Warm weather got you itching to update your home interior? We’ve spent much more time at home lately, so there’s no better time to finish the job.

This time, though, we’re not talking about a new coat of paint, new furniture, or just some new pictures on the wall. We mean removing that wall completely or finally starting on the addition you’ve been dreaming of. Or maybe instead, put in that kitchen island you’ve always wanted.

But what’s the best way to pay for it? This article presents the top choices for the best credit card for remodeling and home improvement. Updating your home is within reach. We’ll show you how.

Best Credit Card for Remodeling and Home Improvement

For large and small home renovation projects, Wells Fargo Cash Wise Visa Card is the right credit card with cash back that can offer many perks, qualifying balance transfers, and benefits beyond those available from a home equity line of credit or other financing methods.

Keep reading to find out what we like about each card, but first, let’s talk a bit about how to choose a home improvement credit card.

Best Credit Card for Small-Scale Home Improvement: Wells Fargo Cash Wise Visa Card

We recommend the Wells Fargo Cash Wise Visa Card for small-scale home remodeling. Among the things making this card so great for a small-scale home remodel are the 0% APR on purchases, qualifying balance transfers, and bonus rewards.

What’s more, this rate with cash back lasts for the first 15 months for other purchases after the account opening. After that point, the interest rate jumps to a variable APR of 19.99% – 29.99%, so promptly paying off all that debt is essential. If you do, you’ve effectively received a no-interest loan for your home remodel.

Like Chase Ultimate Rewards points, the Cash Wise card offers a respectable flat rate of 1.5% on all purchases. Yeah, that’s right: everything. Because you’ve got enough to worry about when sprucing up your casa, you don’t want to have to track what you’re spending and where you’re spending it.

As a welcome bonus, you can buy supplies from a retailer that accepts Google or Apple Pay within the first 12 months after opening the account and earn an additional three points, or 1.8%, on all purchases. Aside from a balance transfer, it offers cash back on combined purchases months after the account opening.

There’s no annual fee with the card, which is nice. However, there’s also no annual bonus, which is something to be aware of. The purchasing flexibility and the generous 0% APR period make this a great no-drama credit card for small-scale home remodeling projects.

With the flexibility of the card and the list of benefits of the premier rewards program, it’s time to start swinging that hammer because financing the new-look interior of your house is easier than ever: on your schedule and at your pace.

Pros

- Spend $500 and get $150 back to help fund other aspects of the renovation, like new furniture.

- Aside from having no annual fee, there are no limits on the amount of cash rewards you can earn, and they never expire so long as the account stays open.

Best Credit Card for a Big Home Remodeling Project: Bank of America Customized Cash Rewards Credit Card

If you have a big home remodel project that needs to be done quickly, consider the next choice in our ranking, the Bank of America Customized Cash Rewards credit card. The 3% cash back on select categories, including home improvement and furnishings, makes it an excellent pick for a big project and qualifying balance transfers for other purchases.

The bigger the project, the bigger the purchase, and the bigger the cash back benefits on eligible purchases, even at gas stations. That makes the Customized Cash Cash Rewards card hard to beat months after account opening.

With Bank of America, you also get a 2% welcome bonus at grocery stores and wholesale clubs up to $2,500 a quarter in combined 2% and 3% categories. While it has a zero annual fee, there’s a lengthy 0% APR period on purchases made within 60 days of opening the account and lasting through the first 15 billing cycles.

After that time, the APR jumps from 13.99% to 23.99%, and there is a 3% fee with a $10 minimum. Plan things carefully, though, and you should be able to pay off all your home remodeling purchases without accruing any extra interest.

As you redeem rewards, you can also enjoy a healthy infusion of cash back in your pocket, helping fund other aspects of the project. These make the Customized Cash Rewards Card from Bank of America the card that keeps giving when remodeling your kitchen, bathroom, or living area.

Pros

- A no-annual fee card with available 3% cash back categories includes gas stations, online shopping, and dining, and Preferred Rewards Members earn up to an additional 75% on all cash back rewards.

- In case you weren’t aware, wholesale clubs offer great deals on supplies crucial for your home remodel, helping you save even more on the project. You continue to enjoy 1% cash back on all other purchases.

Best Credit Card for Additional Remodeling Projects: Alliant Credit Union Visa Signature Card

Suppose your project calls for more than just knocking out a wall or finally finishing up that basement bathroom. What makes the Alliant Credit Union Visa Signature Card a great choice for massive home improvement projects is the generous 2.5% cash back on eligible purchases up to $10K a month.

