Between a jump in the median home sales price amounting to $33,000 and soaring mortgage interest rates, the cost of buying a home in 2023 is twice what it was two years ago. Why are home prices through the roof in 2023?

The simplest explanation of why homes for sale now cost so much is that housing demand currently exceeds housing supply. Nationwide, prospective homebuyers in modest to moderate markets are encountering a painful shortage of homes to purchase.

The housing market crisis affects buyers (and even renters) across all age groups. Young people can’t forge ahead in their adult lives and are instead stuck living with their parents well into their 20s and 30s (and beyond) or throwing away thousands of dollars on rent without building any equity in return. Growing families who need more space can’t afford to upgrade from their modest starter homes to a larger, but not luxury, home. Seniors and empty nesters who want to downsize can’t move into a home that better fits their needs.

No one’s winning, except maybe the institutional investors who are capturing an increasing share of existing home sales.

[To learn more about the challenges facing American households, jump to our article about how inflation is impacting everyday consumers.]

How Supply and Demand Applies to the Housing Market

Nationwide, there are a great deal more prospective buyers looking for homes than there are sellers with homes for sale. In many markets, the number of homes for sale has reached historic lows.

With the housing demand exceeding supply, homebuyers are having to compete with each other. Making the highest and most competitive offer lands buyers the house. As more potential buyers increase their bids to strengthen their chances of getting the home, it drives up the price of the house.

In the housing market, prices are based in large part on comparative market analyses of the sales prices of houses with similar sizes and features that have recently been sold in the same area. As bidding wars that result in above-list-price offers have become more common, it isn’t only the sales prices of these houses that have increased but also the data on which comparisons and estimates are made.

The obvious question is why such an imbalance now exists in the housing inventory. What’s suddenly causing demand to outpace housing supply so drastically?

[Are you an aspiring homeowner? Times are tough out there. Improve your chances of finding your new home with a look at these ten steps toward home ownership.]

The Impact of Institutional Investors on Housing Costs

In many cases, the winners of the bidding wars and buyers of this limited supply of houses aren’t people at all. They’re Wall Street institutional investment firms backed by trillions of dollars of revenue.

