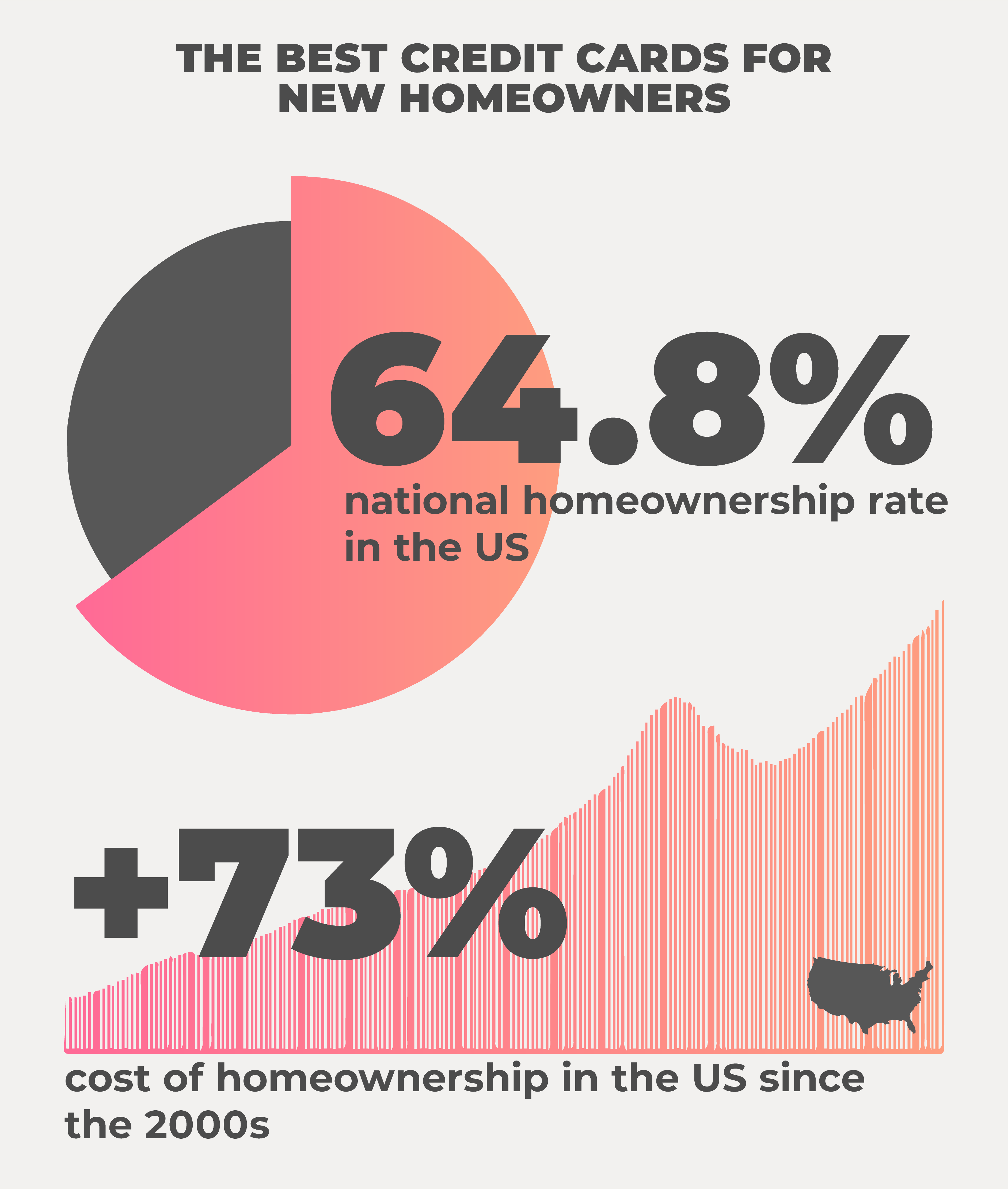

Congratulations! You’re a new homeowner. But with the cost of homeownership up around 73% over the past few decades, the expense of purchasing a house has likely left you feeling a little strapped. That’s especially true because the expenses don’t stop once you purchase your property.

