This article is the first in a three-part series explaining why the economic inflation we are experiencing was all-too-predictable, and outlining the things that ordinary citizens can do by way of self-protection to hedge against it and enhance their finances. The first topic of discussion will be government mismanagement of the money supply and the corrections that need to happen, followed in the second installment by a discussion of government mishandling of the pandemic and the resulting supply chain crisis and cost-push inflation, then the last installment will talk about pro-active steps you can take to protect and enhance your finances in the current economic environment.

The current inflationary woes in the United States—and a good portion of the world—were entirely predictable and mostly preventable. Live and learn, one might say, except that government bureaucracies rarely do, or perhaps more realistically, they have a vested interest, all protestations to the contrary, in their own growth and the extension of their influence and control, and this governmental self-interest, again, all protestations to the contrary, is often at odds with the well-being of the governed. Our current problems are almost wholly the result of the wanton expansion of the money supply and the creation of supply chain crises through inept and draconian measures in response to the pandemic. Let’s have an Economics 101 review of the diagnosis and treatment options.

Table of Contents

Contents

The Importance of Economics

Economics is the social science that studies how individuals, corporations, and societies in varying contexts and on varying scales go about making decisions regarding how to use their limited resources. Every nation, every corporation, and every individual, functions under a wide variety of constraints as they seek to maximize their limited resources to produce and acquire the goods and services that satisfy human needs and wants. Economists collect and analyze the relevant data, try to discern the cause-and-effect relations among economic decisions and their consequences, and recommend policies and actions based on circumstances and desired outcomes.

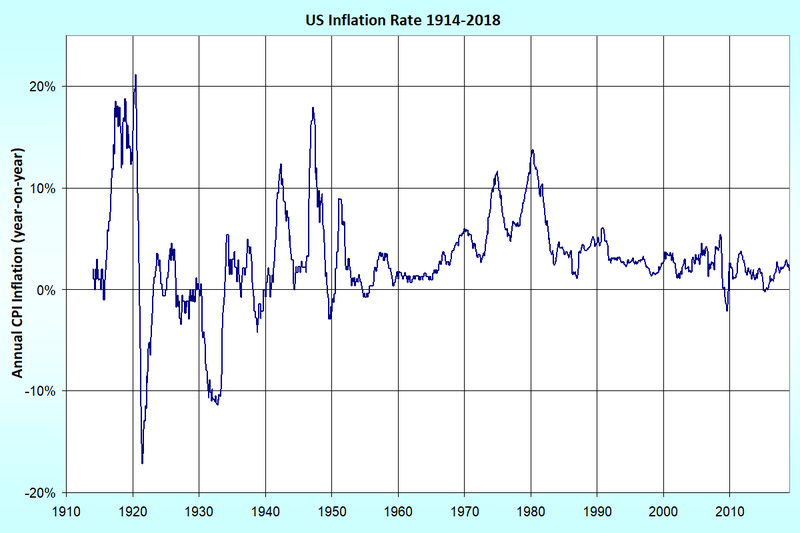

Sound economic practice is inextricably bound to improved standards of living and quality of life, so avoiding wishful thinking and adhering to hard economic realities is necessary. In this regard, it’s difficult to imagine an economic force with more destructive potential than inflation. Every citizen needs to understand what inflation is, what causes it, who benefits from it, who is harmed by it, and the steps responsible governments need to take to prevent it, or if worse comes to worst, to cure it. So here we go.

The Money Supply and Economic Mismanagement

Inflation occurs, quite simply, when the level of prices in an economy is rising universally: the cost of everything is going up. And one of the laws of economics, confirmed over centuries of experience, is that inflation is everywhere and at all times a monetary phenomenon. This is not to say that no one will try to convince you otherwise. But anyone who tries to do so is either lying to you because they have a vested interest that is being served, or they are ignorant of a basic economic truth that is not hard to understand. Politicians and government officials who would tell you otherwise generally fall into the former category, because governments benefit from inflation. Their citizens do not, which is why basic economic literacy is so important for a competent citizenry, and its absence endangers all of us.

