The Wealth Tax in Plain English

What would it mean for the government to impose a wealth tax? In the broadest sense, a wealth tax is imposed on everything that you own. Such taxes are often reserved for those the government deems to be “wealthy.” This can be an individual or a corporation, since the latter is treated as a person under the law because it can own property, buy things, invest, and do most of the things an ordinary person can do.

The “wealth” in question consists of everything owned—all the money, all the property, everything inherited, and so on—minus everything owed; in short, everything the individual or corporation is worth. Nothing owned is out of bounds and there’s nowhere it’s legal to hide it. The government’s approach when imposing a wealth tax is illustrated by Shakespeare’s Henry V, Act 2, Scene 4, where the Duke of Exeter presents the English King’s demands to the King of France regarding the crown:

…[I]f you hide the crown

Even in your hearts, there will he rake for it.

Therefore in fierce tempest is he coming,

In thunder and in earthquake like a Jove,

That, if requiring fail, he will compel,

And bids you, in the bowels of the Lord,

Deliver up the crown…

In essence, the government says to those deemed wealthy: we’re coming for a portion of everything you own, and if you try to hide it, no matter where you put it, we’ll find it and take it from you. And of course, people will try to hide their hard-earned wealth and their family wealth, believing it belongs to them to be handled—charitably or otherwise—as they see fit, not taken from them and distributed or squandered as the government sees fit. Witness, in this regard, the French finance minister in 2013, Jérôme Cahuzac, who shifted his financial assets into Swiss bank accounts in order to minimize his tax liability under his own government’s wealth tax. As it turned out, Cahuzac was merely one of more than sixty French parliamentarians ultimately investigated for suspiciously low asset declarations. Ultimately, France abandoned the wealth tax.

Given the moral claim to one’s private property and obvious incentives for its preservation, even among politicians themselves, why would anyone think the wealth tax is a good idea? It’s primarily advocated by those who bemoan an increasing disparity of wealth and express themselves using the old chestnut that “the rich get richer while the poor get poorer.” Setting aside the cynical observation that advocating a wealth tax is a form of virtue-signaling which polls well among the voter base for such politicians, we need to take seriously the sentiment that it is wrong for the rich live in luxury while the poor struggle to survive, and the perception that the wealth tax is a good means for remedying this imbalance. If we could somehow transfer excess wealth from the rich to the poor, wealth tax advocates say, the world would be a better place. In the estimation of the more zealous wealth-tax advocates, this transfer of wealth should take place both within nations and among nations, as wealthy nations share their good fortune with poorer ones.

Let’s take a closer look at these ideas. A glossary is included at the end of the essay for your convenience and the first occurrence in the essay of a term that appears in the glossary is indicated in bold italics.

Why Would Anyone Think the Wealth Tax is a Good Idea?

A wealth tax is most often levied as an annual tax on the net worth of an individual or corporation above a certain exemption threshold. It is usually in addition to any income tax, sales tax, or other existing form of taxation. Wealth taxes also frequently include a punitive exit tax on assets to discourage capital flight by those seeking to avoid it by renouncing their citizenship and moving abroad. Beyond this, wealth taxes are usually levied on worldwide assets, so if citizenship is retained, there is no tax haven where wealth may legally be sequestered.

As a simple example, consider a 3% wealth tax imposed on net worth over $10 million (the exemption threshold) in worldwide assets. A very wealthy individual with a net worth of $10 billion would be required to pay 3% on the $9.99 billion in assets they own above the $10 million, which would mean paying a $299.7 million wealth tax every year their net worth remained at this level. If an additional 1% marginal tax were imposed on net worth above $100 million, the individual would owe $398.7 million in total wealth taxes. If we take someone who is hyper-wealthy, like Jeff Bezos of Amazon, whose net worth is around $200 billion, he would end up with a wealth tax of $7.9987 billion each year. This would be in addition to income tax and every other kind of tax, for which Bezos would also be responsible.

If we take someone who is hyper-wealthy, like Jeff Bezos of Amazon, whose net worth is around $200 billion, he would end up with a wealth tax of $7.9987 billion each year.

