There are a number of things to think about and to prepare for as we age: finishing college, managing debt, securing adequate housing, and working somewhere fulfilling and saving for the future, to name just a few.

And maybe for you, that list includes finding love and starting a family — even if that family is you and a furry four-legged fur baby.

Considering all that, what are the reasons you should get life insurance? You’re still young after all. Won’t you have time for that later?

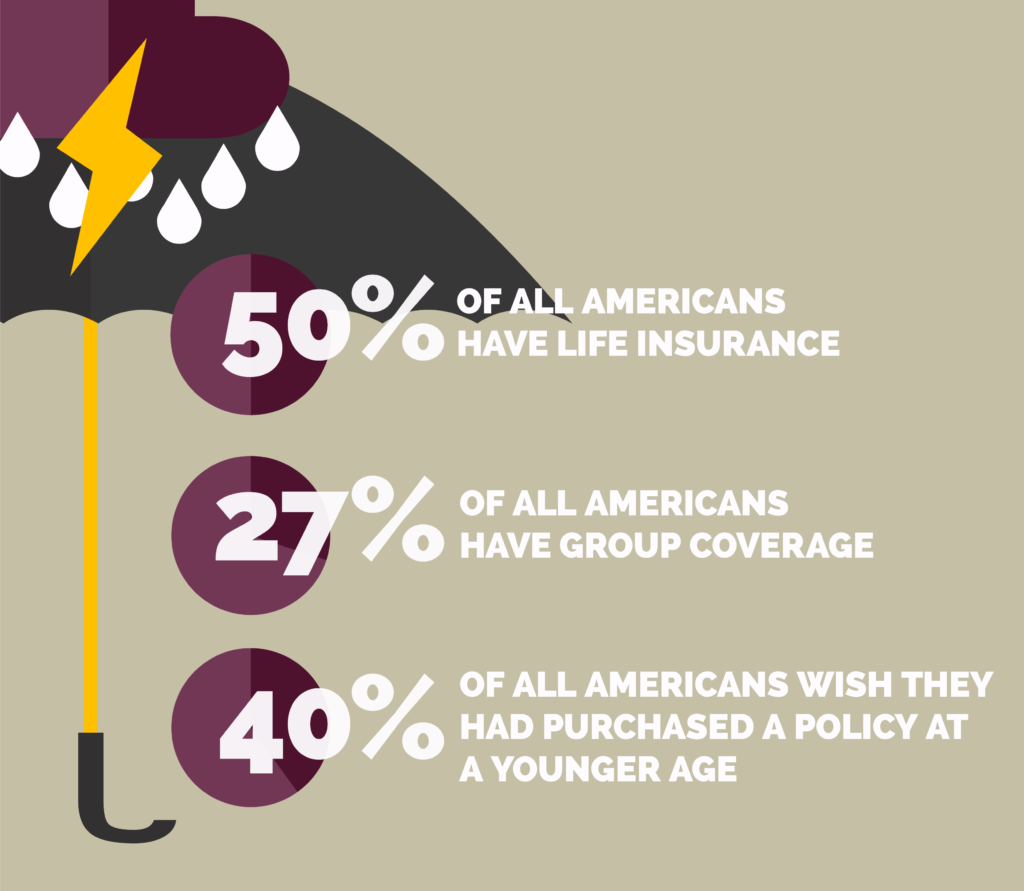

The fact of the matter is, there are many very good reasons to buy life insurance no matter where you are in life. And even though roughly half of all Americans have life insurance, according to recent estimates, 27% have only group coverage. Those types of policies are rarely adequate. And following that number, 40% wish they’d purchased a policy at a much younger age.

When it comes to life insurance, one thing’s for certain: the sooner you buy a policy, the more affordable and effective it will be.

In this article, we present 5 reasons you should get life insurance. The younger you buy a policy, the better. Trust us when we say that life insurance is less expensive than you think and more useful than you imagine.

5 Reasons You Should Get Life Insurance

1. Don’t Leave Your Debt Behind

It could be said that debt, to some degree, is a fact of life. But should you pass away — unexpectedly or otherwise — did you know some of your debt could become the responsibility of those left behind?

That includes any possible heirs, but also business partners, family members, and husbands and wives. Don’t let that happen to you!

According to the Federal Reserve, in fact, average household debt in America reached a staggering $14.6 trillion in 2021, and recent surveys show that most Americans are likely to die with some form of outstanding debt — as much as $60K on average, based on recent surveys.

Those forms of debt include student loans, business loans, mortgages, and credit card debt, among many others!

RELATED: What Do Americans Spend the Most Money On?

Furthermore, both young and old alike expect to leave some debt unpaid at the time of their passing. Not all debt is passed on when you die, it’s important to note. But if you have co-signers on a loan (student or otherwise), a mortgage or credit card debt, or if you’re in business with a partner, then any outstanding debt will be passed on to them at the end of your life.

What’s more, the “death benefit” of a term life insurance policy can be used however a beneficiary would like to use it, including paying off debt. For this reason, most term life policies are taken out for the life of a loan, and most often a mortgage.

