1 Market Caps Run Amuck

In January 1999, I was at a Liberty Fund conference in Tucson having breakfast with a savvy old finance guy as he was reading the Wall Street Journal over coffee. He couldn’t believe the market capitalizations of various newly formed Internet companies. He kept comparing the market caps of these new companies (total number of shares multiplied by the going price of each share) with the market caps of other well-established blue-chip companies, and how the former were trouncing the latter.

The dot-com bubble was in full bloom at the time and still had well over a year to go before it burst. Stocks on the Nasdaq were going crazy, rising 400 percent between 1995 and the peak in March 2000. Tech and internet companies that had no actual products or prototypes or even detailed plans for products were receiving enormous valuations simply on a promise and a prayer. In the housing crisis several years later, NINJA loans were the problem and the joke: lending money to lenders with No Income and No Job or Assets. In the dot-com bubble, Potemkin companies were the problem and the joke: all façade and no substance.

Fast forward to the present, and we see incredible market caps again, even more extreme than in times past. Take Apple. In August 2018, Apple was the first company to hit a market cap of $1 trillion. Two years later, August 2020, it was the first company to hit a market cap of $2 trillion. Today, on October 15, 2021, its market cap is the highest of any company and sits at $2.377 trillion. That’s a 137 percent increase since August 2018. Microsoft is at the moment just behind Apple with a market cap of $2.265 trillion. Back in August of 2018, its market cap was $861 billion, so its percentage increase since then has been even greater than Apple’s: 163 percent.

Leaving aside Saudi Aramco (an oil company) and Berkshire Hathaway (a finance company heavily invested in Big Tech). the top ten companies with the largest market caps are all Big Tech. In addition to Apple and Microsoft, these include, in decreasing order of market capitalizations, Google, Amazon, Facebook, and Tesla. The smallest of these is Tesla, with a market cap of $833 billion. Since by any realistic measure of productivity, the rate at which market caps of these companies is rising far outstrips what these companies are actually producing or even promising to produce, it would seem that the rise of these market caps is inflationary: it costs increasingly much to buy a stake in these companies even though the money being spent correlates with less and less value produced.

That of course raises the question whether we are also witnessing an emerging tech bubble. That’s less clear than the threat of inflation, whose beginnings we are now witnessing in real time. What seems to keep any such tech bubble from bursting, at least for now, is a TINA problem (There Is No Alternative). The Big Tech companies enjoy a monopoly status in huge markets and are very profitable. So even though their P/E ratios are crazy high, demand for them remains strong. Combine that with a sinking dollar, and they likely won’t suffer much. Tesla might be the exception, as their monopoly on EVs is steadily eroding. And yet for the moment Elon Musk and Tesla are thriving as never before (see below).

2 Billions and Trillions

The number billion used to grab our attention, but not anymore. It now takes a trillion to impress us. Carl Sagan in the late 1970s would intone in his Cosmos television series about the “billions and billions” of stars and galaxies out there, and it became a national joke. In the 1980s, Derrell Delamaide wrote Debt Shock: The Full Story of the World Credit Crisis. In it he lamented that various Central and South American countries were about to default on their loans, amounting at the time to between $30 and $80 billion. These defaults were supposed to trigger a global financial meltdown (never happened — the debts were simply refinanced and kicked down the road). Such numbers (even with inflation factored in) now seem like chicken feed.

Even in the Clinton years, deficits in the hundreds of billions seemed like a lot. Billions of dollars have given way to trillions of dollars, much as gigabytes (billions of bytes) have given way to terabytes (trillions of bytes). In the new economy, trillion is the number to beat.

3 Blue-Chipper Market Caps

Even though what’s happening with trillions is commanding our attention, what’s happening currently with only billions is nonetheless economically instructive. According to CompaniesMarketCap.com, America’s three largest manufacturers of traditional gas-powered automobiles are, by market cap, exactly those you would expect:

- GM, with a market cap of $84 billion.

- Ford, with a market cap of $63 billion.

- Fiat Chrysler, with a market cap of $31 billion.

Compared to other market caps, these numbers are remarkable for their puniness. Take Square, the brain child of Jack Dorsey, Twitter’s founder, where the big idea with Square is to connect a credit card reader to a smart phone and allow for credit card payments to occur more conveniently. A good idea, to be sure, but not brilliant (smart phones are, after all, universal computers, and universal computers can be programmed to do anything that’s programmable — so if dedicated digital devices can read credit cards, so can smart phones).