Why Systemic Inflation is a Monetary Phenomenon

What I am about to tell you is neither original nor revelatory. Economists as different as those from the Austrian, monetarist, and Keynesian schools all agree: substantial systemic inflation is a monetary phenomenon. When the quantity of money grows more rapidly than the goods and services available for purchase in a currency, prices in that currency will rise across the board. Furthermore, the quantity of money in every country in the modern world is determined by its government.

Since I’m much more sympathetic to economists of the Austrian School, like Friedrich Hayek (1899-1992), and to monetarists, like Milton Friedman (1912-2006), than to Keynesians, let me bolster the case by quoting as good a Keynesian as any for you, John Maynard Keynes (1883-1946) himself, citing an insight by, of all people, Vladimir Lenin (1870-1924): “There is no subtler, no surer means of overturning the basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner that not one man in a million is able to diagnose” (Keynes, The Economic Consequences of the Peace, 1920, p.236). One would hope that Keynes’s dismal one-in-a-million assessment is hyperbole. But let’s have the diagnosis, just the same.

Here is a basic economic fact extensively confirmed by history: when the money supply grows faster in quantity per unit of output in a nation, proportional inflation is the inevitable result. Output can only grow at a relatively slow pace because it is limited by the natural and human resources available and the ability of the nation to use them. Modern forms of money are subject to no such physical limits, however, and the nominal quantity of units of currency can grow at any rate.

Historical examples abound. Consider what Keynes foresaw from the reparations imposed upon Germany by the Treaty of Versailles. The debt burden was intolerable, and the Weimar Republic in Germany in the 1920s, in its economic ignorance, decided just to print the money needed to pay its debts, inducing the hyperinflation that opened the door for Hitler. The Weimar government had the exclusive right to print German marks, and faced with insuperable debt, was unable to resist the temptation. It simply printed whatever cash it needed to pay its overwhelming bills, running more than 1700 printing presses around the clock. The result was entirely predictable: hyperinflation.

In 1922, the inflation rate in the Weimar Republic soared past 100% per month and reached 6000% by the end of the year. Then things really got out of control. In 1923, a loaf of bread cost over 200,000 marks, a pound of meat cost 2 million marks, and prices were rising 41% per day. Waiters changed the prices on menus at restaurants while patrons were being served, and the customers gobbled down their food before the meal became unaffordable. Factory workers were paid twice a day, with families collecting the money in wheelbarrows and running off to spend it before it became worthless. And this second factor, the increased velocity of money, that is, the increased speed of its circulation due to loss of confidence in its retaining its value, had the same effect as exponentially increasing the money supply, landing a hyperinflationary double-whammy on the hapless citizenry.

Another interesting historical example comes from the Confederacy in the Civil War. The South initially financed the war by printing Confederate money, which produced inflation of about 10% per month from the autumn of 1861 through the spring of 1864. To stop this process, in May 1864, monetary reform was introduced to reduce the stock of money. The result was a drop in the price index (deflation)—despite everything else that was going wrong for the Confederacy and would normally produce inflation—showing that reduction in the money supply is a powerful tool for countering inflationary forces. We will revisit this topic when we consider what the government should do when it comes to its senses.

