You’ve decided it’s time to take the plunge and buy some life insurance. No matter what point you’re at in life, it really is the responsible decision. Even so, there’s no reason to pay any more than you have to for that life insurance coverage. Are highly monthly premiums a foregone conclusion? We’re here to say, there are more ways to save on life insurance than you might at first expect.

In other words, like anything, life insurance costs money, but not as much as you might guess, at least according to the 2021 Life Insurance Barometer Study from LIMRA, or the Life Insurance Marketing Research Association. What LIMRA found was that life insurance is much less expensive than what most consumers estimate.

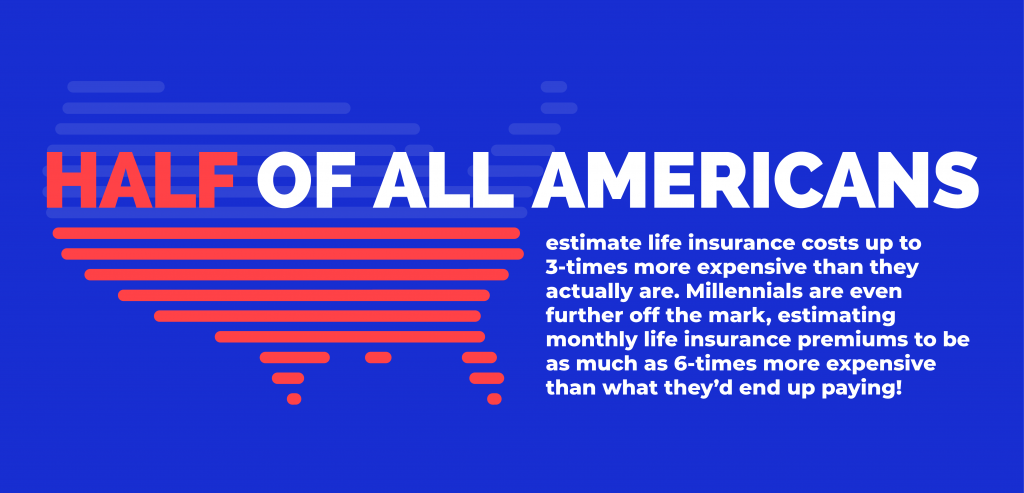

Half of all Americans, in fact, estimate life insurance costs up to 3-times more expensive than they actually are. Millennials are even further off the mark, estimating monthly life insurance premiums to be as much as 6-times more expensive than what they’d end up paying!

So how much does life insurance cost? Well, that depends. What’s for certain, though, is that if you follow any or all of these five tricks for getting cheaper life insurance, you’ll save money on your monthly premiums. You’ll also enjoy the peace of mind that comes along with the protection the best life insurance policies offer you and your loved ones.

5 Tricks For Getting Cheaper Life Insurance

Don’t sign-up for life insurance without first reading our list of tips and tricks to get a better deal.