The average monthly cost of owning a home is about $800, considering mortgage interest, taxes, maintenance, repairs, and other expenses. Why not let the best credit cards for new homeowners take a little of that burden off your shoulders?

But wait, you might be asking; I just went into debt to buy a house: Do I really want more debt on a card?

If you’ve yet to secure a home loan, the answer to that question is a resounding, “no.” You don’t want that hard credit check from an application showing up on your credit score!

But if your home app is complete, or if you’re already living in your new house, we’re here to say the right card can be a useful — and financially responsible tool — for a brand-new homeowner, just like you.

In this article, we’ll tell you what you need to know about the best credit cards for homeowners, presenting what we liked, and a few things we thought you should be aware of about each card we reviewed.

Top Credit Cards for Homeowners Reviews

From the best overall, to the best for new furnishings, and the best choice for fixer-uppers, here are our top three picks for the best cards for homeowners:

- The Best Overall Credit Card for New Homeowners: Chase Freedom Unlimited

- The Best Credit Card for New Homeowners, Furnishing and Decor: U.S. Bank Cash+ Visa Signature Card

- Best Credit Card for New Homeowners, Home Repair, Remodeling, and Updates: Discover it Cash Back Card

Remember: Never put your mortgage payment on a card. It’s never worth it.

But from 0% APR introductory offers to great bonus rewards on what new homeowners need the most, a complete look at what made these cards (and a few others) the best for new homeowners is coming up in our next section.

Best Overall Credit Card for New Homeowners: Chase Freedom Unlimited

Buying a home is a complicated process, so we put Chase Freedom Unlimited first in our ranking for two very simple reasons: 1.5% cashback on all purchases, and 0% APR for the first 15 months.

From fixer-uppers to just a new couch or new furnishings for the guest room, what this means is the card helps you earn while you spend. The card also offers what amounts to a no-interest loan on house-related expenses for the first year after opening the account.

Cardholders also earn a $200 welcome bonus after spending $500 before the card’s third monthly birthday. To stock your brand-new pantry, we also like the 5% cashback on most grocery store purchases made through Chase Ultimate Rewards.

Aside from the 1.5% cash back on non-bonus purchases, this card also offers 5% cashback on all travel expenses arranged through the Ultimate Rewards program, and 3% on dining and drugstore purchases. These are two additional reasons to choose this card for your new home improvement project purchases at home improvement stores.

Although there’s a lot for a new homeowner to like about the Chase Freedom Unlimited card and Chase Ultimate Rewards, there are a few things we think you should be aware of before making your choice. First off, there’s an 3% intro balance transfer fee for each transfer.

First of all, Target and Walmart are excluded from the grocery points program, and the variable APR balloons from 14.99% to 23.74% after that introductory period has elapsed. So it’s important to plan carefully.

Otherwise, there’s no annual fee with the card. And that, coupled with the otherwise generous points program, means the Chase Freedom Unlimited card is the best choice for new homeowners to use when updating their fixer upper.

Best Credit Card for New Homeowners, Furnishing and Decor: U.S. Bank Cash+ Visa Signature Card

Maybe you bought your new home for additional space, and very little remodeling needs to be done.

In this case, you likely need some new furnishings for that extra bedroom, or perhaps an update to the decor in your new family room. We like the U.S. Bank Cash+ Visa Signature Card for instances like these.

Leading off the list of what we liked about the card are perks like 5% cashback on two categories of your choice. This rewards you more than Chase Freedom Unlimited’s 1.5 cash back.

More than the welcome bonus, what makes this particularly useful for new homeowners is that eligible categories include department and furniture stores, both relevant for new-look interiors. But the benefits don’t stop there.

Also of interest to a new homeowner is the 5% cashback on home TV, internet, and streaming services.

That means by choosing the right combination of categories, theoretically, you could earn as much as 5% cashback on your new TV or sound system as well as the streaming service of your choice. That’s hard to beat.

Additional things we liked about the Cash+ Visa Signature Card include 2% cashback on grocery shopping, gas, and restaurants, as well as 1% cashback on all other eligible purchases to help you save money in the long run.