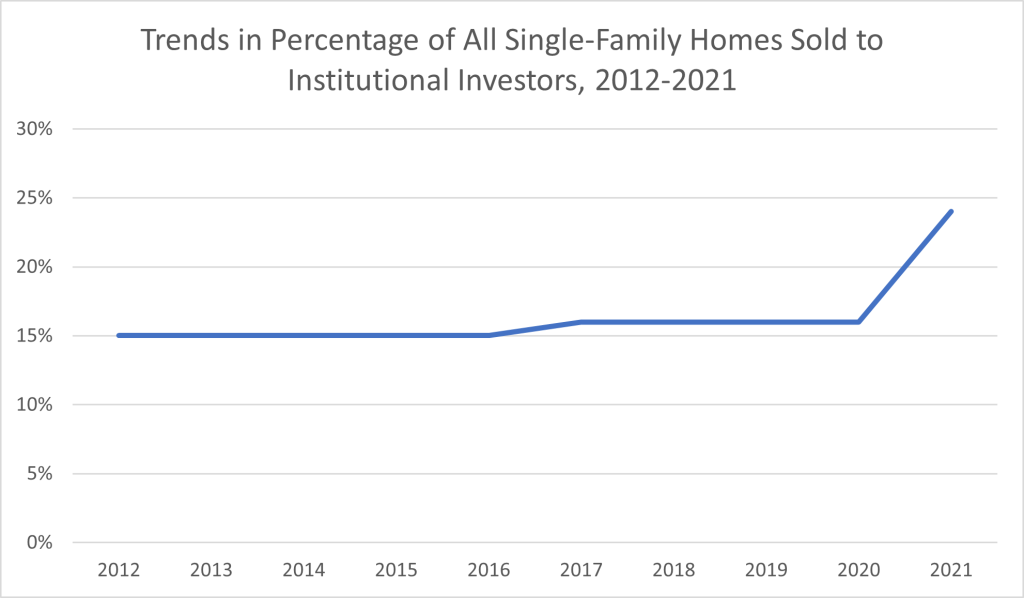

A TIME article published in 2023 reported that investors bought 24% of all single-family homes in 2021, citing an analysis by Pew Stateline. With one in four homes on the market going to people who aren’t even living in them, it’s no wonder that prospective buyers are having a harder time finding—and affording—a home that meets their needs. The percentage of the total housing market that “mega” investors—companies that own at least a thousand homes—purchased increased from 1% in 2021 to 3% in 2022.

“Wall Street has purchased hundreds of thousands of single-family homes since the Great Recession,” CNBC reported in February 2023.

Investors contributing to home sales isn’t a new phenomenon. When foreclosure rates rose during the Great Recession, investors began buying houses at relatively low prices, and they have now been treating single-family homes as profit-turning rentals for more than a decade. What is new is the much larger proportion of homes these investors are snapping up in the name of financial gain. Between 2012 and 2021, investors accounted for only about 15% to 16% of home sales, TIME reported. The 9% increase in the percentage of homes investors were buying compared to just a year before is disrupting the housing market, particularly while the supply of houses available to buy is dwindling.

Looking at the percentage of homes sold to institutional investors is only one way to understand the scope of this issue. We can also learn a lot from the increase in how many more houses these investors are purchasing. Compared to the number of single-family homes institutional investors purchased in 2020, the number of homes sold to these investors in 2021 reflected an 80% increase, according to real estate company Redfin.

This trend of institutional investors scooping up much-needed houses may just keep getting worse. Citing a report by MetLife Investment Management—itself an institutional investment management business—CNBC reported that institutional investors could control as much as 40% of single-family rental homes by the time 2030 rolls around.

Another novel piece of the puzzle is the type of houses investors are buying. By and large, we’re not talking about the rich buying yet another mansion or vacation home but rather about investors snagging smaller, cheaper properties—the same ones that middle-income Americans are looking to purchase or rent.

At the end of August 2023, Redfin reported that 23% of low-priced homes in the second quarter of the year were purchased by investors. The percentage of low-priced homes investors purchased during the second quarter of 2023 was lower than the 25% peak of the previous year. However, Redfin reported that it was still “much higher than investors’ market share for more expensive homes.” Investors also bought 11% of mid-priced houses and 14% of high-priced homes, according to Redfin. Nearly 40% of the homes that investors purchased during the second quarter of 2023 were considered “small” homes, with a square footage of 1,400 or less.

In other words, these large institutional investment companies are buying up the homes that average would-be homebuyers want to purchase. With a shortage of affordable houses to choose from and the growing cost of purchasing a home, these families are often forced to rent instead of buying their own home. Their rent builds more equity in the house for the investor, as well as an income stream. That’s just what many investors want: renters, not buyers. The percentage of sales listings of homes currently owned by investors shrunk from 13% to just 8% in the first half of 2023, Redfin reported.