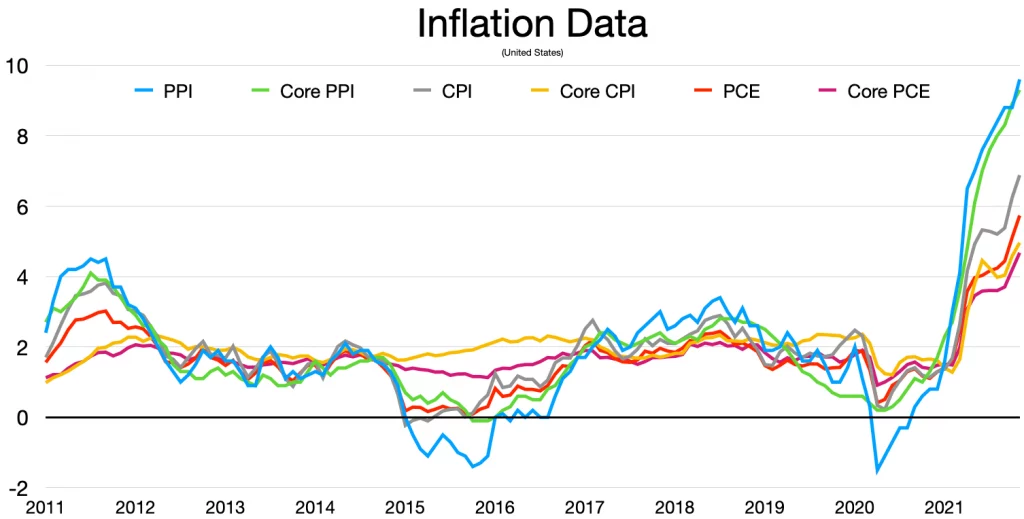

This story is repeated over and over in economic history. If we consider the inflationary period in the history of various countries—the United States, Germany, the United Kingdom, Japan, and Brazil—from the mid-1960s through the late 1970s, and compare the quantity of money per unit output with respective consumer price indices, expressing each series as percentages of their average value over the whole period in question, then there is a remarkable confluence, despite the fact that there is nothing that dictates the two graphs should coincide for any given year (M. Friedman, Free to Choose, 1980, pp.256-261).

Of course, correlation is not causation, and one may legitimately ask whether there is a common cause for both things or, if not, which causes which? The answer is not far to seek. The money supply does not grow because prices are rising, rather the reverse: in the comparisons just discussed, there is a six-month delay between the quantity of money increase for each national economy, and the later inflation indicated in the consumer price index. It is crystal clear that it is the growth of the money supply faster than growth in output that is the driving factor in inflation.