There’s also no annual fee, a one-time $150 bonus after spending $500 within 90 days after opening the account — again, useful for that new home entertainment system and sectional — and even 0% intro APR on purchases and balance transfers for the first 12 months. Note that it requires a balance transfer of 3% of each transfer amount.

Following that, though, the APR on the card does go to a variable 13.99% to 23.99%. There are also some spending caps to be aware of as far as those 5% cashback rewards, and you do need to opt-in to those categories once a quarter.

With zero annual fee, the Cash+ Visa Signature card is a great way to save on furniture, decor, appliances, or home electronics for your new home.

Best Credit Card for New Homeowners, Home Repair, Remodeling, and Updates: Discover it Cash Back Card

Is your new home a fixer-upper? Or did you choose it for its potential rather than how the house presents as-is? In this case, you want a card to help you save on all your home repairs and updates after moving in. That card is the Discover it Cash Back Card.

Although you need to track rotating rewards categories carefully, the Discover it Cash Back Card makes it worthwhile. Aside from a welcome bonus, the card offers 5% cashback on home improvement stores and warehouse clubs, making it one of the best credit cards for home improvement. That way, you’ll save on what you need to complete the job.

Other things that make this Cash Back card the best for your interior updates include no annual fee and Discover’s first-year cash back match. Yeah, you read that right: Discover will match you dollar for dollar on all the cash you’ve earned, but only in the first year.

There are some restrictions to be aware of, and we’ll cover those now. Rewards categories do rotate. This means to take advantage of the offer for remodeling-related expenses, you’ll have to keep an eye out for when it comes time for department stores and warehouse clubs.

There’s also 0% intro APR on balance transfers, and at 26.99%, the interest rate on the card is a bit higher than average. Additionally, it comes with 3% balance transfers.

Pay off purchases of $299 or more within six months after making the purchase, though, and using the card is like a no-interest loan. Aside from not having to pay an annual fee, the card also offers reduced-APR financing on projects costing at least $2,000 with 84 fixed monthly payments.

But again, that offer must be arranged in advance. As can be seen, points and rewards are the primary incentive to use a card for whatever upgrade or renovation, or simply new furnishings and fresh decor for your house.

Best Credit Card for New Homeowners for Flexibility: Citi®️ Double Cash Card -18-month BT offer

Purchasing a home comes with a whole lot of responsibilities. Many times, it could be difficult to keep on top of all these tasks, and the last thing you need is to start worrying about which card you should use for which task. In situations like this, we recommend the Citi®️ Double Cash Card.

This card offers a 2% cash-back rate on all purchases, implying that you can use it for any purpose, whether repainting a room or renovating the kitchen. This 2% cash-back includes 1% on every dollar you spend while purchasing and 1% on every dollar you pay off. You must pay the minimum due on time to earn your cash back.

This welcome bonus and cashback are earned as Citi ThankYou Points, which can be redeemed at 1 cent per point as a statement credit, check, or direct deposit.

Another exciting thing about this card is that it offers 0% intro APR on balance transfers for the first 18 months. Subsequently, the APR will vary between 19.23% and 29.23%, depending on your creditworthiness.

Note that there is no cash back on balance transfers and no intro APR on eligible purchases. So, unlike other cards, the 0% APR doesn’t apply to both purchases and balance transfers. A balance transfer fee applies and carries a 3% foreign transaction fee too.

This card has flexible redemption options, allowing you to pick pay dates that suit your convenience. Also, it does not charge an annual fee or require any quarterly activation.

While this card is a great one, there are a few things to take note of. Firstly, this card does not offer a sign-up bonus; rather, thrives on ongoing benefits.

Also, you risk losing half of your cash-back rewards if you do not pay off your balance as when due. This zero annual fee card helps instill discipline, helping you keep on top of your finances.

Best Credit Card for New Homeowners, Putting Your Kitchen to Use: Blue Cash Preferred®️ Card from American Express

We agree that setting up your bedrooms and living rooms is one of the most enjoyable parts of getting a new home. However, the feeling of walking into a fully stocked and functional kitchen is second to none, especially for cooking and food enthusiasts.

