Purchasing a life insurance policy is a big decision. And like any big decision, it’s best to break down that decision-making process into small chunks. When taken individually, these small parts will add up to the best choice for you and your individual circumstances.

In this article, we’ll lay the framework for answering two of the most commonly asked questions for people just beginning to research life insurance: who should buy life insurance, and which kind is best?

Answering these two questions to the best of our ability will help you purchase the best life insurance policy for you, and for your loved ones.

We’ll begin with who should buy life insurance? If any of this sounds like where you are at in life, purchasing life insurance is a good decision.

Who Should Buy Life Insurance

The most straightforward answer to the question of who should buy life insurance is: Anyone who has reached a point in their life when someone else relies on their income, whether that’s a child, a spouse, a significant other, or simply a business partner. There’s a bit more to know than that, which we’ll cover later on.

But first, there are a few different types of life insurance: term life insurance, or whole life insurance, sometimes called permanent or universal.

Now that we’ve discussed who should buy life insurance, here are some tips and pointers to figure out which type of life insurance is best for wherever you are in life.

Who is Term Life Insurance Best For: Young, Single Adults on a Budget

Typically, the more affordable of the two different types of life insurance is a term life policy, covering an individual for a specific period of time, for 10 or 20 years, for example, or just until a child has reached the age of 18.

For this reason, term life insurance is best for a young, single person without many financial obligations outside perhaps a young child or a business partnership, or who has entered into a loan agreement with a cosigner, such as a student loan.

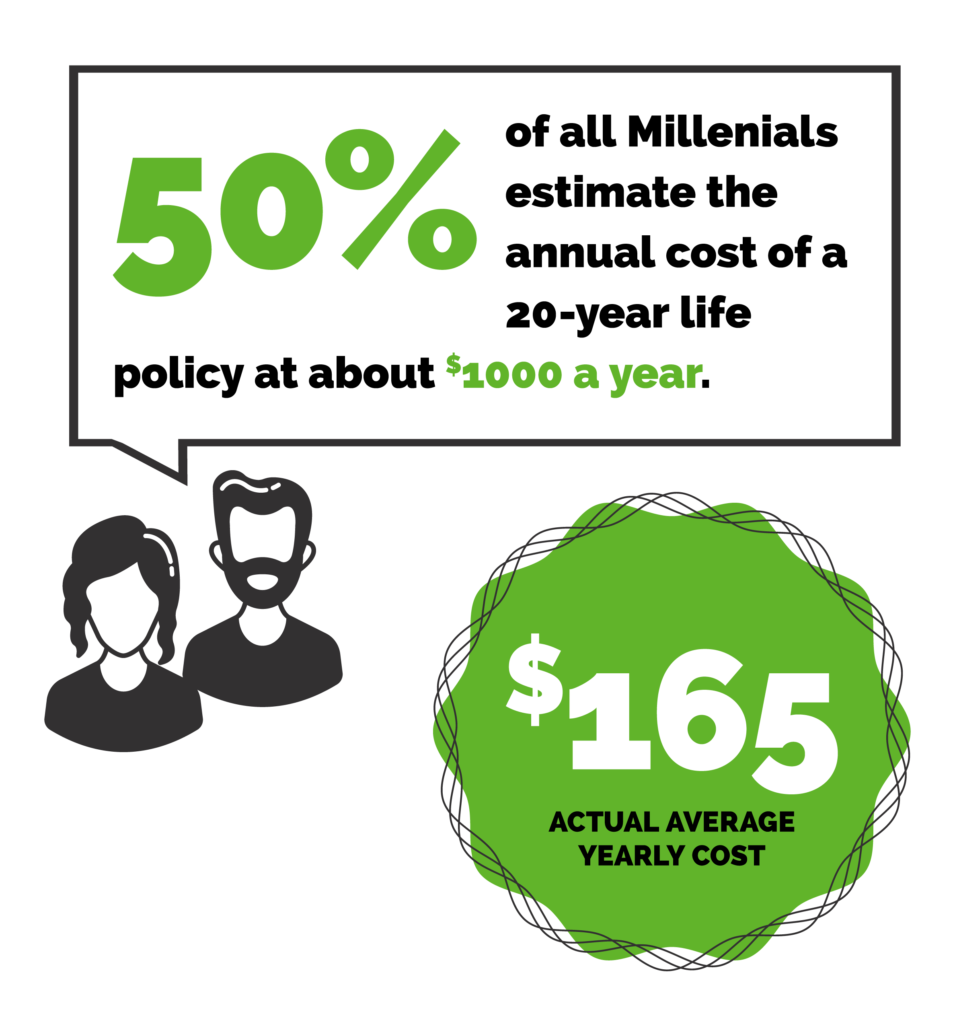

And it’s cheaper than you think! According to LIMRA, the Life Insurance Marketing and Research Association, nearly half of all Millennials estimate the annual cost of a 20-year term life policy at about $1K a year, when in reality, it’s closer to $165. That’s pretty affordable.

Should you pass away during this period, or term, then the life insurance policy could cover funeral expenses or any remaining balance on a loan on which you are a cosigner.