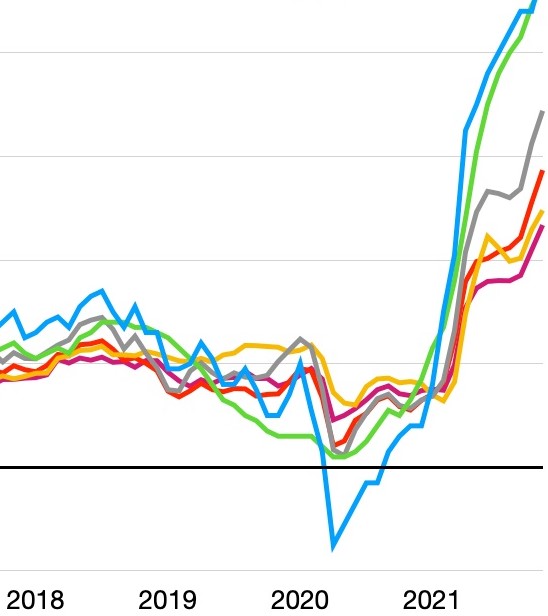

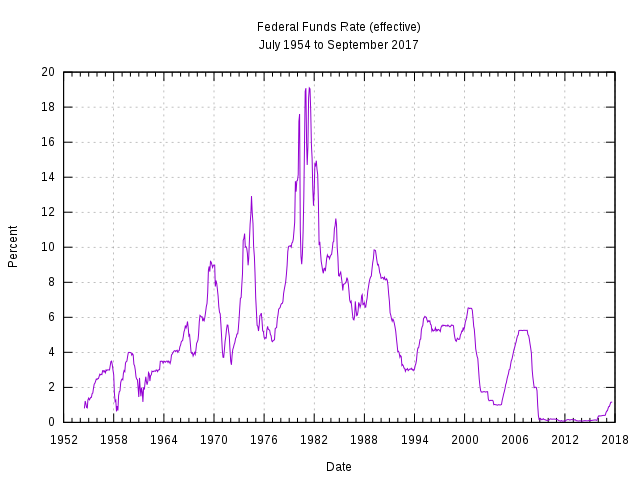

We can see this quite clearly in our current situation, displayed in the two charts below. If we consider, as a critical forecaster of inflation, the growth of the M2 money supply (which includes the M1 money supply—physical cash and checkable deposits—plus money that is less liquid, including savings bank accounts), there were vast additions to the U.S. money supply beginning in early 2020. There was also a 3.5% nosedive in the GDP during 2020, followed by anemic growth 2021, so the growth in the U.S. money supply has vastly outstripped national output. Taking into account a lag time extended by consumer uncertainty under gradually easing lockdowns, we would expect to see substantial inflation emerging around one year later. While there can be little satisfaction in being right about this given the misery it will cause, this is, nonetheless, exactly what we see:

Constructed from Federal Reserve Data

The government’s decision to create and indiscriminately give away money based on taxable income level and independent of actual need in response to the job losses, business destruction, and supply chain inflationary pressures created by its own inept response to the pandemic has, predictably, produced substantial inflation. Before we take a look at what we might expect government to do if it takes responsibility for the crisis it has created, let’s have a brief overview of how the government creates money, why we’re no longer on the gold standard, false explanations for generalized inflation, and why inflation benefits governments but hurts everyone else.

- Price Inflation Hits 7.5%, Highest in 40 Years: What Will the Fed Do?

- Red Hot Inflation: Wholesale Prices Jump 9.7% in January

How Banks and the Government Create Money

This is neither the time nor the place for an exhaustive review of the nature and creation of money, which can be found here:

Instead, I want to focus briefly on how banks increase the money supply through fractional-reserve banking, and then quickly review how the government bank—the Federal Reserve—controls the money supply through its monetary policy.

Modern banks contribute to the creation of money by holding only a fraction of the reserves necessary to cover deposits and loaning out the rest, thus adding to the total money supply. They do this in the realization that not all of their depositors are going to want all of their money at the same time, so money is loaned to others in order to earn interest that is then partly shared with the depositors whose money is being loaned. This effectively adds to the money supply over and above that created by the government. Meanwhile, the banks’ depositors are writing checks on their accounts even as part of the money in those accounts is circulating as loans to others, but rather than paying the full amount on all the checks, only a fraction of the amount is needed to settle the net difference among the banks as, for example, checks written on accounts in Bank A are deposited in Bank B, and vice-versa.

This “fractional-reserve banking” works fine in normal times, but it can run into trouble if depositors fear they will not be able to get their money and there is a run on the banks. This is what happened in the Great Depression of the 1930s, when hundreds of banks collapsed and the money supply contracted by one-third. To avoid this happening again, the Federal Deposit Insurance Corporation (FDIC) was created. The FDIC guarantees government reimbursement (up to $250,000 per depositor) of deposits in insured banks if that bank collapses, removing any reason for depositors to start a run on a bank.

While the FDIC acts as a firewall against bank failures, the government has a more comprehensive way of controlling the national supply of money and credit through its central bank, the Federal Reserve (the Fed). The Fed controls the behavior of all private banks by specifying the fraction of their deposits that must be kept in reserve, by lending to banks money that it creates that can then be loaned to the general public, and by setting the interest rate on money that it loans to the banks, thereby controlling the interest that private banks will charge on the loans that they make. With this in mind, let’s take a closer look at how the actions of the Fed function to expand or contract the national money supply.

How is it that a fiscally irresponsible U.S. government could just write checks to everyone they hoped would appreciate a few extra bucks during the extended (and equally mismanaged) COVID lockdowns? After all, any deposit made by a private bank into an account depends on other deposits that exist. While this can be true for a central bank, however, it doesn’t have to be. A central bank, like the Fed, can create money used for deposits in accounts at other bank accounts without drawing on existing deposits at all. This fiat act brings money into existence out of nothing.

