When it comes time to buy a life insurance policy, the decision to purchase is only the first of many choices consumers need to make. Other considerations include what kind of policy suits both the present and future financial needs of the individual and their family, as well as how much that life insurance policy should be worth. It’s difficult to know exactly how much life insurance to buy, but with the help of a financial advisor, or with any one of the tips and tricks outlined in this article, it’s possible to come close.

The truth of the matter is, there’s no need to feel overwhelmed by the life insurance buying process. By the time you’ve read this primer, you’ll be well on your way, secure that the amount of life insurance you have is sufficient to protect you, your loved ones, and your assets. That way, you can get back to enjoying the things that truly matter most.

How Much Life Insurance To Buy

Outside of meeting with a financial advisor, a life insurance broker, or using any one of the many life insurance calculators available online, here are a few of the most common methods to settle on the correct amount of life insurance coverage to buy. Got a pencil and paper ready, or maybe a calculator up on your phone? Good. Let’s get started.

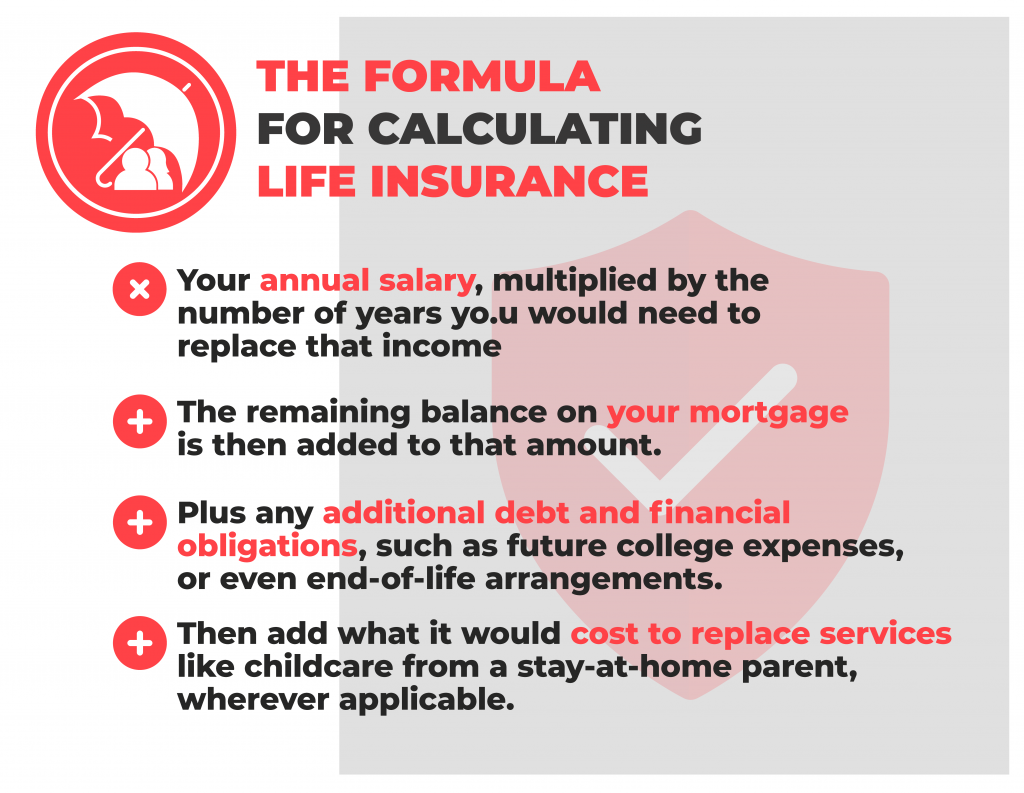

The Formula for Calculating Life Insurance

One common approach to determine how much life insurance to buy is to calculate the amount manually.

Begin by adding up the following:

- Your annual salary, multiplied by the number of years you would need to replace that income.

- The remaining balance on your mortgage is then added to that amount.