That kind of ceiling on your welcome bonus purchases is ideal for big-ticket construction. Moreover, that generous offer goes without any tricky categories, though you do have to be a credit union member to take advantage of this benefit for other purchases.

You can join after approval, although the card with cash back is only offered to those with excellent credit.

There is no annual fee for the first year after opening the account (annual jumps to $99 each year after). On the downside, there is no 0% APR introductory period after account opening, but at 17.24% to 22.24%, the APR on the card is slightly lower than average than other cards.

When all this is taken in whole, it’s clear for the largest of home remodeling projects — or adding an entire addition to your home — nothing competes with the Visa Signature Card from Alliant Credit Union.

Pros

- Aside from no annual fee, those generous cash back rewards can also be deposited straight into an Alliant checking or savings account, further padding the bottom line of your project.

- Estimated average yearly rewards from the card are estimated to be about $360.

Bonus: Other Home Improvement Credit Cards to Consider

The best home improvement credit card with cash back and qualifying balance transfers will depend on your specific needs and preferences. However, some other popular options include:

- Home Depot Consumer Credit Card

- Lowe’s Advantage Card

- Chase Freedom Unlimited (Chase Ultimate Rewards)

These cards offer various benefits, such as cash back rewards, promotional financing, and discounts on home improvement purchases.

How Much Does a Full House Renovation Cost?

The final bill for your renovation project will vary greatly, depending on the nature of the work, whether you’ll be doing it yourself or paying other people to do it. The size and complexity of your home also make a big difference.

If you’re planning home improvement projects, though, here are a few costs you can count on:

- The average home remodel will run you about $50,000, with kitchens and bathrooms the most expensive and bedrooms the most affordable. If you live in a city, that can add some extra expense. It’s not uncommon to pay as much as $200,000 for an extensive redo of your abode.

- Homeowners can typically calculate anywhere from $10 to $60 per square foot for a remodel, but some pay as much as $150 per square foot. That’s particularly true if there are some underlying issues with the space or if you’re updating an older home.

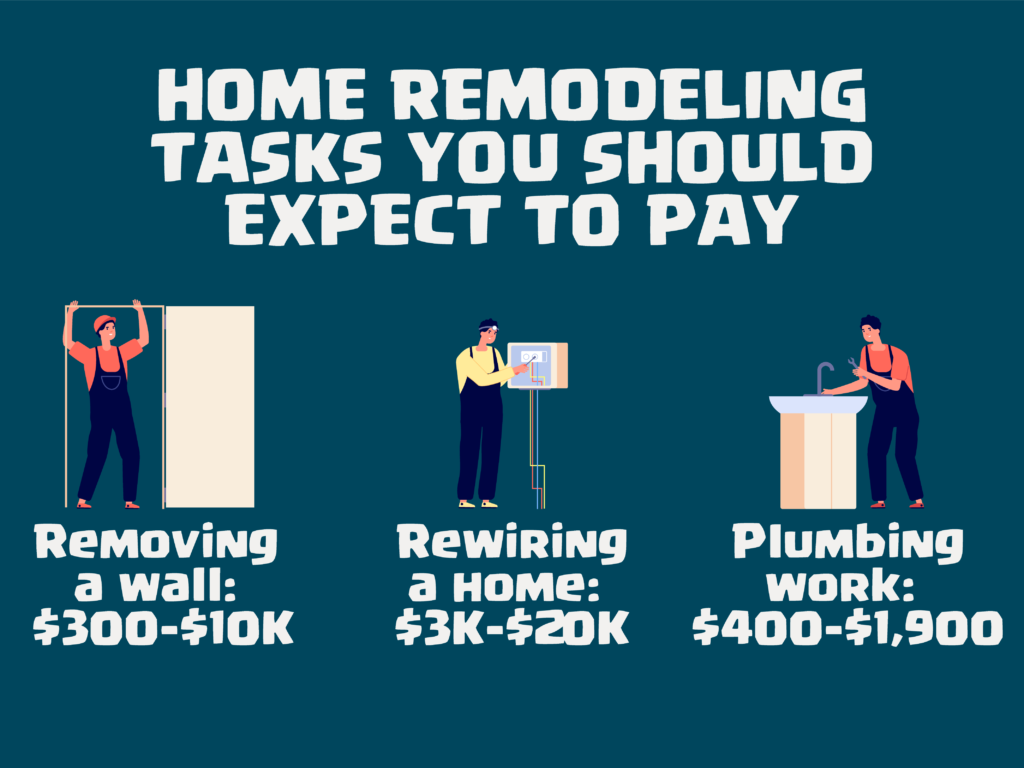

Generally speaking, here are some specific tasks related to a home remodel and how much you should expect to pay for each:

Removing a Wall: $300,000 to $10,000

Don’t start swinging that sledgehammer before you consult with a structural engineer. The last thing you want is to remove a crucial load-bearing wall. If it does happen to be a non-load-bearing wall, however, tearing it out will likely cost you less.