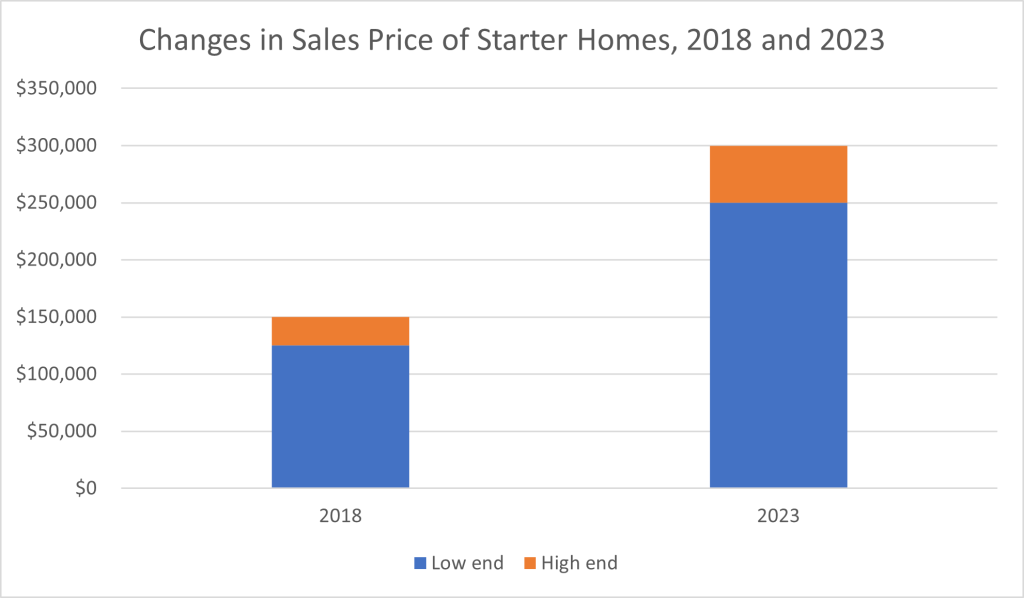

What used to be inexpensive starter homes valued between $125,000 and $150,000 15 years ago now cost between $250,000 and $300,000, a Yahoo! Finance article reported in April 2023.

There’s money for investors in these small and comparatively low-priced rental properties because families need a place to live, even during troubling times like a recession or a pandemic. Unlike individuals who rent out a property—and, by the time they factor in property taxes, upkeep, and insurance, may not even break even—these companies enjoy a lot of perks that make renting out property more profitable.

For one thing, unlike the average individual or small group, they have the resources to weather short-term financial losses, such as the cost of repairs or downtime between paying tenants, as long as the investment pays off in the long run. Unlike a homebuyer who intends to actually live in the property and needs to make sure it meets their needs, investors can buy a house as-is, even without ever seeing it. Not having to deal with inspections and requests for potentially expensive repairs makes these offers appealing to the seller.

The institutional investor may even have the financial resources to make a cash offer, in which case the high mortgage rates are irrelevant. Buying properties outright gives institutional investors a significant advantage over homebuyers, the Urban Institute reported in 2021 (and mortgage interest rates have only increased since then). When institutional investors can’t pay cash for properties, they may still get a better deal than the average American. According to federal and state legislation tracking software company BillTrack50, investment firms “usually have access to far more money for a far lower interest rate.” They may be overpaying for the house itself in order to outbid the people who want to actually live in the home, but they can afford that extra expense since they aren’t paying the high interest rates individuals have to pay for a mortgage.

Major institutional investment companies aren’t the only investors gunning for the housing market. Many smaller investment groups and individual investors are also purchasing real estate for financial gain, either to rent out or to “flip” and resell in hopes of turning a profit. However, these institutional investment firms not only have more purchasing power to make these transactions but also some unfair advantages over individuals and localized investment groups.

The biggest names in institutional investment housing purchases, the ones you encounter again and again, are BlackRock, Vanguard, and State Street. Together, these companies comprise the “Big Three” index fund managers. A 2022 article published in The New York Times put their combined managed assets amount at $22 trillion, more than half of the total value of all shares for S&P 500 companies. At one time (at least as recently as 2019, per an article published in the Harvard Business Review), one of the Big Three was the largest shareholder in 88% of S&P 500 companies. In other words, BlackRock and these other companies can produce hundreds of thousands of dollars with little notice and withstand the costs of significant repairs and renovations. They have plenty of resources to produce a cash offer that beats out the best offer the “little guy” in need of housing for his family can make.

[In tough economic times, job security is critical. To learn more, check out our list of 10 Recession Proof jobs.]

How Population Shifts Have Fueled the Housing Demand

Not all of the blame for the current housing crisis relates to corporate greed. To some extent, researchers have concluded that population shifts are part of the reason housing demand has remained strong.

