Congratulations! You’ve decided to pop the question to your significant other. Maybe you’re planning a wedding or some kind of commitment ceremony that suits your values. Either way, engagement rings cost a lot. Here is the ultimate list of the best credit card to buy an engagement ring.

Best Credit Card to Buy an Engagement Ring in 2023

The right credit card will help you buy the ring you’ve always wanted and perfectly represent your love and commitment. Furthermore, with the best cash-back rewards, points earned on the purchase can go toward gas, travel, and dining during or after the ceremony — or even perhaps cut the cost of building or renovating your forever home.

This guide presents the three best credit cards to buy the ring that best represents your love. Even with an annual fee, let the best credit cards for purchasing a ring help make the wedding jewelry purchases of your dreams come true.

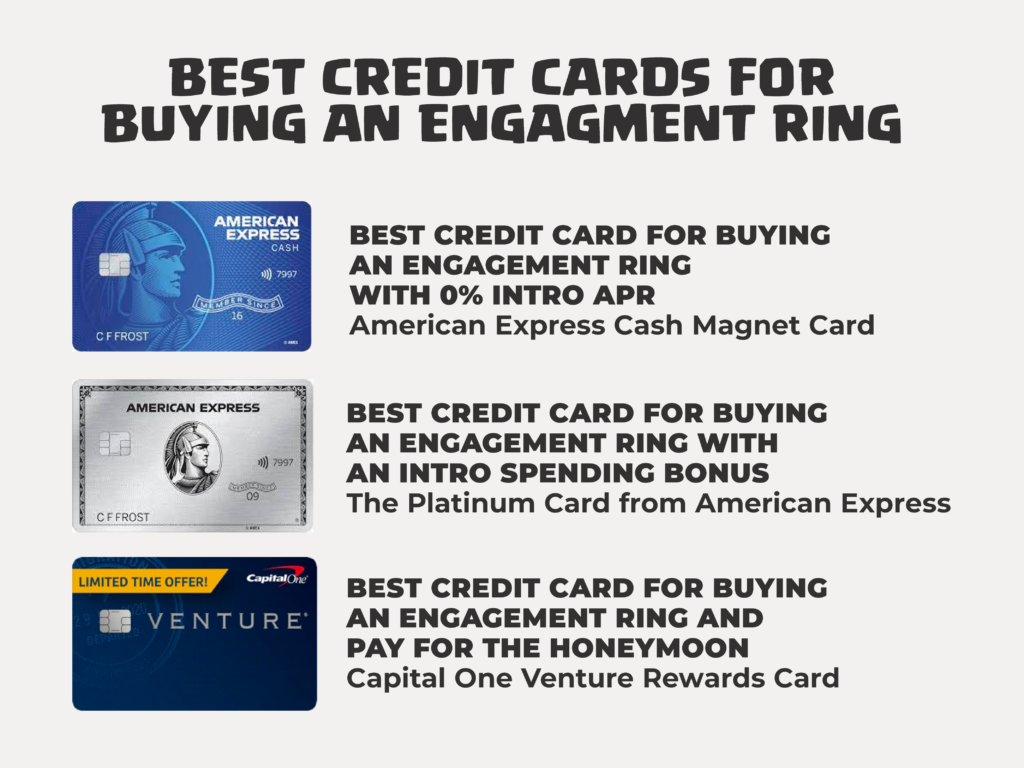

Best Credit Card for Buying an Engagement Ring With 0% Intro APR: American Express Cash Magnet Card

The best reason to buy the diamond ring representing your commitment is to take advantage of the 0% APR introductory period, cash-back rewards, and a high credit limit. The best American Express Cash Magnet Card for the 0% intro APR with no annual fee is, without a doubt, the Cash Magnet card from Amex.

All information about the American Express Cash MagnetSM Card has been collected independently by Expensivity.com.

Use the Cash Magnet card and get no interest for the first 15 months from account opening. Aside from having no annual fee, this credit card issuer can turn a roughly $5,000 ring purchase into $400 monthly installments.

As well as the generous introductory period, we like how the Cash Magnet card shows up strong with 1.5% cash-back rewards as a statement credit on all purchases, with no categories to track. After all, you have enough to worry about when planning a wedding, don’t you?

Make other purchases and get cash-back with the card related to the wedding ceremony, and these points could go a long way toward funding the honeymoon. For example, how else could you get as much as $80 cash-back rewards on the average $5,000 ring?

Pros

- Other points concerning the Cash Magnet card include the $150 statement bonus after the first $1,000 spent on the card within the first three months after account opening and no annual fee.

- And when making a purchase as large as a ring, you want protection. With AMEX, enjoy $1,000 in incident protection if the ring is damaged, lost, or stolen within 90 days of purchasing.