The Blue Cash Preferred®️ Card from American Express comes at a high recommendation for helping you put your kitchen to use. This card offers a high cash-back rate for grocery shopping at supermarkets and incorporating streaming services into your entertainment center.

Aside from a great welcome bonus, it also offers high rewards at gas stations, which will be a great help when driving to and fro your new home. The following are the cash back categories it offers:

- 6% cash back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%).

- 6% cash back on select U.S. streaming subscriptions

- 3% cash back at U.S. gas stations and on transit (including taxis, rideshare, parking, tolls, trains, buses, and more)

- 1% cash back on other purchases

These cash backs are received as Reward Dollars and can be redeemed as a statement credit. Additionally, if you spend $3,000 in purchases on this card in the first six months after getting it, you earn a $250 statement credit. With all the kitchen expenses you’ll be footing, this shouldn’t be too hard to achieve.

This card has a 0% intro APR on purchases and balance transfers for the first 12 months from account opening. Subsequently, the APR will vary between 19.24% and 29.99%. You’ll pay a $0 intro annual fee for the first year and pay $95 yearly subsequently.

While this may seem like a lot, you can spend enough on the card in supermarkets and transit to make up for this cost and earn a profit. Another benefit of this card is that it offers $84 yearly in statement credit to subscribe to the Disney Bundle. This yearly credit is broken down into $7 monthly statement credit.

Furthermore, if you pay for an Equinox membership with your Blue Cash Preferred® Card, you’ll get $10 monthly in statement credit. While there’s no annual fee, there’s a 2.7% foreign transaction fee, which can escalate into significant foreign transaction fees with multiple purchases.

Best Credit Card for Home Improvement Projects: Bank of America®️ Customized Cash Rewards Credit Card

Newly purchased homes often require a lot of improvements, and furnishing and financing these could be expensive. We understand that you want your new home to be perfect, so we’ve brought another on the list of great credit cards for home improvement projects you may want to embark on – the Bank of America®️ Customized Cash Rewards credit card.

Even with a welcome bonus, the card offers 3% cash back from many services and contractors in several catagories:

- Gas

- Online shopping

- Dining

- Travel

- Drugstores

- Home improvement projects and furnishings.

Depending on your changing needs, you can change this category once a month. You can earn 2% cash back at wholesale clubs and grocery stores and 1% on all other purchases. This cashback is valid on up to $2,500 spent quarterly in combined purchases on the category and grocery store you choose.

You also stand the chance of winning a $200 online cash bonus if you make purchases of up to $1,000 in the first 90 days of opening your account. It requires a $0 annual fee. You also pay 0% intro APR for 15 billing cycles or purchases and balance transfers made within 60 days or two months from account opening.

Subsequently, a variable APR of 18.24% – 28.24% will apply, and a 3% charge that serves as balance transfer fee. These perks make this card a great choice to help you fill up your home with as many nice things as possible.

Additionally, if you’re a Preferred Rewards member, you can earn between 25% and 75% cash back on every purchase. However, because of the $2,500 quarterly cap on cash back, this card may not be so efficient for people who need to make large purchases and improvement projects.

Even though there’s zero annual fee, it has a 3% foreign transaction fee and foreign transaction fees tend to pile, costing you a pretty sum.

Best Credit Card for New Homeowners When Ordering In: Capital One SavorOne Cash Rewards Credit Card

When shopping for food, groceries, entertainment, and other home essentials, you need a card offering a welcome bonus and high cash back on purchases. The Capital One SavorOne Cash-rewards Card is one such card. Here are some of the cash-back rewards that this card offers:

- 3% cash back on all entertainment, dining, popular streaming services, and grocery shopping at stores, excluding Target and Walmart

- 10% cash back on purchases made on Uber & Uber Eats. Your monthly membership fee on Uber One is also covered until the 14th of November, 2024

- 8% cash back on Capital One Entertainment purchases, such as tickets for movie theaters, sports promoters, amusement parks, tourist attractions, aquariums, zoos, dance halls, and more

- 5% cash back on hotels and rental cars booked through Capital One Travel

- 1% cash back on other purchases

You have to agree that the 5% cash bank on hotels can come in handy if you’ve got any renovation work in your new home and need a hotel to spend the night. These rewards can be redeemed through Paypal and used at Amazon.com.