American proponents of a wealth tax—politicians like Bernie Sanders and Elizabeth Warren—argue it would ameliorate rising wealth inequality while generating substantial tax revenue for redistribution through government entitlement programs and projects. Sanders’ progressive tax on net worth ranges from 1% on wealth over $32 million to 8% on wealth over $10 billion. Warren’s progressive plan taxes wealth over $50 million at 2% and wealth over $1 billion at 6%. By these standards, Bezos is catching a break in the example above. Sanders’ plan would affect about 180,000 families in the United States and he estimates it would raise about $4 trillion over a 10-year period; Warren’s would affect 75,000 families and she estimates it would raise $3.7 trillion in 10 years. Economists disagree on this assessment. Lawrence Summers and Natasha Sarin, for instance, argue that the Warren plan would only raise 12% to 40% of this figure, an analysis disputed by Warren apologists Emmanuel Saez and Gabriel Zucman.

Even so, those who advocate a wealth tax champion it as an effective means of addressing economic disparity. Wealthy people accumulate vast fortunes without vast tax consequences, they maintain, when those fortunes could be put to work serving the public good by financing government health care, public education through college, a vastly expanded welfare state, and so on. By contrast, middle income people have savings accounts and, if they’re fortunate, investment accounts, and they pay income taxes on the interest and any capital gains realized each year, thus limiting the growth of their wealth. Tax-free growth for the middle class comes mostly in the form of IRAs that have contribution limits and, if they aren’t Roth IRAs built from income already taxed, tax will be paid on the withdrawals when they’re eventually required to make them.

The median income for white households is $68,000 per year but only $50,000 per year for Latin American households and $40,000 for African American households.

Meanwhile, the rich have vast assets that appreciate each year and on which they have unrealized capital gains. No tax is owed on these gains unless the assets are sold, thus allowing their wealth to accumulate much more rapidly and substantially over time. Ordinary working Americans, on the other hand, pay taxes on their incomes annually. This explains why wealth inequality vastly exceeds income inequality. While the top 1% of income earners in America receive about 20% of the total income each year, the top 1% of wealth holders own 42% of the wealth, according to Saez and Zucman. Furthermore, there is a racial income gap. The median income for white households is $68,000 per year but only $50,000 per year for Latin American households and $40,000 for African American households.

Wealth disparity is even more pronounced in that median wealth for white households is $140,500, but only $6,300 for Latin American and $3,400 for African American households. Wealth tax advocates argue that this is the result of generations of compounded inequality that must be addressed. In their eyes, the wealth tax can ameliorate these economic disparities by directly taxing these assets and transferring this wealth where it’s most needed to alleviate disparity. You could think of it in terms of Karl Marx’s slogan, “from each according to his ability; to each according to his need.” And the rich are able.

For example, one tax expert estimated that in 2015, when Warren Buffett’s net worth was about $70 billion, if Buffett’s unrealized capital gains had been subject to a standard wealth tax each year from the start of his career, his net worth would only have been $9.5 billion, regardless of whether his assets were sold. In the eyes of wealth tax advocates, that’s over $60 billion that the government could have appropriated during this time to serve its vision of the public good. Of course, nowhere near $60 billion would have been generated if the government had helped itself to some of Buffett’s unrealized capital gains each year.

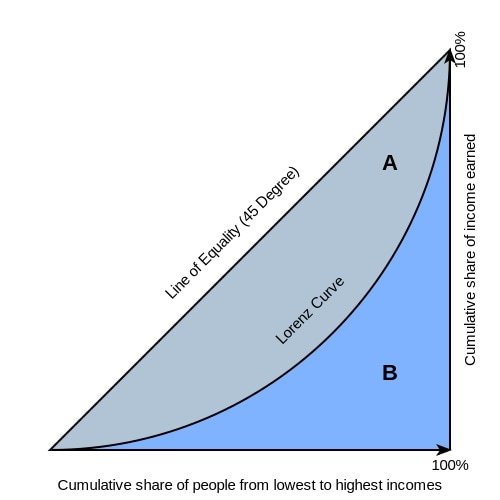

A statistical tool for wealth tax analysis is the Lorenz Curve and its associated Gini Coefficient (also known as the Gini Index). The Lorenz Curve gives a graphical representation of either the income or the wealth distribution in a population, and the Gini Coefficient quantifies the difference between this curve and perfect equality as a number between 0 and 1, with 0 being perfect equality and 1 being perfect inequality. While the Gini Coefficient for income distribution in the United States is large, evaluated at 0.4046 in 2010, it is nonetheless about the same as for African countries. Of course, the income scales are different because the United States has one of the highest levels of income per capita in the world. On the other hand, when wealth distribution is measured, the United States’ Gini Coefficient is one of the highest in the world, measuring 0.852 in 2018. The analysis is even more pronounced if the Gini Coefficients are applied worldwide, giving Gini Coefficients for both income and wealth inequality approaching 1, with first world nations at the top of the wealth and income scales, and developing nations at the bottom.