- Plus any additional debt and financial obligations, such as future college expenses, or even perhaps end-of-life arrangements.

- Then add what it would cost to replace services like childcare from a stay-at-home parent, wherever applicable.

Once you’ve added up all that, subtract from that total your liquid assets (savings accounts, college funds, or even other life insurance policies). Once complete, that number should be close to the amount of life insurance you need.

There are a few additional ways to estimate how much life insurance could be adequate, though these approaches tend not to be as thorough as the formula outlined above. Nevertheless, these approaches get you close, and when it comes to purchasing life insurance, an estimate is better than nothing.

- Annual income multiplied by 10. This approach won’t present a complete picture of your individual circumstances, but in broad strokes, it will give you some idea what your overall life insurance policy should be worth, especially if there are no children in the picture.

- Annual income multiplied by 10 + $100,000 per child for college. To account for college expenses for each of your children, multiply your yearly income by 10 and then add $100,000 in college expenses per child.

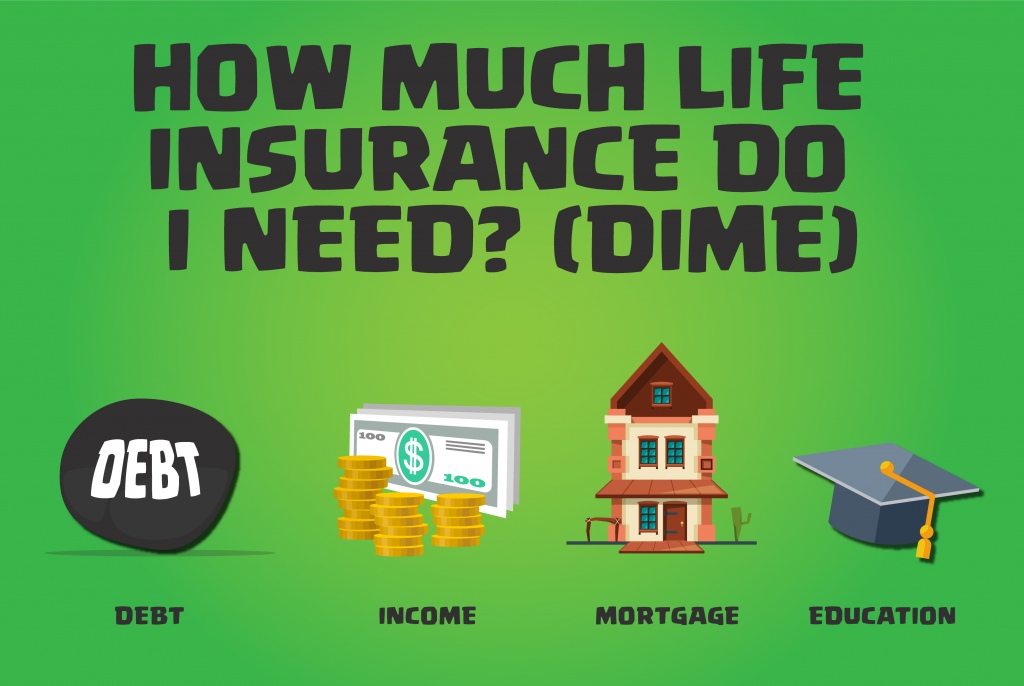

Perhaps the most accurate DIY approach to calculating how much life insurance to buy, however, is called the DIME method. We’ll explain more about that in our next section.

The DIME Method

Taking the closest look of all at your financial situation and how that scenario may change over time, the DIME method stands for: debt and final expenses, income, mortgage, and finally education. Add all that together and you’ll have a pretty good idea how much life insurance to buy. Here’s how it works:

- Debt, including any other kind of debt that might get passed on at the time of your passing, outside your mortgage. This number should also include funeral expenses or other kinds of end-of-life planning. This way, it won’t be left up to your loved ones to sort all that out in an already difficult time.