If you’re purchasing outside of the U.S. using this card, there is no foreign transaction fee, unlike AmEx cards. Foreign transaction fees can pile up significantly, so you can save on that. And it gets better!

You earn a $200 cash bonus if you spend $500 on purchases within the first 3 months from account opening. There is no annual fee and a 0% intro APR on purchases and balance transfers within the first 15 months of opening an account.

So, you only pay a balance transfer fee after the initial 15 months. Subsequently, there is a variable APR of 19.99% – 29.99%. There is also a 3% transfer fee within the first 15 months.

Best Credit Card for New Homeowners for Escaping Chores: Capital One Venture Rewards Credit Card

Last and not least on our list is the Capital One Venture Rewards Credit Card, and we vote it as the best for new homeowners looking to recover from the stress of purchasing a new home or take a break by traveling.

This card comes with an annual fee of $95. However, it has 0% intro APR on purchases or balance transfers. While this could be slightly discouraging, you can spend enough on your hotel/rental car booking and other purchases to make up for this amount and earn a mile profit.

While this card may not offer much cashback, it more than compensates for this in the rewards from travel purchased. So, if you’re looking to travel soon, this card is an excellent choice as it offers a one-time bonus of 75,000 miles after you spend up to $4,000 in purchases within 3 months of opening the account.

This bonus is equal to $750 in travel. You also earn 2X miles per dollar on every purchase and 5X miles per dollar on hotels and rental cars booked through Capital One Travel. There’s no limit to the number of miles you can earn, and these miles will not expire for the duration of the account.

Even though it has an annual fee, it makes up by letting you enjoy two complimentary visits per year to Capital One Lounges or Plaza Premium Lounges through the Partner Lounge Network. You also get a $100 credit for Global Entry or TSA PreCheck®.

What Is Best: a Credit Card or a Personal Loan?

The final decision a new homeowner may need to make is whether a personal loan is a better option for their project than a credit card. To help answer this question, we’ll now examine the pros and cons of personal loans vs. credit cards:

Personal Loans vs. Credit Cards: Pros and Cons

Chances are, if you’ve recently purchased a home, the very thought of taking out another loan sounds like the last thing you’d want to do. Nevertheless, here are some things to consider:

- Personal loans help you build credit. But if you qualified for a home loan, your credit is likely in pretty good shape already.

- Lower rates. Personal loans also offer lower interest rates than credit cards or other kind of financing, sometimes as low as 3% balance transfers. However, no rate offered on a personal loan will be as competitive as a 0% intro APR on balance transfers on a credit card.

- Flexible spending. Personal loans are often available quickly, and for pretty significant amounts. What’s more, you can spend the money on whatever you like once you have it, with no rotating rewards programs to track.

Some cons to consider before choosing a personal loan for your home improvement project:

- They accrue interest, fees, and penalties. Personal loan interest rates can sometimes be competitive, but other times those rates are as significant as a credit card. Furthermore, personal loans may require an application or processing fee, and you may incur a penalty if you miss a payment.

- They can damage your credit. Speaking of missed payments, personal lenders report any late or missed payments to credit reporting agencies, just like a credit card company. Like any kind of loan, then, it’s important to never borrow what you can’t pay back.

- It’s still debt. Regardless of the pros and cons of personal loans vs. credit cards: debt is still debt, and should only be entered into after careful planning and consideration, and only with a solid plan in place to pay it back.

Can I Pay My Mortgage Payment With a Credit Card?

In most cases, you cannot directly pay your mortgage payment with a credit card to your mortgage lender. Mortgage payments are typically made through other methods such as bank transfers, checks, online bill pay, or direct debits from your bank account.