1. Choose a Convertible Term Life Policy

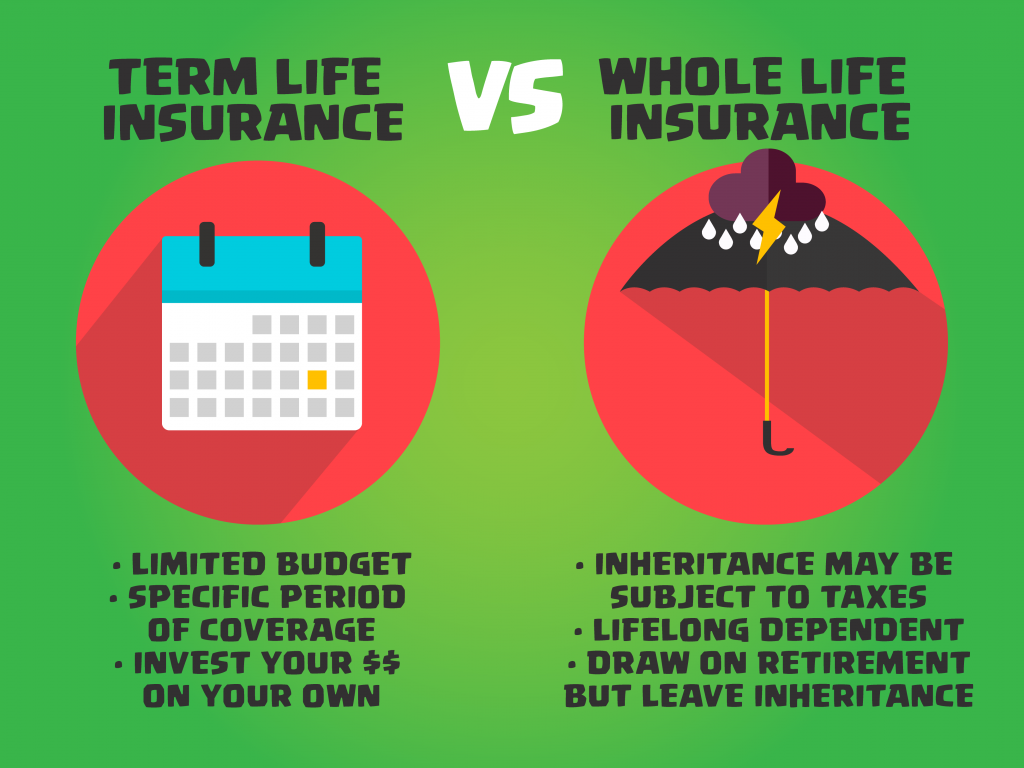

There are primarily two types of life insurance:

- Term life, covering you for a specific period of time.

- Universal life, also sometimes called whole life or permanent life insurance.

Term life policies last for a specific amount of time, perhaps until your children are grown and out of the house. For this reason, these kinds of policies are cheaper than whole life policies. Although premiums are more expensive, cash-value life insurance, on the other hand, does offer some investment incentive, growing in value over time.

According to recent estimates, an otherwise healthy 35-year-old man could pay only about $430 a year for a term life policy, while that same person could pay as much as $4,400 a year for $500,000 in whole life coverage, all other things being equal. That’s a big difference!

So which one do you choose? If you’re young and relatively healthy, you will save money choosing a simple term life insurance policy. Here’s the thing, though, some, but not all, term life policies can be converted to whole life coverage, once the term for which policy has been purchased has elapsed.

This way, young people in the prime of life can pay less for term life coverage up front, while also enjoying the cash-value benefits of a whole life policy as their income improves.

2. Buy Life Insurance While You’re Young

Although making end-of-life arrangements is not what most young people consider a good time, the fact of the matter is: One of the best ways to save money on your life insurance policy is to buy one while you’re young. Here’s why:

- You’ll never be healthier than you are right now, and purchasing coverage before preexisting conditions can develop will also help drive down your monthly costs.

Your life insurance rates aren’t just based on your age, either. Some other factors considered when settling on a monthly life insurance premium include:

- Where you live

- Your gender

And even what you do for a living.

BONUS TIP: Think just because you’re a smoker that means you’ll pay more for life insurance? While that’s sometimes the case, a smoking habit does not automatically equal higher monthly premiums. Some policies are designed specifically for smokers. It’s also never too late to quit or to take steps to prove to your life insurance provider that you can now be considered a nonsmoker, potentially lowering your premiums.

Smoker or not, what’s unquestionably true is the younger you buy life insurance the better, with typical premiums increasing anywhere from 8% to 10% each year you age, according to some estimates.

3. Ladder Your Coverage

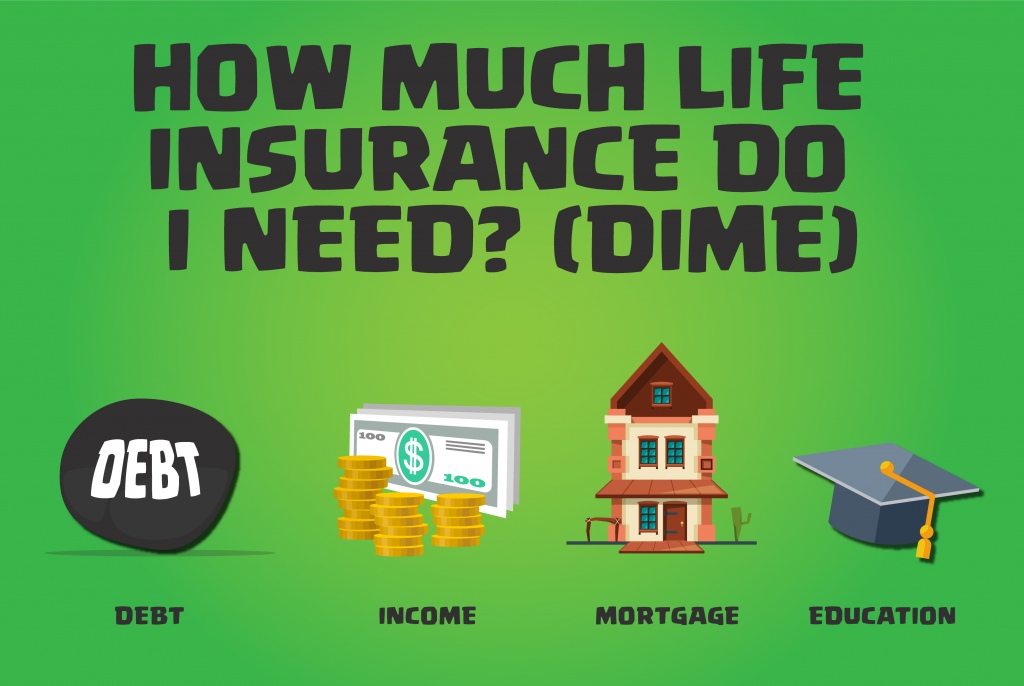

Settling on how much life insurance you need is the first and maybe most important step in buying a life insurance policy. There are a number of different strategies to reach an appropriate dollar amount for your policy:

- The DIME method.

- A life insurance calculator.

- Purchasing a policy equal to 6 to 10-times your annual income.

- Consulting with a life insurance agent or financial advisor.

It’s crucially important to buy the right amount of life insurance, but the more you buy, the more expensive your monthly premiums will be

What happens, though, when your debt and obligations change? Is there a way to keep your life insurance policy, and monthly premiums, finely tuned to whatever point you are at in life? There is, and it’s called laddering.

Look at it this way: life insurance needs typically tend to actually decrease over time: Children grow and become independent, debt gets paid off, and so on, all while our income increases.

Laddering means rather than buying one policy adequate for the rest of your life, planning to purchase a series of term life policies sufficient enough to cover specific periods of time: just until your children leave for college for example, or over the terms of a specific loan. That way your life insurance stays flexible as your needs change, reflected in the monthly premiums you pay.

4. Cut Unnecessary Riders and Avoid Simplified Life Insurance

This next trick for getting cheaper life insurance is really a 2-step process that could best be summed up as: read the fine print. Which is important to do, anyway, before entering into any kind of contractual obligation.

Riders are specific accommodations made in a life insurance policy, and one of the most common is for smokers. Some life insurance companies offer special deals to attract people who smoke, helping their life insurance be somewhat more affordable than their life insurance would otherwise be. Other types of riders include accidental death, for individuals who have risky professions or hobbies, and long-term care, among others.

Crucially, and although riders can be useful to customize a policy as much as possible to your specific circumstances, it’s important to keep track of these riders as time goes on — for example, maybe you quit smoking — why keep paying for the rider? It’s also important to make sure you aren’t paying for any riders you don’t need right off the bat, so you’re not paying for something in your policy you don’t really need.

Furthermore, a medical exam is commonly required when buying life insurance, although these days some policies are available with no doctor’s appointment necessary. These are sometimes called simplified life insurance policies. What’s important to note about policies of this type is that even though they are perhaps easier and more convenient than having to visit the doctor, they are often more expensive than they might otherwise be.

That’s because the insurance company is assuming some risk, also called underwriting, covering individuals without first checking to see what kind of physical condition they are in, or if they have any preexisting conditions. This type of coverage can cost as much as 2-times more than policies requiring a doctor’s appointment, proving that nothing comes for free — including simplified life insurance policies.

BONUS TIP: None of this is to say that affordable such as Bestow, Ladder, and Haven Life. offering quick life insurance policies online without a doctor’s appointment. This new breed of company uses modern technology to check relevant health records to sell underwritten policies that are different from simplified life insurance. If you’re young and otherwise healthy, there’s no reason not to go this route.

5. Shop Around

The final, and perhaps most important trick for getting cheaper life insurance is to shop around, rather than simply accepting the first policy offered from the first company you approach. Be sure to check the viability of the company through services like A.M. Best or the Standard & Poors. It is possible to do this all on your own, but if that proves too much or too difficult, consult with a local independent insurance broker, who works for you — the consumer — rather than a specific insurance company. This way you’ll receive a fair and balanced appraisal of the offer, with a licensed professional helping you find coverage that suits your needs and fits your budget.

5 Tricks For Getting Cheaper Life Insurance: Conclusion

Buying life insurance is a big — and sometimes expensive — proposition. If you’re young and healthy, there’s no time like the present to buy a policy. All that being said, there’s no reason to accept the first high-priced life insurance policy you’re offered. In this article, we present five tricks for getting cheaper life insurance.

- Choose a convertible term life policy

- Buy life insurance while you’re young

- Ladder your coverage

- Cut Unnecessary Riders and Avoid Simplified Life Insurance

- Shop Around

Shop carefully, take your time, and work closely with an independent insurance broker that works for you, not for a specific insurance company. That way you’ll get a fair and balanced opinion about what policy suits you best. For more information about life insurance, and to pick the best life insurance policy for your individual circumstances, no matter what stage of life you are in, consult Expensivity’s Complete Guide to Life Insurance.