In light of this worldwide economic disparity, various globalists propose a worldwide wealth tax. Economist Jeffrey Sachs has advocated a 1% worldwide tax on all wealth, including individual assets in excess of $1 million, all publicly listed companies, and all trusts, transferring wealth from industrialized countries to developing countries with the goal of helping them across the threshold of economic competitiveness in 15-20 years. In 2014, economist Thomas Piketty proposed a global system of progressive wealth taxes to reduce worldwide inequality and prevent the world’s wealth coming under the control of a minority of nations and individuals. Both proposals have been subjected to severe criticisms and are politically impractical and logistically intractable.

Anatomy of a Really Bad Idea: A Critique of the Wealth Tax

A variety of arguments demonstrate that, when all is considered, the imposition of a wealth tax is a bad idea.

Let’s consider the effects of implementing a wealth tax in America before briefly discussing the concept of a global wealth tax. The intention of wealth tax advocates like Warren and Sanders is that the burden of a vast expansion of government regulation and welfare be imposed on a comparatively small number of wealthy individuals. This is naïve. The disincentives created by a wealth tax would cause the burden of the tax to metastasize throughout the whole economy. As argued by economists Douglas Holtz-Eakin, former Director of the Congressional Budget Office, and Gordon Gray, Director of Fiscal Policy at the American Action Forum, the reduction in the supply of capital induced by wealth taxes would reduce investment in innovation, thus resulting in lower productivity and, ultimately, a reduction in the growth of wages, thereby partly shifting the effective burden of the wealth tax to the average worker.

In a market economy, it is simply wrong to think that workers can be insulated from the effects a wealth tax would have on the ability of the owners of capital and industry to reinvest in work facilities, the work force, research and development, capital equipment, and intellectual property. The only debate remaining is how large the financial burden affecting the wages and jobs of average workers would be.

Over the long run, Holtz-Eakin and Gray argue that a wealth tax of the sort proposed by Warren and Sanders would collectively impose an effective tax of 63 cents on average workers for every dollar of revenue raised. In addition, Holtz-Eakin and Gray calculate that this wealth tax would shrink the Gross Domestic Product (GDP) by $1.1 trillion during the first ten years, with a further reduction of $283 billion each successive year (all measured in 2018 dollars). Given a GDP of $21 trillion (in 2018), the erosive effects of the wealth tax on the American economy would advance at an alarming rate.