However, there are some indirect ways to potentially use a credit card to pay your mortgage. These include:

- Third-party services

- Balance transfer checks

- Home Equity Line of Credit (HELOC)

While using a credit card with an annual fee to pay your mortgage can offer convenience and earn you credit card rewards, it’s generally not recommended due to the potential costs involved. Credit cards often have higher interest rates than mortgage loans, and using them to pay large expenses like your mortgage could lead to significant debt if paid off slowly.

How to Best Use a Credit Card for Home Repairs

Even with an annual fee, a credit card for home repairs can offer convenience, an avenue for earning rewards, and financial flexibility. Following some smart practices is essential to make the most of this option. These include:

- Before charging your home repairs to a credit card, create a detailed budget for the project, including the total cost of materials, labor, and additional expenses. Doing this will help you choose the right credit card and ensure you can comfortably pay off the balance.

- Next, select a credit card that aligns with your home repair needs. Look for cards with rewards or cash-back categories relevant to home improvement, special financing offers, online purchases, and competitive interest rates.

- Monitor your credit limit and balance transfer progress to avoid overspending.

- Pay off the credit card balance within the billing cycle to avoid interest charges. If that’s impossible, consider a card with a 0% intro APR on balance transfers, allowing you to spread out.

How Do Credit Card Reward Points Work?

There are in fact a few different kinds of credit card rewards. Rewards are nothing more than incentives a card company offers for consumers to use their card to make certain purchases.

These rewards programs are typically developed in conjunction with an airline, retailer, or another partner. Understanding what each one is and how they work is an important first step in selecting credit cards for any purpose.

We’ll define the different kinds of credit reward points now:

Types of Credit Card Rewards

Reward Points

Typically offered in categories like travel and dining, rewards points are an agreement between a credit card company and a retailer or service provider to offer bonuses to customers.

These points are most often awarded on a 1:1 basis or $1 in reward points for every $1 spent on a credit card in certain categories. However, some rewards programs depending on the rewards cards are more generous, but exclusions and restrictions typically apply.

Miles

A specific type of reward points offered by a credit card company are miles, earned by charging travel-related expenses to your credit cards. These programs are also most often 1:1 or sometimes 2:1.

Thus, for every dollar or two spent with a specific airline or travel partner, consumers earn miles that can then be redeemed on future travel discounts (allowing you save money), lodging, or even sometimes dining.

Cash Back

One of the most common reward points programs offered by a credit card company is cash back, usually on a 1:1 basis. Sometimes, though, cash back comes in as much as a 5:1 ratio when purchases are made on credit cards in certain categories.

Those categories often include gas at the pump, dining, and sometimes even grocery store purchases. And cashback rewards can most often be redeemed in the form of a statement credit, discounts with online retailers, or sometimes gift cards with specific department stores.

Rewards points programs often rotate on rewards cards, and they have deadlines by which the points must be redeemed. A consumer should consider these terms, exclusions, and restrictions before choosing from the list.

Planning carefully, though, and paying off the annual fee or credit balance in full, means these programs to earn rewards can be a great way to pad the budget for home renovations or to simply buy new furniture or appliances. This allows you to earn a little back while you spend, or to simply take a bit off the total purchase amount.

How to Use Reward Points at Home Improvement Stores

Once you’ve settled on a credit card program to earn rewards that best suits your purposes, how do you ensure you’re making the most of the offer? Here are some pointers:

- Use the right card for the right reasons: Once you select one of the many rewards cards, or maybe multiple cards, with the right rewards program or rewards programs for you, it’s important to pay attention to which card you’re using for what kind of transaction. And then, to actually remember to use the card. Signing up for a program to earn rewards won’t pay off any other way.

- Spend enough on the card to reach your goals: Even if you do use the right card at the right time, there are most likely minimum spending amounts that must be met within certain introductory periods. To maximize a 0% intro APR offer on balance transfers, for example, it’s important to spend and pay off your balance within that period, usually from within 12 to 15 months after account opening.

- Read the fine print: Credit cards reward programs can be used to your advantage, but these programs are not without exclusions and restrictions. Often, rewards offered in specific categories will rotate — for example, rewards at a department or home improvement coming only at certain times of the year.