Homebuyer Demographics

Who buys a house? It isn’t only young people just starting out.

It’s the natural order of life in America that, at some point upon reaching adulthood, young people move out and start their own lives in homes away from their parents and family of origin. For many people, eventually owning a home is part of the plan.

There are a variety of practical reasons for pursuing home ownership, from building home equity and financial assets to the security of knowing that you aren’t at the mercy of a landlord who could suddenly raise your rent. There are also emotional reasons to buy a house, such as the safety and freedom of having a place to live that’s yours and the achievement of a recognizable accomplishment. Owning a home is a critical part of the American dream.

Some young people buy a starter home first and move into a larger house later on in their lives. Others rent or live with family until they are able to afford to buy a more permanent home. In either case, most such homebuyers are focused on the lower- to mid-priced housing market. They aren’t looking at bona fide mansions or flashy properties in high-end neighborhoods of the biggest, most expensive cities. Yet more moderate and even modest homes are now well out of their price range.

Those same modest to moderate houses are attracting another growing population of prospective homebuyers: the Baby Boomer generation. According to a March 2023 report by the National Association of Realtors (NAR), 39% of homebuyers were part of the Baby Boomer generation in 2022, marking a 10% increase from the 29% of homebuyers that were part of this generation last year. Millennials—both older and younger Millennials—made up 28% of homebuyers in 2022 compared to the 43% of homebuyers this generation constituted a year ago, according to the NAR market data. Generation X accounted for 24% of buyers in 2022, and the 18-and-up members of Generation Z grew from 2% to 4% of total homebuyers between 2021 and 2022.

Compared to the past, people are generally living longer and in relatively better health, which allows them to age in their own (old or new) homes rather than in nursing homes. As the large generation that is the Baby Boomers approaches life changes like the kids moving out and retiring from the workforce, many are looking to downsize, often into the same price level homes as first-time homebuyers. In fact, rather than the number of households headed by the Baby Boomers decreasing, this generation is increasingly creating more individual households (due to divorce or the death of one spouse), CBS News reported in September 2023.

That means the competition for the limited housing inventory out there would be strong even if institutional investors weren’t snatching up a quarter of low-priced homes on the market.

The Challenges Facing Homebuyers by Generation

On the one hand, more established homebuyers have somewhat of a leg-up on first-time buyers in this tough market. Downsizing Baby Boomers and Gen Xers who have lived in the same house for decades and already paid off their mortgages should see significant profits from the sales of their homes at the current inflated house sales prices. New entrants to the housing market are less likely to have such a chunk of money saved up to apply to a down payment.

It’s telling that the National Association of Realtors reported the number of first-time homebuyers in 2022 as 26%, down from 34% in 2021. Without the proceeds from the sale of another home, buying a home in this market is out of the budget for many would-be homebuyers. The generations most likely to be first-time homebuyers were younger Millennials (of whom 70% were first-time buyers), older Millennials (46% first-time buyers), and Gen Xers (21% first-time buyers).

Downsizing Boomers and Gen Xers are facing their own serious struggles in the housing market. Although they may have cash from selling a paid-off (or nearly paid-off) home, the cost of buying a new home can easily swallow up these proceeds. With the current housing prices, the sale of their former, often larger, home may not be enough to buy the house they’re looking for, especially if they’re changing geographic areas. If their house wasn’t fully paid off, or if they had outstanding home equity loans that had to be settled when the home was sold, they may have made a lot less selling their old house than they will need to buy a new house in this market.

As a result, many established homeowners will still need a mortgage even if they’re downsizing. Getting a mortgage is harder when the applicant is retired or nearing retirement. Even if they can qualify for the mortgage, buyers have to consider how much debt they will be able to take on—and still live comfortably—if they’re likely to be retiring soon and, in turn, seeing a considerable decline in their income. Meanwhile, younger buyers with decades of work ahead of them can better expect to earn a relatively consistent income by which they can pay their mortgage over 10, 15, or even 30 years.