Of course, to prevent the Fed from just creating money to spend—a real temptation, as we saw in the case of the Weimar Republic—the Fed doesn’t get to spend the money it creates. That’s the job of the U.S. Treasury. There’s a little dance and some legerdemain that’s done in an effort to provide accountability. Actual accountability depends on the integrity of those running the institutions, however, and their ability and willingness, for the good of the republic, to resist political pressure. If you’re worried this could be a problem at times, go to the head of the class. But for now, we need to finish our tale of money creation with a short description of the U.S. Treasury-Federal Reserve polka twirling across the dance floor (hopefully not eventually the graveyard) of the American economy.

When Congress decides it wants more money—to pay its bills, bribe the public, or spend on boondoggles—and it’s run out of the public’s money collected through taxes, it asks the U.S. Treasury to issue bonds (also called treasuries) for sale in the form of T-bills, T-notes, and T-bonds, depending on how long they take to mature, with promise of payback with interest (usually quite modest) at maturity.

Since the Federal Reserve Act specifies that the Fed can only buy bonds on the open market—it can’t buy them directly from the U.S Treasury—it credits the account of the bank, foreign government, or other relevant third party that sold it the bond. Since the Fed didn’t need to debit a prior deposit to pay for the bond, by buying bonds, the Fed creates money and expands the money supply. Here is the Fed’s current balance sheet:

As you can see, the Fed owns a lot of treasuries, as well as a hodge-podge of other dodgy securities, loans, and other holdings. As of the beginning of 2022, the Fed has about $5.7 trillion in such bonds. These bonds are liabilities for the U.S. Treasury that it is supposed to pay back with interest at maturity. When the Fed sells these treasuries, they are paid off and retired, thereby eliminating the money associated with their creation and contracting the money supply.

The Gold Standard, Its Demise, and the Specter of Modern Monetary Theory

In the world of fiat currencies, a limit is imposed on the creation of money by the artifice of loaning it into existence. This may seem rather complicated, but some constraint is necessary. This constraint used to be provided by the gold standard.

For our purposes, we’ll truncate the story of the gold standard in the United States and summarize it from the turn of the twentieth century onward. In March of 1900, the United States reaffirmed its commitment to the gold standard with the “Gold Standard Act,” which established a gold reserve for government-issued paper money. The legislation declared the gold dollar to be the standard unit of account and required all forms of government-issued money to be maintained in parity with it.

This arrangement was inelastic and proved intractable in short order. Because there was seasonal variation in the need for cash transactions, especially at harvest time, and because fractional-reserve banking was the standard practice and the system of gold-bound legal tender notes was not elastic, banks experienced money “shortages” when greater-than-normal numbers of customers demanded cash from their accounts. Any inability to provide the needed cash could lead to a run on the bank and a bank failure.

This problem was intended to be addressed in two ways by the creation of the Federal Reserve System in 1913. First, it would enable banks to borrow money to satisfy customers’ demands for cash when money was tight, and secondly, it created a new form of cash—Federal Reserve notes—that could be expanded or contracted to respond to the need for more or less money. Even so, the Fed operated under the gold standard: the dollar was still defined in terms of gold and Federal Reserve notes were redeemable in money that was legal tender, with a percentage of gold cover held for the notes themselves.

While much of the world was forced off the gold standard during the First World War in order to be able to expand the money supply to cover war costs, the United States remained on the standard, probably because it didn’t enter the war until 1917 and it was over in 1918. The collapse of the stock market in 1929 and numerous subsequent runs on the banks from 1930-1933, however, demonstrated that the Fed was unable to provide sufficient liquidity to the banks, largely because of the constraint imposed by the gold standard. To keep the economy from collapsing, the Fed needed to expand the money supply to meet public demand and to lower interest rates, but this would have driven investors abroad and accelerated the exportation of gold, making it increasingly difficult to maintain the legal gold value of the dollar. Staying on the gold standard required a policy of contraction when the economy was already in recession, thus exacerbating the problem.