For these reasons, new homeowners seeking to maximize their credit card spending should not only spend on the credit card but also make sure their spending is targeted when and where they need it most.

As can be seen, credit card rewards programs can be an effective way to finance home improvement projects or renovation project, while getting some cashback or rewards points back in the meantime. That’s true so long as the balance and annual fee are paid off on time and in full.

How to Maximize Credit Card Rewards After Account Opening

Maximizing credit card rewards requires a strategic approach to spending and card usage. Here are some tips to help you get the most out of your credit cards:

- Use categories of bonuses offered by your credit card to earn higher rewards.

- Combine different reward categories to maximize benefits. For instance, use a card that offers welcome bonus rewards for dining at a restaurant that’s also part of a shopping portal or loyalty program for additional rewards. Online shopping on certain websites can contribute too.

- Interest can quickly negate the value of your rewards. Therefore, pay your credit card balance in full each month to avoid interest charges.

- Aside from a welcome bonus, watch for special promotions, sign-up bonuses, and limited-time offers.

- Some cards offer referral bonuses for bringing in new cardholders. Refer friends and family to earn extra rewards.

- Make occasional small purchases on cards you’re not using regularly to keep the accounts active and prevent them from being closed due to inactivity.

- If your card has an annual fee, ensure the rewards you earn outweigh the fee’s cost. If not, consider downgrading or canceling the card.

- If you have multiple credit cards from the same issuer, see if you can combine rewards into one account to increase their value.

Which Credit Card Bonus Categories Are Best for New Homeowners

The credit card bonus categories best for new homeowners are:

- Home Improvement Stores

- Furniture and Furnishings

- Utilities

- Groceries

- Home Services

- Insurance Premiums

- Moving Expenses

- General Cash Back

Which Credit Card Has the Best Rewards for Home Improvement?

The credit card that offers the best rewards for home improvement projects is the Bank of America®️ Customized Cash Rewards Credit Card. This card offers 3% cash back in any category of your choosing from the following six:

- Gas

- Online shopping

- Dining

- Travel

- Drugstores

- Home improvement and furnishings.

With this card, you earn 2% cash back at wholesale clubs and grocery stores and 1% on all other purchases. This cashback is valid on up to $2,500 spent quarterly in combined purchases on your chosen category and grocery store.

Should I Apply for a New Credit Card Before I Buy a House?

Deciding whether to apply for a new credit card before buying a house depends on your financial situation and the timing of your home purchase.

If you’re planning to buy a house soon, avoiding major changes to your credit profile is generally advisable, such as applying for a new credit card, especially one with an annual fee. This ensures that your credit score remains stable for mortgage approval.

However, if you have a good credit score and are eligible for a credit card with favorable terms, getting one before buying your house could enhance your financial flexibility and give you access to better rewards and lower interest rates.

Frequently Asked Questions

Can I Get a Credit Card After I Buy a House?

Yes, you can apply for a credit card after buying a house. Buying a house does not generally prevent you from obtaining a new credit card. However, there are a few considerations to remember, the most important of which is your credit score.

Suppose you’ve recently purchased a house and obtained a mortgage. In that case, the mortgage application and any other credit checks associated with the home purchase process might have impacted your credit score. If your credit score is not great, this may affect your credit card approval.

What’s the Best Way to Charge a Big Purchase for Your Home?

A credit card is the best way to charge a big purchase for your home. A credit card can provide convenience, flexibility, and potential rewards or cash back even with an annual fee. Some cards also offer introductory 0% APR periods on the balance transfer, which can help spread out payments without interest.

Can a Credit Card Extend Your Purchase Warranty?

Yes, many credit cards offer a benefit known as Extended Warranty, which can extend the manufacturer’s warranty on eligible items you purchase if they accept credit cards. This warranty is typically extended for one year but could be less.

Conclusion

And there you have it, in this article we presented the best credit cards for new homeowners. Whether you’re fixing up your fixer-upper, or simply furnishing and decorating the extra space you now enjoy in the home of your dreams, the primary incentives for choosing credit cards for your new home remodeling project are 0% intro APR financing periods and targeted rewards programs.