- There’s also zero fraud liability, so your security is never in doubt.

Best Credit Card for Buying an Engagement Ring with an Intro Spending Bonus: The Platinum Card from American Express

To get the most bang for your buck regarding an introductory spending bonus within the first few months of your account opening, consider the next card in our ranking: The Platinum Card from American Express. With the Amex Platinum, earn an impressive 75,000 points after spending $5,000 in the first six months of card membership and 1x cash-back rewards on all purchases in a jewelry store.

Compared to a Citi Double Cash Card, using the Amex CardMatch for more targeted spending means getting offers as high as 125,000 Membership Rewards (some exclusions apply). Despite offering purchase protection like Chase, an annual fee on the Platinum card will run you upwards of $550.

Despite having an annual fee, Amex membership cash-back reward points are among the most valuable in the game and especially useful for those planning a wedding or a honeymoon. For example, these points transfer to 16 hotel and airline partners, ideal for planning your honeymoon, with many opportunities to upgrade the experience.

Those bennies include airline fee credits, elite status at all sorts of hotels, and even airport lounge access. And if heaven forbid, your flight is delayed for more than six hours, Amex Platinum covers up to $500 related to the delay and even offers $200 in Uber credits once you arrive.

Pros

- Annual fees on the Platinum card will run you upwards of $550, though. But don’t miss the $200 yearly airline fee credit, covering additional luggage costs and other incidentals, making your honeymoon flight as comfortable as possible.

- The Platinum Card is also the best choice for purchase protection and cash-back, reimbursing up to $10,000 with a maximum of $50,000 annually on other purchases within the first 90 days should the ring be lost or damaged.

- The card is undoubtedly one of the credit cards to buy an engagement ring and pay for the ceremony of your dreams.

Best Credit Card for Buying an Engagement Ring and Pay for the Honeymoon: Capital One Venture Rewards Credit Card

You bought the ring and popped the question. What’s next? It turns out that’s just the beginning of the wedding planning process. When planning the honeymoon, specifically, the Capital One Venture Rewards Credit Card can help with purchase protection despite having annual fees.

Leading off the list of things making this the best card to buy the ring, earn rewards, and pay for the honeymoon (or other parts of the ceremony) on points is the very generous 100K in bonus miles offered on the first $20,000 spent on the card in the first year after opening the account.

Other things we liked about this travel rewards credit card include unlimited 2X miles on every purchase, every day, with no foreign transaction fees. Even if you have to pay an annual fee, there’s also no pressure to redeem them because the miles won’t expire for the life of the account opening.

A long engagement is in store, or if you have a big wedding to plan, this cash-back card is even more reason for you. If a wedding price tag like that isn’t your style, the card with reward programs still offers 50,000 miles on the first $3,000 spent in the first three months of card membership, so there’s something for everyone.

Pros

- Regular APR on the card ranges between 17.24% and 24.49% within a certain amount of time from the account opening, which is on par with most credit cards, and there is a $95 annual fee.

- Offers features like the $100 application fee for Global Entry or TSA PreCheck.

- It allows you to transfer those miles to more than 15 travel loyalty programs with no foreign transaction fee.

Should I Buy an Engagement Ring With a Credit Card?

Again, it’s never a good idea to charge any purchase — including an engagement ring — you can’t afford without a solid plan to pay back the debt and annual fee.

With careful budgeting and strategic selection of the right credit card offering the best perks, many sensible reasons exist to put the ring on plastic.