So here’s the billion-dollar question: Doesn’t it seem excessive that Square should have a market cap of $114 billion, essentially that of GM and Chrysler combined?

Square employs about 5,500 people and its net income for 2020 came to $213 million. By comparison, GM employs 155,000 people and its net income for 2020 came to $6.4 billion. The disparity between the size and scope of these companies seems stark. Yet the much smaller enterprise has a significantly bigger market cap. Square, unlike GM, is also a card carrying member of Big Tech.

Or compare GM with Tesla. Tesla’s market cap is $833 billion, or ten-fold more than GM. Yet in 2020 Tesla produced only around 510,000 vehicles compared to GM’s 6,829,000, and its net income was only $721 million compared to GM’s $6.4 billion. True, Tesla has had a great first two quarters in 2021, with a net income of $1.5 billion (it has yet to announce third-quarter earnings). But even these latest numbers seem unexceptional for traditional car manufacturers with much smaller market caps (such as GM).

Granted, the future may belong to electric vehicles (EVs), and for now Tesla seems poised to control the commanding heights for this industry (though how long it can maintain its first-mover advantage is questionable). Yet even the future of EVs seems less than assured. Internal combustion-based vehicles still possess significant advantages, not least range. Moreover, the “greenness” of EVs is questionable given not only that most of the electric energy in their charging ultimately derives from fossil fuels, but also that there’s significant pollution involved in the manufacture of their batteries (see, for instance, “The Great Electric Car ‘Zero Emissions’ Boondoggle“).

In all this, it’s not as though the more staid traditional companies like GM have seen their market caps stay flat. If we use August of 2018 as our baseline (the point at which Apple was the first company to hit a market cap of $1 trillion), we see that GM back then had a market cap of $51 billion. So by rising to a market cap of $84 billion currently, it’s also seen a solid increase in its market cap: 65 percent. By comparison, Tesla’s market cap in August 2018 was $51 billion, the same as GM’s. By rising to $833 billion currently, it has seen a jaw-dropping percentage increase over the last three years of 1,500 percent (a ten-fold increase beyond even Apple’s percentage increase during that time).

4 Market Caps Outside Big Tech

There’s something surreal about these wildly increasing market caps. It’s not as though net income or productivity of Big Tech companies like Apple, Microsoft, Google, or Amazon has proportionately increased anywhere near as much as their market caps.

Tesla is perhaps the exception because in 2018 it was operating at a $2 billion deficit and its production was only 100,000 vehicles annually (compared to 500,000 today). But Tesla was at the time a company hanging on for life. Its rebound has been true enough, but by any realistic gauge of actual performance and accomplishment, its results are not overly impressive. The promise of Tesla is that it will fundamentally disrupt the traditional automobile industry and come to dominate the EV industry, with which it intends to supplant fossil-fuel powered vehicles.

But it’s hardly clear how long Tesla can maintain its first-mover advantage in the EV industry. Already smaller EV manufacturers are creating vehicles that challenge the performance of Tesla EVs (compare the Lucid Air; see also our article “Expensivity Accelerated,” which reviews the highest performance EVs out there — including EVs in the million-dollar range).

Gargantuan market caps, however, are not confined to stocks. Cryptocurrencies are seeing huge market caps as well (see CoinMarketCap.com). At the time of this writing in mid October 2021, Bitcoin is again over $60,000 per bitcoin and the market cap of Bitcoin is over $1.16 trillion (that’s the total value of all bitcoins produced to date). The market cap of Ethereum is presently over $450 billion. And the combined market caps of all cryptocurrencies listed at Coin Market Cap is almost $2.5 trillion.

If we think of cryptocurrencies as currency (and there’s a lot to commend this view), then cryptocurrencies represent an addition of $2.5 trillion in liquidity and thus a $2.5 trillion increase in the money supply worldwide. If we take seriously economist Milton Friedman’s claim that “inflation is always and everywhere a monetary phenomenon,” then cryptocurrencies represent another spur to inflation (added to the inflation in the market caps of stocks).