Institutional investors notwithstanding, American homebuyers across generations are going through a rough time. Unfortunately, the state of the current housing market also makes this problem difficult to solve through the usual means.

The Reluctance to Sell in Such an Expensive Market

If the lackluster housing inventory is the root cause of the housing crisis, the answer may sound simple: increase the number of homes on the market. Unfortunately, it’s not that easy. Also contributing to the shortage of homes for sale is the hesitation of prospective sellers because of the housing market.

With such high home prices, you might think sellers would be eager to unload homes at prices that, at least a few years ago, they likely wouldn’t have dreamed of getting. For those for whom the sale would be pure profit—such as a second home, a vacation home, or a house they recently inherited—the strong market is certainly appealing. However, most would-be sellers aren’t in possession of numerous properties. They’ll need to go somewhere after they sell their house. Between the high home sales prices and the much higher interest rates (compared to most existing mortgages) that are used to finance these purchases, the cost of buying even a smaller house is, in many markets, prohibitive.

Many homeowners who have already paid off their mortgages—mostly in the Silent Generation and Baby Boomer generations—and who would otherwise be looking to downsize are instead holding off on selling their homes. After all, under the current housing market, these homeowners may have to spend more to buy a smaller home in a more desirable location than they would get for their larger, already paid-off house. It may not make sense to take on this debt, especially at such high (and continuing to rise) interest rates, right when these homeowners are approaching retirement age.

Instead, many older homeowners are staying in houses that may be too large for their needs and require more upkeep and utility costs than they want. Meanwhile, the prospective buyers who would be interested in the property are searching high and low for a house to purchase. It’s a lose-lose situation and can feel like a catch-22: until the housing market improves, these current homeowners won’t want to sell, yet improvement is unlikely unless the housing demand and supply become more closely aligned.

The Challenges of Building New Homes for Sale

If there aren’t enough existing homes for sale, why not find other ways to increase the housing inventory and reduce competition in this tough market? Wouldn’t building new single-family homes help ease this pressure?

In general, new single-family construction has seemed like a promising way to meet consumers’ real estate needs. Unfortunately, factors like the rising interest rates are now having a negative influence on home builder sentiment and, in turn, the future construction of new homes for sale. The National Association of Home Builders (NAHB) reported in August 2023 that a survey had shown a meaningful decline in builder confidence after seven months of steady increases. Other factors like a shortage of construction workers and the effects of inflation on materials have made building new construction an expensive endeavor. In densely populated areas, there may not be land on which to build new real estate projects.

That’s not to say that all new home sales are out of the question, but rather that just building new homes to make up for the shortage of existing homes isn’t a simple solution.

In August, National Association of Home Builders Chief Economist Robert Dietz urged policymakers to “enact policies at all levels of government that will allow builders to construct more homes to address a nationwide shortfall of approximately 1.5 million housing units.” Numerous states have legislation either currently or recently under consideration that would address the housing affordability crisis in some way. Several of these proposed laws and policies are aimed at preventing investors from scooping up new properties as soon as they hit the market.

What Does the State of the Housing Market Mean for the Average American?

A huge part of the current housing crisis is how widespread its effects are. Nearly 80% of Americans happen to fall into the middle-income (50%) or lower-income (29%) category, according to Pew Research. The low inventory of low-priced and moderately priced houses directly affects this huge segment of the population.

Tips for House Hunting in the Current Market

For people who are house hunting despite the current climate, knowing what you’re up against at least helps you plan your home search.

Your next step should be to find a real estate agent who fully understands your situation and your goals. The advice a real estate agent gives one house hunter with one budget, timeframe, and goal for their new home may differ from the advice they give another house hunter whose situation is different.