Term life insurance policies have no cash value, so when the term for which you’ve purchased elapses then that money will be gone, and even though purchasing any type of life insurance when you’re young will be more affordable than it might be otherwise, term life policy premiums do become more expensive over time.

Who is Universal Life Insurance Good For: Younf Families or Business Owners/ Partners

The next kind of life insurance goes by a few different names: universal life, permanent life, or whole life insurance, or sometimes simply “cash value insurance.”

This kind of life insurance is more expensive than term life coverage, but it also typically has a cash value that increases over time and that can be drawn upon or borrowed against for a variety of reasons, including an emergency, but also possibly home renovations or to supplement the cash position in a business for which you are a partner or have an ownership stake.

And of course, whole life insurance will be with you for exactly that amount of time: your whole life — so long as you pay the premiums and keep the policy current.

As well as term and whole life insurance policies, there are a few additional, and perhaps less well-known types of life insurance to consider. Each offers its set of pros and cons. We’ll go over those now.

Guaranteed Life Insurance: Best for Older Adults

Guaranteed life insurance is designed specifically for older adults who’ve reached retirement age, and whose children have long since started families of their own.

Why buy life insurance at all at this late stage in life? Guaranteed insurance is good for funeral expenses. What guaranteed life insurance means is you’ll be offered a policy regardless of age, medical history, and sometimes without a medical exam.

For these reasons, guaranteed life insurance is expensive.

For more information about guaranteed life insurance, or for help deciding if guaranteed life insurance is right for you, consult a trusted financial advisor.

Variable Life Insurance: Best for Adults with Long-Term, Tax-Deferred Investment Objectives

Variable life insurance is a lot like universal life insurance, and policies of this type can often be combined with universal policies. In a word, variable life insurance is just that: variable. It offers a death benefit, but that death benefit varies depending on the performance of what is contributed over time in terms of interest rates, investment performance, and other factors.

Variable life insurance carries some risks.

Since your contributions to a life insurance policy are tied more closely to the market than is the case with other kinds of coverage, there’s the potential for better growth, but there’s also the potential for loss.

For this reason, variable life insurance should not be used for short-term savings objectives but can be useful for long-term investment goals. Best of all, all contributions are tax-deferred.

Like any life insurance policy, though, it’s best to do your research and carefully consider your options before purchasing a variable life insurance policy.

With a basic understanding of the different kinds of life insurance policies, with some understanding of which kind is best for different stages and different potential life scenarios, let’s now conclude with a closer look at who should buy a life insurance policy.

If any of the following sounds like where you are in life, it could be time to purchase a life insurance policy.

Who Needs Life Insurance

Purchasing life insurance is a big decision. To help you make your choice, consider the following. If you check any of these boxes, you should consider buying a life insurance policy.

- Anyone with children or dependents. If anyone depends on your income and would be negatively impacted by your passing and subsequent loss of income, it’s time to protect your loved ones with the best life insurance policy.

- Business owners and business partners. If you own a business, or if you’re in business with partners, it’s also time to consider life insurance.

First off, the death benefit associated with a life insurance policy could help your family and partners settle business issues, pay off debt, finance selling the business, or simply keep the business up and running in the event of your passing.

Additionally, though, the value of a whole life insurance policy can also be borrowed against to improve cash flow should the need ever arise. If you’re in business with partners, or if you’re a partner in a business it’s also a good idea for the partners involved to carry life insurance policies. And offering life insurance is also a great benefit to offer your employees.

- Anyone with a lot of debt. If you carry a lot of debt for whatever reason, or if you have a cosigner or if you are a cosigner on a loan, picking up a life insurance policy is highly recommended. Many forms of debt are immune to creditors should you happen to die before the balance is paid off, but not all.

If you have or if you are a cosigner on a loan, your passing would mean paying off the remainder of what’s owed will become the sole responsibility of the other person carrying the loan. The last thing you want is for your remaining debt to become the responsibility of your heirs, or for your estate to be decimated by creditors, or locked up in probate. The death benefit associated with a life insurance policy will help settle what’s owed.

- Anyone concerned about burial expenses. In 2021, the average cost of a funeral is estimated to be anywhere from $9,500 to $12,500, depending on where you live, among other factors. Some life insurance companies even offer a specific type of coverage for funeral expenses called final expense insurance, with a death benefit intended specifically to cover the cost of burial or cremation.

Who should buy life insurance and which kind is best: Conclusion

There are two basic types of life insurance: term life, or whole life, as well as guaranteed life insurance, which is less common. There are some further particulars that can be adjusted within these kinds of life insurance policies to best suit the needs of the individual carrying the policy.

What’s important to note is that each type of life insurance has advantages and disadvantages, and which kind is best depends on where you are in life. Term life is likely best suited for a young adult without children or dependents, while whole life coverage is a better option for families or anyone with dependents.

It’s also the best choice for business owners, business partners, or anyone carrying a significant amount of debt. Some consumers do take out term life insurance just until their children are out of the house, or until the terms of a loan have elapsed and the balance has been paid in full, however.

For additional information about the best life insurance policies and which kind of policy might be best for you and your loved ones and trusted associates, consult a financial advisor, or see Expensivity’s Complete Guide to Life Insurance.