If we stretch the idea of market caps to include the money supply (yes, its a big stretch!), then we see that M2 money (which is perhaps the best indicator of the money supply) went from about $14 trillion in August of 2018 to $21 trillion a the present moment, an increase of 50 percent. This is hefty, and, again, if we take inflation as a monetary phenomenon, then we should see this increase as tightly correlated with inflation. And yet, with stocks and cryptocurrencies seeing their market caps so far exceed these increases in the money supply, it seems that investing in stocks and crypto may be a way of staying ahead of inflation. Maybe — more on this shortly.

If we stretch the idea of market caps to include the total value of a given item that’s readily traded (less of a stretch than with the money supply), then we can look at the market cap of commodities such as gold. Throught 2020, the total gold extracted by people ever since people began extracting gold from the earth comes to about 200,000 metric tons (which can fit into under 4 Olympic sized swimming pools) or 6.43 billion troy ounces, which at the current spot price of gold at $1,775 per troy ounce comes to a grand total of $11.4 trillion. If we think of this as the market cap for gold, then it is less than the combined market caps of the six top listed stocks (i.e., Apple, Microsoft, Aramco, Google, Amazon, and Facebook).

This just seems incredible. Gold, if you go back to the early part of the 20th century (and also earlier) wasn’t just a form of money but was the first thing people thought of as money (with silver a close second). To this day, some economists think that gold remains the quintessential money and that the best thing that could happen for the economy is that we returned to a gold standard. I have no stake in that debate, but it is strange to think that all cryptocurrencies taken together have achieved about 20 percent of the total value of gold.

It also strikes me as strange that while so many other “stores of value” (such as stocks and cryptocurrencies) are seeing wild increases in price, gold, which for a significant portion of human history was the quintessential store of value, has been seeing essentially no increase in price. If we go back to our August 2018 baseline when Apple first hit a $1 trillion market cap, we see that gold was at about $1,500 a troy ounce, so it’s increase from then to now has been a paltry 18 percent.