Speak with your real estate agent in the area where you are looking for a home about getting pre-approved for a mortgage and any tips to make your offers more competitive. For example, some agents may recommend seeking a mortgage through a local lender rather than a national lender, as sellers sometimes give preference to these offers. Having a significant down payment can also make your offer more appealing, as well as reduce the amount of money you have to borrow under the current sky-high interest rates, so keep making it a priority to save for your down payment. Remember, you can always look into refinancing once rates (eventually) go down.

You might have to be more flexible in your house search in the current climate than you would otherwise need to be. You may need to cross off some of the features on your wish list and think critically about features you would otherwise have considered “needs.” However, you should stand your ground on matters that are important to you.

For example, with the pressure to make the most attractive offer, some buyers are agreeing to waive inspection on existing home sales. “Waiving a home inspection comes with sizable risks,” Realtor.com cautioned. If you’re not comfortable with this risk, Realtor.com offers the alternative of asking for a home inspection “for informational purposes” only. You can’t ask the seller to make repairs or reduce the cost based on this inspection report, but it could help find out if you would be making a mistake that amounts to multiple hundreds of thousands of dollars by purchasing the property.

Finally, be patient. You may have to put in a couple (or several) offers on different homes over the course of your house hunt. Buying a house right now can be emotionally draining, time-consuming, and financially expensive. Know going in that getting exactly the house you want in a short span of time may not be realistic, and plan for your living arrangements in case finding your house takes longer than you would hope.

Giving Up on Buying a Home in This Unaffordable Market

When real people repeatedly have homes scooped out from under them by institutional investors’ cash offers, they may not want to resign themselves to the grueling and emotionally charged process of continuing to house hunt in a market where they’re likely to encounter more of the (disappointing) same. Some would-be buyers drop out of the house search entirely.

The Mortgage Bankers Association (MBA) reported that applications for mortgage loans had “declined to the lowest level since December 1996” during the week that ended on September 1, 2023. This drop, which represents a 28-year low, comes even after the average mortgage rate declined slightly from 7.31% the week before to 7.21%, the Mortgage Bankers Association reported.

While people who need housing as soon as possible may persist in their home search despite the dreary inventory of homes for sale and the (still) high mortgage rate, those who can are opting out of participating in this unaffordable real estate market. Even if home prices and mortgage rates aren’t getting worse compared to previous weeks or months, they’re also not getting better enough to inspire much confidence among average American consumers.

What does this mean? Adult children in their 20s, 30s, and beyond are still living with their parents—an arrangement that’s often at odds with their goals and vision for the future. It isn’t only the children for whom this living situation is less than ideal. Their parents, too, are finding that life at this stage isn’t what they had expected. They have less freedom than they thought they would after raising the kids to adulthood, and they may be taking on a larger financial burden.

Moving out to rent their own place is one option for these young adults who can’t afford (or find) a home, but the insane increases in housing prices aren’t limited to purchasing real estate. Rent costs have jumped, too. The national median rent price climbed from $1,828 in August 2021 to $2,052 in August 2023. This marks an increase of more than 12% and amounts to more than $2,600 extra per year compared to just two years ago. Compared to pre-pandemic times, the increase is even more notable. In the four years between August 2019 and August 2023, the national average rent cost rose more than 25%, from $1,637 to $2,052. Renters are now paying an average of $5,000 more for housing than they were four years ago, and they aren’t even building equity by doing so.

The Emotional Toll of the Housing Market Unaffordability Crisis

The insurmountable increases in interest rates and home costs are keeping growing families trapped in houses too small, while empty nesters are left puttering around homes that are too big and require too much upkeep. This market is preventing renters from making the jump to ownership and the financial benefits it brings. It’s putting out of reach the sort of opportunities that might require people to relocate, such as landing your dream job in a competitive industry or being closer to the grandkids.

Ultimately, the unaffordability of the current housing market is about much more than money. It translates to a loss of freedom and security for American buyers, homeowners, prospective sellers, and renters.

***

So where does this leave you, the consumer? It depends on your personal and financial situation. To better understand your situation, jump to our list of 50 questions that you should ask before buying a home.]