Rewiring a Home: $4,000 to $20,000

Wiring can be much less expensive in a new addition and before the new walls are all sealed up, so that’s something to consider. Whereas rewiring an old home, or even just a room in a house, can be pretty costly.

Plumbing Work: $400 to $1,900

Like electrical work, upgrading old plumbing costs much more than new pipes. Regardless of the plumbing work you need, expect to pay anywhere from $400 to $1,900.

Now that you know how much a remodel can cost, let’s discuss the best way to pay.

How Do You Finance a Home Renovation?

Many trips to home improvement stores may be in your future. However, paying with a credit card is only one of many ways to finance home improvement expenses. Paying for a home remodel on a credit card after careful budgeting and with a plan to pay back the debt right away offers many advantages.

Pay off the charges within a 0% APR introductory period, and you’ve received what amounts to a no-interest loan on the project. Furthermore, with the right credit card offering rewards on the purchases you make the most, paying for the work puts some cash back in your pocket.

There are other ways to pay for construction, however. Each with its own set of pros and cons. We’ll go over those, next:

Home Remodel Loans

Typically offered by banks, credit unions, and some online lenders, home remodel loans — sometimes called home repair loans — are unsecured loans to finance your project.

Plus, you don’t have to use your home for collateral. On the downside, eligibility is based on your credit score, an issue for many with a checkered financial history.

Home Equity Lines of Credit or Home Equity Loans

Home equity loans are like a second mortgage: take one out to finance the work and pay it back a little at a time. Home equity lines of credit often have lower interest rates, allowing you to take money out when needed and only as much as you need.

The drawback to both these options is that you must use your home as collateral, which can add extra time to your mortgage.

Mortgage Refinance

Or you could instead simply refinance your mortgage at a lower interest rate, funding your project with the difference. You could cash-out refinance or choose a rate-and-term refinance, each with pros and cons.

Be aware, though, that either option will require a home reappraisal — which costs money and takes time — and both will extend the life of your loan.

The last option for those interested in a house upgrade is government loans, such as a HUD Title 1 Property Improvement Loan or a cash-out refinance loan from the Department of Veteran Affairs.

How to Pay for Home Remodeling Using a Credit Card

Suppose you finance your home remodeling on a credit card. In that case, however, it’s always important to carefully budget the project and plan to pay back the debt without incurring any extra cost. Ensure the benefits do not change for other purchases after opening the account.

- A no annual fee and 0% introductory APR period is an enticing reason to pay for the work on plastic (or essentially a no-interest loan!). Once that introductory period is over, the average credit card interest rates are well over 20%! Don’t tack that kind of interest onto the project’s total cost!

- Bonus categories on credit cards may also be enticing. There are specific spending categories that a credit card issuer offers rewards or cash back for, such as dining, travel, gas stations, grocery stores, drugstores, home improvement stores, and more.

These categories typically rotate quarterly or annually and offer higher reward rates than the card’s standard rate for other everyday purchases. Cardholders can often earn additional rewards by using their card in these bonus categories.

Before deciding on the best home project credit card with cash back, it’s helpful to understand what renovations might cost you. Lastly, be sure to pay at least the minimum due on time to earn cash back.

How to Maximize Credit Cards for Home Improvement

Knowledge is power when making the most of credit cards for home improvement. You can create the conditions for a smooth renovation process that improves your living space and maximizes your financial gains by leveraging the right credit card and its features.

Home renovations remodels, and upgrades are expensive. You will make a lot of home improvement purchases. It’s essential to consider the potential return on investment and how the home improvement project may affect the value of your home.

Another way to save cash is to put some or all of the work on the right credit card.

- An annual fee credit card is a type of credit card that charges a yearly fee for access to its benefits and rewards program.

- These fees can range from a few dollars to several hundred dollars, and are often associated with premium credit cards that offer higher rewards rates, exclusive perks, and other benefits.

- While annual fee credit cards can offer great value for frequent users who take advantage of their benefits, there may be better choices for those who only use their credit cards occasionally.