- Income, taking into account all forms of income, estimate how much money your family, colleagues, and even possibly your business partners would need to replace, and then multiply that number by how long they’d need the death benefit to fill in that gap.

- Mortgage, now add the remaining amount on any outstanding mortgage debt.

- Education. The final number to include in the DIME equation is an estimate of how much each child might need for education expenses, including tuition, room and board, and other possible expenses.

The total amount will be pretty close to the right amount of life insurance to buy, considering your financial situation and other unique life circumstances.

And with that, we’ve covered three of the most common ways to calculate how much life insurance you need, beyond meeting with a financial advisor or registered life insurance broker. If you do choose to meet in-person with a life insurance professional, keep in mind it’s often best to meet with a broker rather than insurance agent.

That way the broker will be working for you and you alone, seeking the best deal possible, rather than simply selling you a policy from the insurance company they work for. We’ll conclude with a few tips and tricks to fine-tune your life insurance policy.

Laddering Coverage

Why buy one life insurance policy, when you could buy two? Stay with us here, because by the time we’re finished explaining this really will make sense. Term life insurance policies cover specific periods of time, like until your children are grown and out of the house, just for one example. As your children grow and become independent, your life insurance needs will change, and in this instance, lessen — so why keep paying for a life insurance policy with your dependents included in the total amount of coverage?

For this reason, many recommend an approach called “laddering” your life insurance coverage. What this means is, rather than buying just one universal life insurance policy sufficient to cover you for the rest of your life, buy a series of term life policies, instead, planned to strategically expire as your life insurance needs change. This approach also works well if you expect your life insurance needs to increase, rather than decrease. Purchasing a policy while you’re young will always help you get the best deal possible. If you hope to have kids later, though, plan to ladder your coverage to account for kids when that time comes.

Remember, life insurance is just one part of the financial planning process

Life insurance is an important part of the financial planning process, but it is not the only part, nor is it best to view it as strictly an investment opportunity. To be sure, there are some kinds of life insurance with a cash value amount, growing over time, but it’s generally recommended not to treat life insurance as your only means to plan for the future. Instead, life insurance should be viewed instead as a means to protect your dependents, domestic partners, business partners, and maybe even employees when you die.

Don’t be cheap, and be open with your family

Last, and perhaps most importantly, purchasing a life insurance policy is not the time to be overly cost-conscious. This is an important part of the estate planning process, and you don’t want to leave anyone out in the cold when you die. Also, it’s surprisingly common for life insurance policies to be kept secret. Discussing death with friends and family is never pleasant, but it’s important for those closest to you to be well aware of your life insurance coverage before they really need it.

How To Know How Much Life Insurance To Buy: Conclusion

Purchasing life insurance is a big — but important — step. Nobody is as healthy as they are when they’re young, and for this reason, it’s best to buy a life insurance policy as soon as possible, which can equate to the best deal possible, but otherwise, how do you know how much life insurance to buy? And in this article, we outlined a few of the most common approaches.

First of all, life insurance calculators are common online, and they will help you come close to a final number. It’s also possible to meet with a financial advisor or qualified life insurance broker. We recommend working with a broker rather than an agent because this way, you’ll be sure to see the best deal the market has to offer, rather than just what that specific insurance company is trying to sell you.

Otherwise, here are a few common strategies to determine how much life insurance to buy:

- Add up your annual salary, the remaining balance on your mortgage, all additional debt or financial obligations, including college expenses. Then, subtract from that number your total assets.

- Simply multiplying your annual income by 10, or instead, if future college expenses are in the picture, multiplying your annual income by 10 and adding $100,000 in educational expenses per child.

- The DIME method: debt, income, mortgage, and education.

Following that, laddering life insurance is a common strategy for saving money on whatever amount of life insurance you settle upon. There’s a lot to keep in mind when shopping for your very first life insurance policy. Including, but not limited to, what kind of life insurance to buy, but also how much that policy should be worth. We hope this simple guide helped you get started. For more information consult Expensivity’s Complete Guide to Life Insurance.