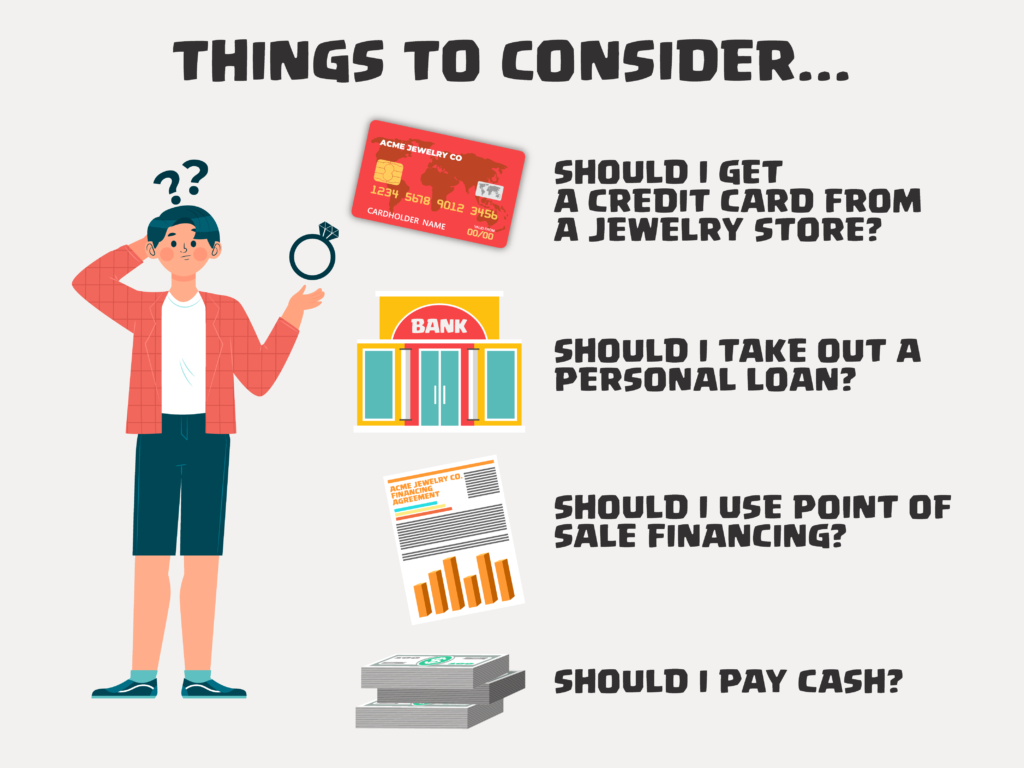

Should I Get Credit Cards From a Jewelry Store?

Like many retailers, jewelers offer such credit cards of their own. However, people should determine the suitability of credit cards considering their own individual financial position.

- Merchant-specific credit cards like these are less likely to offer 0% intro APR financing or the flexibility to redeem points earned by purchasing travel and credit cards.

- The minimum credit score requirements are likely much stricter than the major credit card companies.

- Choose a cash-back credit card with a credit limit much higher than the ring’s price.

- Avoid getting cards with foreign transaction fees and a high annual fee.

Should I Take Out a Personal Loan?

Another way to pay for the ring is a personal loan. The interest rate will likely be much lower than those offered through a credit card issuer (much higher than a 0% APR intro offer on balance transfers in bonus categories, so there are tradeoffs).

For example, personal interest rates are currently hovering around 10%, according to the Federal Reserve, while average credit card interest rates are more like 16% on the low end! You should also check for purchase protection benefits covering theft or damages to eligible items and foreign transaction fees.

Should I Use Point-of-Sale Financing?

Increasingly offered across a broad range of retailers, point-of-sale financing is appealing for many reasons, including the freedom to pay back the money in installments. Many point-of-sale financing services boast 0% interest intro periods, just like a credit card company with cash-back.

Should I Pay in Cash?

Spend the cash (or save up the money) and use such credit cards and enjoy the best of both worlds:

- Make a responsible financial decision and enjoy the benefits of repayment.

- Enjoy a no-interest introductory period or waived annual fee.

- Put some cash-back in your pocket.

For this reason, a combination of money in the bank and a strategic credit card purchase with a solid plan to repay the debt is the best way to buy a ring. Sometimes, you can redeem this cash-back as a statement credit or direct deposit.

How Much Should I Spend on a Ring?

Beautiful engagement rings are available for as little as $1,000, or much more than $20,000, depending on your tastes. Here are some points to consider when budgeting for your jewelry purchases to get a cash-back.

The Two Months Salary Rule: Debunked

Popularized by De Beers, the two months salary rule says your ring should cost two months. If the average American wage is about $80,000 annually in 2021, you should spend about $14,000 on your ring.

That’s nearly three times the average cost of a wedding ring. We discourage using the two-monthly salary rule because it sets up some unreasonable expectations about how much a wedding ring should cost: expectations padding the jeweler’s bottom line instead of the big event’s planning budget.

The Diamond Approach

Some say the cost of a ring is reflected by the size, type, and carats of the diamond, and if you want to pay less, you should downgrade the diamond.

This may seem sensible at first because diamond prices can vary widely depending on several factors, directly affecting the overall cost of the ring. The thing to be careful about using this approach is that when it comes to diamonds, you get what you pay for.

Just be sure your thriftiness won’t result in dissatisfaction with the overall presentation of the ring sometime down the line.

The Rule of Averages

Most experts agree that a ring will cost you somewhere in the range of $5K to $6K, regardless of your income and regardless of the size, type, and quality of the diamond.

Bearing this average in mind when you begin the ring-shopping experience will help ensure you don’t overpay for the ring. However, you also get a ring that you and your partner will be truly satisfied with for eternity.

Conclusion

Ring or not, it’s never a good idea to purchase something on a credit card you can’t afford or without a plan to pay off the debt or annual fee in a timely manner.

Planning carefully, though, while saving some cash and buying the ring with the right credit card with cash-back can pay dividends down the line: on the ceremony, for the honeymoon, and your life beyond.