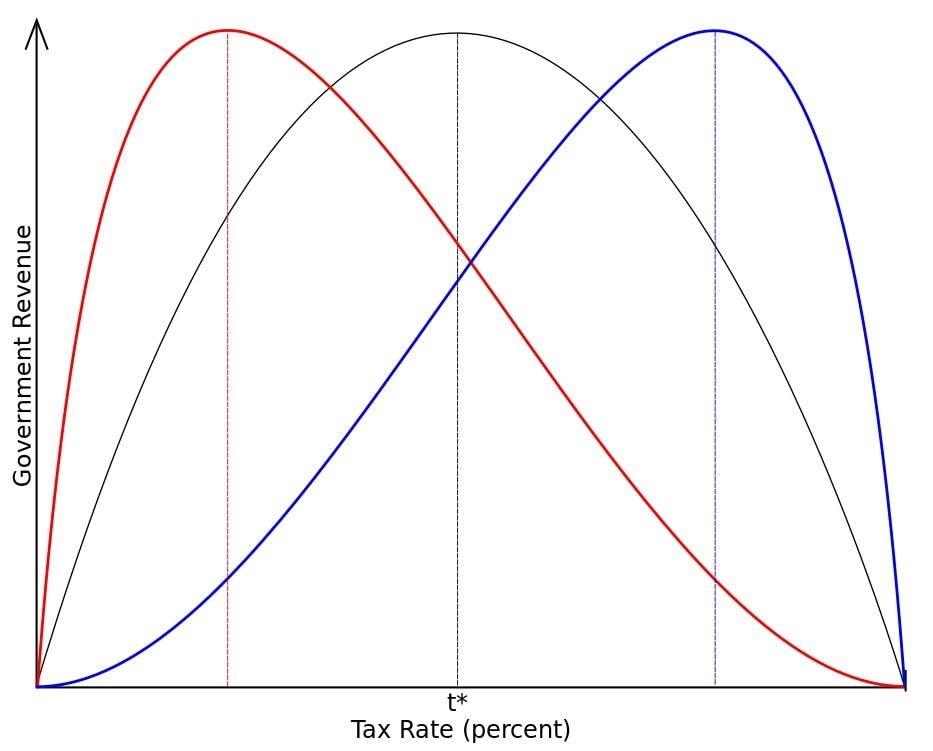

What advocates of a wealth tax fail to appreciate is that increasing the tax burden reduces the amount of capital available for economic expansion, thereby reducing the amount of income generated to be taxed, which ultimately leads to a reduction in tax revenue. This consequence is nicely illustrated by the Laffer Curve, which shows the relationship between tax rates and the amount of tax revenue collected by the government. Lowering tax rates allows the economy to expand faster than it otherwise would and can result in a net increase in tax revenue.

Another fatal flaw of the wealth tax is the issue of valuation. In 2012, the Wall Street Journal estimated that 62% of the wealth of the top 1% was non-financial,

Another fatal flaw of the wealth tax is the issue of valuation. In 2012, the Wall Street Journal estimated that 62% of the wealth of the top 1% was non-financial, consisting of real estate, vehicles, and ownership of private businesses, with the last constituting the largest category and accounting for nearly 40% of the wealth in question. The difficulty, of course, is that the value of a business is difficult to assess until it is sold and business owners are well-practiced, for tax purposes, in making their businesses look less valuable than they are.

The question of valuation also leads to the matter of its implementation. Instituting a wealth tax would require a vast expansion of the IRS since it would be responsible for the difficult, invasive, and costly task of tracking and valuing the worldwide assets of wealthy individuals and corporations. Furthermore, the value of these assets fluctuates, so a date would have to be specified each year on which the assets were valued. In January 2019, the Institute on Taxation and Economic Policy, which favors a federal wealth tax, estimated that Warren’s wealth tax, which is simpler than Sanders’, would require at least $5 billion in new spending on the IRS and hiring the equivalent of 80,800 new full-time IRS agents.

A wealth tax also succumbs to the law of unintended consequences. Families owning homes that historically were valued much more modestly than they are now may find, with real estate appreciation, that they are subject to a wealth tax they cannot afford to pay. The same may apply to farmers who earn little but whose land is subject to high valuation. Depending on the level at which wealth taxes are assessed—and ad valorem taxes on property are levied on all home and land owners—families with insufficient liquidity may be forced out of their homes or off their land. A federal wealth tax on all assets would only increase this burden and make such an undesirable outcome more common.

With respect to private businesses, wealth taxes strip them of resources that could be invested in improving products and services and hiring more workers, ultimately leading to downsizing and a reduction in employment. A wealth tax forces a private business to get a valuation every year, even as the tax drives down that valuation. This cyclical effect is easily devastating, ultimately driving the company out of business. Family-owned businesses over a certain size would almost certainly disappear from the economic landscape, either being sold to public companies or private equity firms with a large and diverse base of investors. In short, a wealth tax poses an existential threat to the success of private companies.

In the United States, wealth tax proposals also face a challenge regarding their constitutionality. The debate over the constitutionality of a wealth tax revolves around the question of whether it is a direct tax, since Article 1, Section 9 of the Constitution requires that direct taxes be apportioned across the states by their populations. While the Sixteenth Amendment made an exception for the income tax, it says nothing about wealth or assets or property, so it remains debatable whether a federal wealth tax would be constitutional.

In short, before the government could impose a national wealth tax, another constitutional amendment may be required. Beyond this, it is arguable that the wealth tax and various penalties for its avoidance—for example, an exit tax for someone renouncing their citizenship and leaving the country—runs afoul of the takings clause of the Fifth Amendment, which prohibits government appropriation of private property for public use without just compensation.

If we consider how wealth taxes have fared in other countries, we may note that fifteen different countries had a wealth tax in 1995, but only four still have one. Eleven of these countries judged the wealth tax to be a failure and they eliminated it. Germany even made it unconstitutional in 1995, judging that it would have to be confiscatory to bring about any real redistribution of wealth, and would thus either be undesirable or inefficient.