5 Destroying the Middle Class?

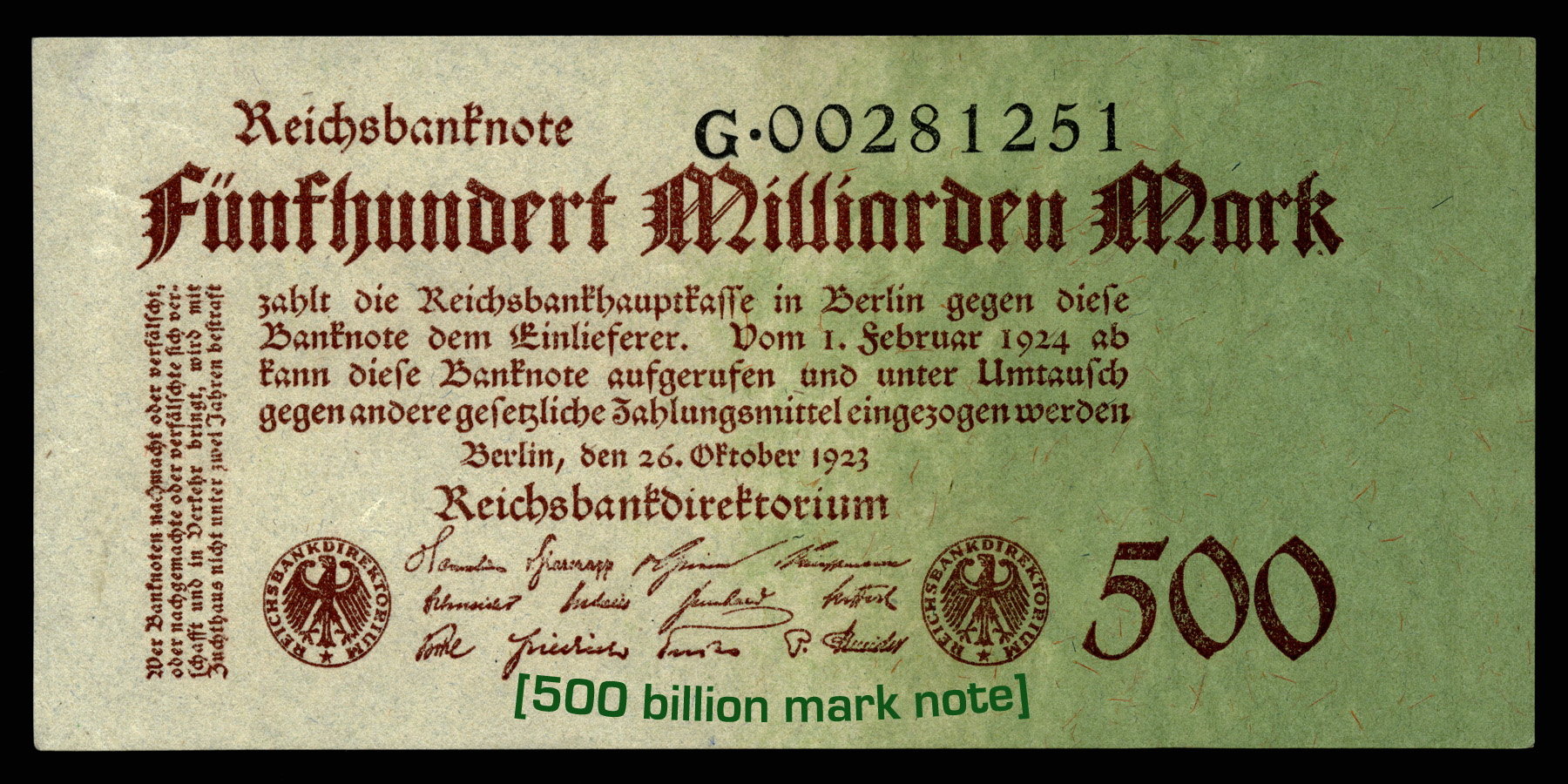

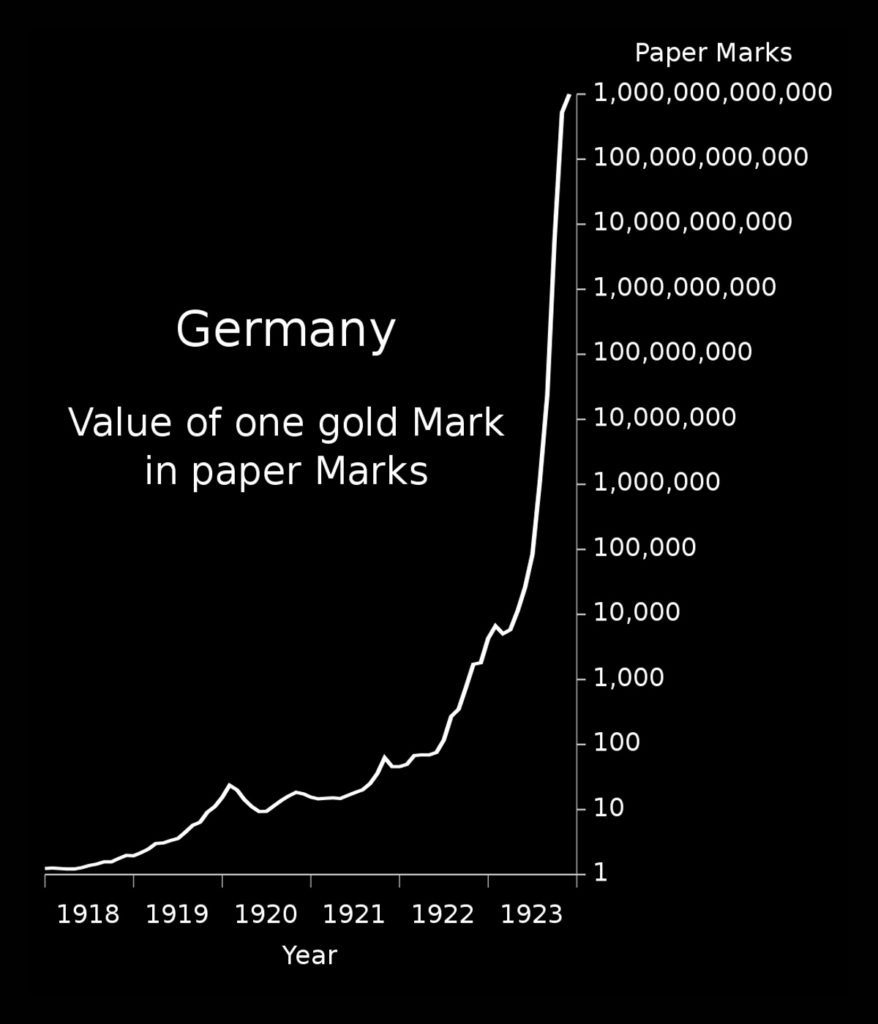

I’m a baby boomer, and I still remember talking to friends and relatives who lived through the German hyperinflation of 1921-23. I’ve even held in my hands billion mark notes that were not worth the paper they were printed on. One of the more noteworthy things about the German hyperinflation is that the middle class, which with German frugality had saved its money and deposited it at the bank, got hit hardest, losing everything.