Incentives

Even with an annual fee, the right credit card for your house upgrade should offer incentives and rewards on the stuff you need for the project, like paint, nails, screws, or even drywall. This could be a Lowe’s or Home Depot home improvement store card.

If you like comparison shopping, though, choosing a major credit card like the cards included in our ranking helps to keep your options open. The cards offer cash back points combined purchases months after the account opening

0% Introductory APR

In addition to credit, that not only rewards purchases most related to house renovations, although many cards offer a 0% intro APR or annual percentage rate with balance transfers. This means all purchases made within that period will be interest-free for other purchases months after the account opening.

Even if you have the cash to pay for the project, put it on the card and pay it off on time or within the grace period the credit company offers. Not only will your project be financed, but you’ll also earn cash back rewards while you’re at it with this intro APR offer!

Strategic Card Selection

Choose cards with sizable benefits and rewards for home remodeling purchases. Aside from a zero annual fee and welcome bonus, look for those offering cash back or points on purchases from contractors, home improvement stores, and hardware stores.

Introductory Offers

Many cards with cash back have tempting introductory offers, like 0% APR and a zero annual fee for a set time. This could be a game-changer because it will allow you to finance your home improvement project immediately without paying interest.

Some even have a welcome bonus where you can earn a statement credit. Furthermore, be cautious since some cards have an intro transfer fee for balance transfers completed within months of account opening.

Credit Card Rewards

Utilize the rewards earned from your card to defray the cost of home improvement. These advantages can significantly reduce your expenses, whether you use cash back or reward points for purchases.

In addition to rewards on construction gear and supplies, purchases made for the home remodeling project earn points. Those credit card offers can be spent on food to keep your crew happy, putting the finishing touches on the new room, or gas to make the dump run after demolition is complete.

Instead, use the points to reward yourself with travel because you’ll naturally want to leave the house once the project is finished. Some even offer cash back when dining at restaurants, including takeout and eligible delivery service.

How to Earn Credit Card Rewards When Financing Home Improvements

The ability to earn credit card rewards while financing your home improvements results from the fusion of strategic thinking and sound financial judgment. With careful planning, your renovation costs can be the foundation of an enriching experience beyond your home’s confines.

Be Strategic in Spending

To maximize rewards, charge your home improvement costs to the card of your choice. Whether it is a new kitchen countertop or a fresh coat of paint, every dollar you spend can go toward your rewards account.

Additionally, be on the lookout for foreign transaction fees and balance transfers for overseas orders. For some banks with an annual fee, balance transfers don’t earn cash back and use an intro balance transfer fee for each transfer on other purchases.

Maximize Your Rewards

Transform your earned rewards into statement credits or gift cards designed primarily for home improvement retailers. Even with an annual fee, this maximizes your rewards and gives your renovation efforts immediate value. Note that balance transfers do not earn cash back.

Time Your Purchases

Plan significant purchases to coincide with card promotions or bonus categories. This strategy can result in greater rewards while saving money as you make home improvements. Also, consider getting cards from banks with round-the-clock monitoring for unusual credit card purchases.

Related Questions

What Are the Benefits of Using Credit Cards for Home Improvement and Remodeling?

Convenience, cash back rewards, and promotion financing are the main benefits of using credit cards for paying for home remodeling and improvement. It’s a quick and easy way to finance your home improvement project and add value to your home. Some cards offer cash back, points, or credit card rewards for home improvement purchases.

When Would Other Cards and Strategies Be Better Than Credit Cards?

A HELOC might offer a more affordable financing option than credit cards when considering significant renovations. It is a viable option for more extensive projects because the interest rates are typically lower than cards. Depending on your credit rating and financial situation, a personal loan might provide fixed interest rates and a well-defined repayment schedule.

What Are the Disadvantages of Using a Credit Card for Home Remodeling and Improvement?

If not used wisely, credit cards can put you at a disadvantage due to high-interest rates and debt. Using a credit card can add to your overall debt load and impact your credit score if you can’t make timely payments. This is why it’s crucial to plan your purchases accordingly.

Conclusion

Putting home improvements on a credit card can be a smart and doable option. Consider your financial situation and determine if putting your home improvements on a credit card is the right choice for you.

Be sure to look at annual fee terms, welcome bonus, the opportunity for bonus points, credit limit, and the terms that apply before making a decision. No matter what financing option — or combination of financing options — you choose, that new addition, kitchen counter, or refinished basement you’ve been dreaming of is within reach.