Given the widespread failure of wealth taxes imposed at the national level, the idea of a global wealth tax is risible. Not only would the requisite valuations be intractable and inequitable, its administration would be impossible, and the very idea that some sort of international body should impose taxes on the citizens of every nation of the world is both megalomaniacal and tyrannical. It would violate national sovereignty and be rejected by the majority of the free world’s citizenry. If history teaches us anything it is that government functions best when it is most sensitive to needs at the local level. The government of a large nation is ineffective and inequitable enough. The idea that the world economy could be managed from the top down is an academic fantasy and the pipe dream of would-be despots.

This brings us, finally, to the moral dimensions of the wealth tax. While its proponents see themselves as occupying the moral high ground, they are merely myopic. As Thomas Sowell wisely observed, “I have never understood why it is ‘greed’ to want to keep the money you have earned, but not greed to want to take somebody else’s money.” The whole idea that wealth needs to be redistributed is based on the false premise that there’s a fixed amount of wealth in the world so that, when there is wealth disparity, some people have too big a piece of the pie.

No. Wealth acquisition is not a zero-sum game. Wealth is created. The fact that Jeff Bezos is hyper-wealthy doesn’t make me poorer. In fact, in free world market economies it is a general principle that when the rich get richer, the “poor” also get richer because more jobs are created and average salaries rise. Wealth at the lower end of the spectrum doesn’t increase at the same rate as the top end, which explains increasing economic disparity, but that disparity is not an indication of abject poverty at the lower end of the scale. While we should not minimize the difficulty of being poor in America—Barbara Ehrenriech’s book Nickel and Dimed: On (Not) Getting By In America gives a vivid account of this—the fact remains that the poor in America do not experience the abject poverty of vast swaths of humanity in the third world. American advocates of the wealth tax need a reality check. If more tax revenue is desired, the secret is to be found in wealth creation, not unjust wealth confiscation.

Conclusion

Ultimately, a wealth tax is a form of double-taxation and an immoral and direct confiscation of personal assets. Not only does it erode the economic health of a nation and diminish the wealth of all its citizens, such a tax contributes to a tragedy of philanthropy by stifling personal generosity and appropriating resources that might otherwise voluntarily be given, all the while alienating givers from receivers by interposing an impersonal bureaucracy.

To sum up, the wealth tax undermines personal freedom, generosity, and liberty. It is essentially Marxist in conception and morally destructive of the values of a free society. By taxing long-owned property, it alters the very institution of private property and the relationship between the citizen and the state, turning freeholders into leaseholders and violating a core principle of American identity, namely, the expansion of private property and the democratization of wealth. It is an utterly toxic idea that must be resisted at every turn.

Glossary: Locking in Some Lingo

It’s good to have familiarity with the vocabulary in which this idea is debated. Here are some terms it’s helpful to know (examples for many of which are found in the preceding discussion):

Ad valorem tax: Ad valorem is a Latin phrase meaning “according to value.” An ad valorem tax is imposed on the basis of the assessed value (the dollar value assigned for tax purposes) of the item being taxed. The most common ad valorem tax is the municipal property tax assessed on the real estate of property owners, but it may also be levied on other property that is owned, such as cars and recreational vehicles.

Assets: An asset is anything of monetary value owned by an individual, corporation, or organization.

Capital Flight: Capital flight is the exodus of financial assets from a country because of political or economic instability, currency devaluation, punitive taxation, or the imposition of capital controls attempting to restrict the flow of money into or out of a country.

Capital Gains: A capital gain is an increase in the value of a capital asset. It is realized and subject to capital gains tax when that asset is sold. If the asset is not sold, the capital gain is unrealized. Capital gains are short-term if they are realized in a year or less, and long-term if realized after holding that asset for at least a year. Realized capital gains are reported for tax purposes and taxed at a higher rate if they are short-term rather than long-term gains.

Direct Tax: A direct tax is a tax paid by an individual or an organization directly to the entity imposing it. Some examples of direct taxes are income taxes, property taxes, corporate taxes, estate taxes, and taxes on assets.

Economic Disparity/Inequality: Economic disparity simply refers to differences in personal income and wealth. Given that some people live in luxury while others live in abject poverty, the question gets asked whether taxation should be used in an attempt to address these differences.

Estate: An estate is the entire net worth of an individual and includes all of the real estate, investments, cash, possessions and other assets owned by an individual. An individual’s entire net worth is of particular relevance under conditions of bankruptcy, death, or the imposition of a wealth tax.