By contrast, wealthy German families, such as the Krupps, did just fine. Neither wars, nor the Nazis, nor the German hyperinflation seemed to slow them down. They held assets that would retain their value despite extreme economic vagaries.

Unlike the Krupps, who owned factories and land, the wealthiest American families and individuals these days have their assets in digital and technology enterprises. It’s unclear if those assets can withstand a truly uncontrolled hyperinflation on the order of magnitude of Germany’s during the 1920s, especially since our tech titans depend so much on “lower class” consumers to keep their enterprises afloat.

But our “upper classes” might do quite well with a brisk rate of inflation that’s even in the double digits (we are currently half-way there). This would be an inflation that keeps their digital assets (as represented in tech stocks and cryptocurrencies) well ahead of inflation but leaves the vast majority of Americans with less and less purchasing power. (Note that the reference here to “upper” and “lower” classes is not intended pejoratively, but rather to highlight and push back against the recent tweet by economist Jason Furman that inflation is a “high class problem.”)

No doubt there will be a government safety net for the dependency class. Perhaps the dependency class will be happy to live off of government largesse, receive a guaranteed income, and forgo meaningful work. The ancient Romans used to talk about “bread and circuses” as keeping the plebs (“lower class”) happy. Perhaps nowadays it’s “fast food, social media, and video games” that will keep the plebs happy.

But to the traditional middle class, whose livelihood depends on working for a living rather than living off a dole on the one hand or living off capital investment on the other (that’s what defines it as “middle class”), such a level of inflation would be devastating. Indeed, we seem to be entering a perfect storm for a type of inflation that benefits the rich, assuages the poor, and destroys the middle class.

Interest rates are near zero. In consequence, the term “fixed income,” which used to refer to bond investments and to suggest a safe and stable way to earn income from savings invested at interest, has lost its appeal. In order to stay ahead of inflation, even a modest inflation, you now need to be investing in things like stocks and cryptocurrencies.

Even gold constitutes a problematic investment, at least for now, because its price is being manipulated and kept artificially low: Central banks are able to drive down its price not by selling real gold (in fact, they are currently buyers of gold). Instead, they use the COMEX “paper gold” futures market to drive down the price of real gold, making it cheaper for them to buy. About 100 times the dollar value of real gold trades are conducted in the COMEX gold futures market, none of it backed by an unconditional promise of physical delivery.

Nor does real estate offer a safe haven for the “lower class.” Most American’s who claim to own a home find that the bank in fact owns the majority of their home. As it is, most American have no significant investment in the types of assets that will actually increase their wealth and keep their net worth rising ahead of inflation. In particular, they are unable to cash in on the stocks whose capitalization has gone through the roof in recent years.

What’s behind this perfect storm that seems ready to undo the middle class? I’m no conspiracy theorist, but it does seem that market and political forces can collaborate to produce what looks like a conspiracy. It’s clearly in the interest of Big Tech to see their stocks rise to ever increasing and unprecedented heights. Moreover, Big Tech’s lobbying of politicians in Washington ensures that nothing will stand in the way to prevent their wealth from continuing to surge.

And so their wealth continues to grow at a pace and magnitude unprecedented in human history (leaving off, perhaps, the conquerors of the past who dispossessed entire nations, such as Alexander the Great). Elon Musk started 2020 with a net worth of $27 billion. His net worth stands, at the time of this writing in October 2021, at over $200 billion. With this rate of wealth increase, Musk and his fellow “high class” tech titans (such as Bezos, Page, Bryn, and Zuck) have nothing to worry about even with a rate of inflation in the double digits.

But what about the rest of us “low class” people who want to maintain our self-respect, care for our families, do meaningful work, and not constantly look over our shoulders to see whether we’re earning enough to stay ahead of inflation and avoid bankruptcy — in other words, what about the middle class? Unlike the tech titans, America’s middle class has much to worry about with Big Tech’s absurd market capitalizations.