first consider the various regulatory regimes seeking to erode the ability to preserve private family wealth for future generations and for private philanthropic use. Internationally, the Organization for Economic Cooperation and Development (OECD) and the World Trade Organization (WTO) have worked to impose regulations requiring banks in as many nations as possible to report information on their foreign customers. Each country has responded to these regulations in different ways and in different degrees, some complying broadly and others not at all.

More insidious for American investors, however, has been the U.S. Foreign Account Tax Compliance Act (FATCA) passed in 2010 and enacted in 2014, and various Tax Information Exchange Agreements (TIEAs) enacted in its wake. These not only require U.S. citizens, no matter whether they live at home or abroad, to file annual reports on their foreign financial holdings, but have leveraged agreements with a large number of foreign nations that require them to report on the financial holdings and activities of Americans abroad if they wish to avoid having their own national finances interrupted and withheld by the United States. The result has been a further drain of private wealth into the government coffers as the ability of U.S. taxpayers to reduce taxes by shifting their tax liability to some foreign entity has become increasingly restricted and vastly more complicated.

The final drawback to consider is the cost of establishing offshore accounts. This will vary depending on your goals and the jurisdictions you have in mind. Foreign accounts will have minimum deposits and balance requirements as well as transaction fees, and setting up shell companies will involve service and registration fees as well as ongoing licensing fees. Finally, due diligence in assuring the legality of your arrangements and their proper setup will incur the fees of investment advisors, accountants, and attorneys both at home and abroad, and this may also involve travel expenses. Individual investors will need to count the costs and decide whether they are suitably offset by the gains.

[NOTE: This article is a chapter in our

Comprehensive Guide to Tax Havens.]