Exit Tax: An exit tax or expatriation tax is a tax filing procedure sometimes required for individuals moving abroad and giving up their citizenship in a country. For instance, it applies to some US citizens or holders of a green card (permanent alien residents) seeking to leave the country and end their tax obligations. The exit tax process measures untaxed income and delivers a final tax bill. Countries often require exit taxes because some income classified as taxable, such as capital gains on home ownership, is not taxed until you dispose of the asset. Once you fully leave the jurisdiction of a country it can no longer pursue you for taxes, which is why it wants to grab its share of your assets while it can.

Fiduciary: A person or organization functioning as a fiduciary acts on behalf of another person, persons, or organization by putting the interests of their client ahead of their own with the legal and moral duty to act transparently and honestly in the best interest of their client.

Flat Tax: A flat tax or proportional tax applies the same tax rate to everyone regardless of income.

Gini Coefficient: Named after the Italian statistician Corrado Gini (1884-1965), the Gini Coefficient, or Gini Index, measures the distribution of income across a population and is often used to assess income or wealth distribution across a population as a gauge of economic inequality. The coefficient ranges from 0 (perfect equality) to 1 (perfect inequality), with values over 1 being theoretically possible because of negative income or wealth. See also Lorenz Curve.

Gross Domestic Product (GDP): The GDP is defined as the total monetary or market value of all goods and services that are produced in a country during a specific time period. It provides a broad measure of domestic production and functions as a comprehensive indicator of the economic health of a country.

Investment: Investment is the use of financial resources in the pursuit of financial gain; in short, money used in a way that may earn you more money.

Laffer Curve: The Laffer Curve, named after American economist Arthur Laffer (1940 – ), shows the relationship between tax rates and the amount of tax revenue collected by governments. The curve (see below) illustrates the principle that reducing the overall tax rate can sometimes lead to an increase in total tax revenue. Taxes that are too high along the curve discourage the associated taxed activities—work and investment—enough to reduce tax revenue, in which case cutting taxes will reinvigorate those activities and increase tax revenue.

Legal Person: A legal person is a human or non-human entity that is treated as a person for limited legal purposes. Legal persons can sue or be sued, own property, and enter into contracts. Corporations, partnerships, limited liability companies, and so on, all function as legal persons in business and election law.

Liabilities: A liability is something a person or a company owes, often a sum of money. Generally, it’s a financial obligation not yet settled between one party and another. For example, taxes are a liability for those being taxed. It’s important not to confuse liabilities with expenses where running a business is concerned. An expense is something a company incurs to generate revenue and their net income is given by their revenues minus their expenses. Liabilities, on the other hand, are obligations and debts that a company owes. Delaying payment of an expense generates a liability. The net worth of a corporation or the net wealth of an individual is the result of subtracting their liabilities from their assets.

Liquidity: Liquidity is the ability to sell an investment promptly and without penalty or otherwise incurring a loss.

Lorenz Curve: The Lorenz Curve, named after the American economist Max Lorenz (1876-1959), provides a graphical representation of the way that income or wealth is distributed within a population. It plots percentiles of the population against the cumulative income or wealth of everyone at or below that percentile. The Lorenz Curve and associated statistics are used to measure inequality in populations, but it does so imperfectly because it requires fitting a continuous curve to incomplete and thus discontinuous data. The curve is often accompanied by a straight diagonal line with slope 1 that represents perfect equality. The Lorenz Curve lies beneath it and displays the observed or estimated distribution. The area below the line of perfect equality minus the area below the Lorenz Curve, all divided by the area below the line of perfect equality gives the Gini Coefficient, a numerical index of inequality. See Gini Coefficient.

Marginal Tax Rate: A marginal tax rate is the rate of tax you pay on every additional dollar of income over a certain amount. For the United States, this rate increases for individuals as income rises. This method of progressive taxation has the goal of taxing individuals based on their income so that high-income earners are taxed more than low-income earners. There are seven different marginal tax rates that determine seven different tax brackets in the United States. Most wealth tax proposals also involve marginal tax rates establishing different tax brackets.

Net Wealth/Worth: Net wealth is determined by subtracting the liabilities of an individual or company from its assets. An asset is anything owned having monetary value, whereas liabilities are obligations or debts that decrease financial resources. An entity with positive net worth has assets that exceed liabilities and one with negative net worth has liabilities that exceed assets. Positive and increasing net wealth/worth indicates financial health and decreasing net worth can be a cause for concern, especially if it indicates an increase in liabilities relative to assets.