Having a life insurance policy with a single beneficiary will also protect your assets from reverting to an estate, potentially locking it up in probate where creditors can get at it.

For these reasons and more, if you’re carrying debt, and you expect it will remain outstanding at the time you die, it’s important to take out a life insurance policy to protect your asset from creditors.

This will leave a little something behind for loved ones, business partners, or for whomever you’ve named as a beneficiary.

2. To Plan for the Future

Your passing could put undue hardship on anyone in your life who depends on your income, including your family members, but also business partners and employees.

The death benefit associated with life insurance policies will fill that income gap, covering average living expenses and a whole lot more until your family, friends, and colleagues can get themselves back up on their feet.

Another little thought-of benefit of life insurance relates to college tuition.

Parents of one or more children who plan to attend college — a crucially important step to secure good-paying jobs of the future — may not realize that life insurance policy payouts can be used to cover college tuition, which reached nearly $44K per year on average, according to recent data from the U.S. News & World Report.

Life insurance policies can also sometimes be used to cover long-term care expenses for dependents with special needs. And another less well-known benefit of life insurance is to help pay for your own retirement.

No, you won’t need the money if you’re dead, but many life insurance policies have what’s called a cash value, which can be drawn upon to supplement income when retirement age is reached, or if long-term care is required.

3. Business Planning and Estate Taxes

As previously mentioned, if you’re in business with a partner or partners, it’s particularly important — for all of you! — to carry life insurance policies, and most typically a whole life policy.

This way, should one of you die all the potential loose-ends associated with the business will be tied up. But that’s not all.

Here are some additional reasons small business owners should have a life insurance policy:

- Whole life policies earn cash value. Whole life policies gain value through interest and pay dividends over time. This becomes useful to businesses in any number of ways, and can even boost a business’s cash flow when used strategically.

- Whole life policies attract quality employees. Instead of a 401k plan, some business owners attract and retain quality employees by offering whole life insurance policies.

Policies of this sort behave similarly to a retirement account over time, and business owners even gain some tax benefit for paying the premiums on those policies.

Speaking of taxes, life insurance also helps cover the cost of estate taxes. Estate or inheritance taxes are paid by your heirs on whatever the total amount they receive happens to be at the time of your passing, and that can be a lot. Let the best life insurance policy help cover the cost!

4. You Want to Get Married and Start a Family

Professional goals and business concerns aside, purchasing life insurance is crucially important for anyone who is interested in getting married and starting a family. Here’s why:

- Joint life insurance policies help already successful couples enter into a marriage secure that the burden of estate and inheritance taxes will be lessened for their beneficiaries. In some circumstances, individual life insurance policies may be a better fit for a couple, rather than a joint life insurance policy. Consult a financial advisor, accountant or estate planner to explore which option is best for you.

- Life insurance protects children. And that’s true whether you’re planning to have a child sometime in the future, or if children are brought into a marriage from a previous relationship. When a child is the beneficiary of a life insurance policy, establishing a trust will preserve those assets while they’re still a minor.

On the topic of families, life insurance can also help pay the costs of long-term care for aging parents, a dilemma more and more young people are faced with as the Baby Boomer generation ages.

According to recent data from the AARP, in fact, more than 6 million millennials are caring for aging relatives, and that number is only expected to grow.

In instances like these, life insurance with a long-term care rider helps pay for the expense.

5. You Like to Take Risks or You Have a Risky Job

The last but certainly not least reason to buy life insurance is if you have dangerous hobbies, or if your job puts you at high risk of injury or even death. If you’re employed in a risky line of work — mining, aviation, firefighting, or construction, to name a few — you may already be covered by an employer-provided life insurance policy, but if you switch jobs, retire or leave that employer for whatever reason, that policy will lapse.

For this reason, it’s important for anyone employed in a high-risk environment to carry life — and even possibly disability — insurance on their own.

And what about risky hobbies when you’re not at work?

Is your idea of a good time jumping out of an airplane, kayaking on a rough and remote body of water, or rocking climbing? If thrill-seeking is how you unwind, then it’s also important to have life insurance to protect your family, business partners and employees should something go wrong.

Some insurance companies charge higher premiums to individual policyholders with risky pastimes. For this reason, it’s particularly important for adventurous policy-holders to shop around before settling on a life insurance provider, or to first consult with an advisor before making their decision.

5 Reasons You Should Get Life Insurance

These, after all, are only five reasons to purchase life insurance. The list could go on. If we’ve convinced you to take the plunge and purchase a policy, then great! Our job here is done.

But if you need more information, that’s ok, too. Something as important as life insurance should never be purchased without first gathering the data you need to make an informed choice. Check out Expensivity’s Complete Guide to Life Insurance for more information.

Most importantly — and even though the end of your life is never a fun subject to consider — it’s never too soon to start planning for the end. Purchasing a life insurance policy while you’re young can save money, improve results, and give you the peace of mind necessary to enjoy the time do you have with friends and family.