Pareto Principle: Named after the Italian economist, Vilfredo Pareto (1848-1923), the Pareto Principle states that 80% of consequences come from 20% of the causes. The principle was derived from the imbalance of land ownership in Italy and seems to hold as a general observation, but it is not a law and it has exceptions. It is commonly used to illustrate the fact that not all things are equal and a minority of people will own a majority of the wealth, or that in a business, a minority of the employees will drive most of the profits, or that in a voluntary organization, a few of the people will do most of the work.

Progressive Tax: A progressive tax is one that requires those with a higher income to pay a higher percentage of it in tax. It operates on the assumption that those with higher incomes can afford to pay more.

Property Tax: Property tax is paid on property owned by individuals or corporations. The tax is most often based on the assessed value of the owned property. The most common form of property tax is a real estate ad valorem tax, but it also is levied sometimes on tangible personal property like cars and recreational vehicles. It is a regressive tax.

Proportional Tax: A proportional tax or flat tax applies the same tax rate to everyone regardless of income.

Regressive Tax: A regressive tax imposes the same percentage on products or goods owned or purchased regardless of the buyer’s income and is thus considered to be disproportionately hard on low earners.

Securities: A security is an investment that is highly liquid and can be bought, sold, or traded on a public exchange (market). These investments can be either equity securities or debt securities. The most common kind of equity securities are stocks and the most common kind of debt securities are bills and bonds (the former involving an investment of principal a year or less and the latter being for a much longer term).

Tax Competition: Tax competition comes about when governments use reductions in taxation to encourage the inflow of productive resources and discourage the outflow of the same. This usually involves lower tax rates on individuals and corporations and is intended to attract business and investment by creating a comparative advantage.

Tax Havens: A tax haven is a jurisdiction, often a foreign country, that offers individuals or businesses in another jurisdiction little or no tax liability in a politically and economically stable environment while sharing very limited or no financial information with tax authorities in these other jurisdictions. Most tax havens do not require residency or even business presence to benefit from their tax policies.

Trusts: Trusts are established as fiduciary relationships in which the trustor gives another party, the trustee, the right to hold title to property or assets to benefit a third part known as the beneficiary. Trusts are established to protect the trustor’s assets and make sure they are distributed according to the wishes of the trustor. They can also reduce paperwork, save time, and be helpful in minimizing inheritance or estate taxes. Executors of wills, accountants, financial advisors and money managers, bankers, insurance agents, board members, and corporate officers all have fiduciary responsibilities.

Tragedy of Philanthropy: The tragedy of philanthropy is the thesis that government entitlement programs, financed through taxation, take resources from personal giving and drive out many private charities through competition and replacement. The tragedy is manifest in that government entitlement programs discourage private compassion and are less effective in helping the disadvantaged because they depersonalize both the giver and the receiver of charity. By interpreting the causes of poverty materially and environmentally, bureaucratic approaches to addressing it replace volunteers with government workers and disincentivize work, saving, marital stability, and mutual support within families and small communities. Private charities with personal volunteer involvement, on the other hand, operate on the principle that permanent change results when individuals are given personal attention, emotional support, and are morally challenged by being held accountable for their actions. This thesis has been advanced on the basis of historical studies and explored in various ways by the political scientist James L. Payne (1939 – ), the social scientist Charles Murray (1943 – ), and the academic journalist Marvin Olasky (1950 – ), among others.

Valuation: The quantitative process of determining the fair monetary value of an asset or of a whole firm is called valuation.

Wealth Tax: A wealth tax, sometimes also called a capital tax or equity tax, is levied on the net worth of some or all of the individual tax payers in a country. Often it is reserved for those whose net worth (assets minus liabilities) exceeds a certain specified amount. The assets in question would include such things as cash, bank accounts, corporate shares, fixed assets (property, plants, and equipment), pension plans, private homes, personal cars, and trusts.

References and Further Reading

Bunn, Daniel. (2019) “What the U.S. Can Learn from the Adoption (and Repeal) of Wealth Taxes in the OECD,” Tax Foundation Report. January 30, 2019. Available at: https://taxfoundation.org/wealth-tax-repeal-wealth-taxes-in-europe/.

Edwards, Chris, and Ryan Bourne. (2019) “Exploring Wealth Inequality,” Policy Analysis No. 881, Cato Institute, November 5, 2019. Available at: https://www.cato.org/sites/cato.org/files/2020-01/pa-881-updated-2.pdf.

Friedman, Milton. (2002) Capitalism and Freedom (40th Anniversary Edition). Chicago: University of Chicago Press.

Friedman, Milton and Rose. (1980) Free to Choose. New York: Harcourt, Inc.

Gilder, George. (2012) Wealth and Poverty: A New Edition for the Twenty-First Century. Washington, DC: Regnery Publishing, Inc.

Hayek, Friedrich. (1994) The Road to Serfdom (50th Anniversary Edition). Chicago: University of Chicago Press.

Hechler-Fayd’herbe, Nannette. (2019) Global Wealth Databook 2019. Credit Suisse Research Institute. October 2019. Available at: https://www.credit-suisse.com/media/assets/corporate/docs/about-us/research/publications/global-wealth-databook-2019.pdf.

Holtz-Eakin, Douglas, and Gordon Gray. (2020) “Wealth Tax and Workers,” American Action Forum Research. January 10, 2020. Available at: https://www.americanactionforum.org/research/wealth-taxes-and-workers/#_ednref6.

Li, Huaqun, and Karl Smith. (2020) “Analysis of Sen. Warren and Sen. Sanders’ Wealth Tax Plans,” Tax Foundation Report. January 27, 2020. Available at: https://taxfoundation.org/wealth-tax/.

Murray, Charles. (1984) Losing Ground: American Social Policy 1950-1980. New York: Basic Books.

Olasky, Marvin. (1994) The Tragedy of American Compassion. Washington, DC: Regnery Publishing, Inc.

Payne, James L. (1998) Overcoming Welfare: Expecting More from the Poor and from Ourselves. New York: Basic Books.

Piketty, Thomas. (2014) Capital in the Twenty-First Century. Cambridge, MA: Harvard University Press.

Richards, Jay W. (2010) Money, Greed, and God: Why Capitalism is the Solution and Not the Problem. New York: HarperOne.

Sachs, Jeffrey D. (2005) The End of Poverty: Economic Possibilities for Our Time. New York: Penguin Books.

Sachs, Jeffrey D. and the United Nations Sustainable Development Solutions Network. (2018) Closing the Sustainable Development Goals (SDG) Budget Gap. Move Humanity: A Wealth and Justice Initiative, October 2018. Available at: https://movehumanity.org/wp-content/uploads/2018/10/FINAL-2018-10-18_Closing-the-SDG-Budget-Gap.pdf.

Saez, Emmanuel and Gabriel Zucman. (2019) “Progressive Wealth Taxation,” Brookings Papers on Economic Activity, September 5-6, 2019. Available at: https://www.brookings.edu/wp-content/uploads/2019/09/Saez-Zucman_conference-draft.pdf.

Samuelson, Paul and William Nordhaus. (2009) Economics, 19th edition. New York: McGraw-Hill Education.

Sanders, Bernie. (2019) “Tax on Extreme Wealth.” Available at: https://berniesanders.com/issues/tax-extreme-wealth/.

Sowell, Thomas. (1995) Vision of the Anointed: Self-Congratulation as a Basis for Social Policy. New York: Basic Books.

Sowell, Thomas. (2007) Conflict of Visions: Ideological Origins of Political Struggles (revised edition). New York: Basic Books.

Sowell, Thomas (2009) Applied Economics: Thinking Beyond Stage One (second edition). New York: Basic Books.

Sowell, Thomas. (2011) Economic Facts and Fallacies (second edition). New York: Basic Books.

Sowell, Thomas. (2015) Basic Economics: A Common Sense Guide to the Economy (fifth edition). New York: Basic Books.

Sowell, Thomas (2019) Discrimination and Disparities (revised and expanded edition). New York: Basic Books.

Summers, Lawrence and Natasha Sarin. (2019) “A ‘Wealth Tax’ Presents a Revenue Estimation Puzzle,” The Washington Post, April 4, 2019. Available at: https://www.washingtonpost.com/opinions/2019/04/04/wealth-tax-presents-revenue-estimation-puzzle/.

Wamhoff, Steve. (2019) “The U.S. Needs a Federal Wealth Tax,” Institute on Taxation and Economic Policy Report. January 2019. Available at: https://itep.org/the-u-s-needs-a-federal-wealth-tax/.

Warren, Elizabeth. (2019) “Ultra-Millionaire Tax.” Available at: https://elizabethwarren.com/plans/ultra-millionaire-tax.