But the gold standard wasn’t the issue as the depression developed and persisted through the 1930s, because in 1933 Franklin Roosevelt, through a series of executive orders, followed by legislative actions and court decisions, took the United States off the gold standard, suspending the convertibility of currency into gold and nationalizing private gold holdings. For private citizens, the dollar no longer had a value in gold in any practical sense. A quasi-gold standard remained for international transactions under the Gold Reserve Act of 1934, however, covering official transactions with the central banks of other countries.

This international standard without domestic convertibility was retained under the Bretton Woods international monetary agreement of 1944. This agreement also established the International Monetary Fund (IMF) to stabilize exchange rates among currencies and cushion inflationary or deflationary pressures in countries with undervalued or overvalued currencies until proper valuation was achieved, and it also established the World Bank as a resource for fighting poverty in developing nations.

Once the restriction of a domestic gold standard was gone, Roosevelt implemented Keynesian recommendations of currency devaluation (which amounts to the same thing as monetary expansion) late in 1933 in an effort to overcome liquidity problems. The deepening of the economic depression and skyrocketing of unemployment throughout the remainder of the 1930s thus can hardly be blamed on the gold standard. In fact, Keynesian, monetarist, and Austrian economists all agree that the gold standard was not the problem.

So what was the problem? Tariffs and taxation. In 1930, Herbert Hoover and Congress thought that imposing tariffs on thousands of imports, no matter their country of origin, would protect American businesses and farmers and secure the nation’s economy, so they passed the Smoot-Hawley Tariff Act. Understandably, other countries responded by imposing their own tariffs, imports became largely unaffordable, and global trade declined by 65 percent, deepening the depression not just in the United States, but around the world.

Hoover then worsened the problem through gigantic tax increases. Desperate to balance the Federal Budget, under Hoover, Congress passed the Revenue Act of 1932 that raised corporate tax rates almost 15 percent, raised income tax rates across the board with the highest rate moving from 25 percent to 63 percent, imposed consumption taxes on everything from chewing gum to gasoline, and doubled the estate tax. Franklin Roosevelt continued in this vein. In an effort to fill the coffers to pay for all the government social programs he created, he instituted the Social Security tax, and in a series of legislative acts—the Revenue Acts of 1934, 1935, 1936, and 1940—increased corporate taxes and progressive taxation across the board until, by 1940, the highest income tax rate was 79 percent!

Other governments behaved similarly. For anyone with a basic understanding of human nature, the predictable result of all this slap-happy tax slapping was that bank credit contracted, businesses cut down their work forces or went bankrupt, unemployment went through the roof, there was a huge reduction in consumer spending, efforts at tax evasion were rampant, and what might have been a shorter period of hardship became the Great Depression era (1929-1941).

But we were talking about the gold standard. Let’s finish that story and then consider the implications this economic history has for a new-fangled approach to macroeconomics that’s all the rage among the print-money-and-spend-like-there’s-no-tomorrow crowd, namely, the advocates of Modern Monetary Theory (MMT), like Stephanie Kelton, who are having a substantial and regrettable influence on monetary policy debates.

As we noted earlier, after Roosevelt took us off the domestic gold standard, there was no private market for gold in the United States. Private markets existed abroad, however, and the law of supply and demand in these markets led to prices that deviated from those used for international transactions. By the late 1960s this was posing a serious problem and all attempts at government intervention in the gold market had failed.

In August 1971, the Nixon Administration announced that gold would no longer be converted into dollars at the official international exchange rate. This was intended to be temporary, but it became permanent because every subsequent attempt to establish a new official price for the dollar in terms of gold was unsustainable. In October 1976, the government officially amended the Bretton Woods Agreement Act to remove any definition of the dollar in terms of gold. At this point, the United States monetary system officially became a pure fiat currency, though it had been functioning that way without any pretense of restraint since 1971.

It’s no secret that we had inflation that frequently strayed into the double-digits in the 1970s combined with high unemployment (stagflation), and a host of other economic and political crises. The Keynesian thinking dominating the Fed in this era held that inflation should have a positive relationship with economic growth and an inverse relationship with unemployment: the basic idea was that an increase in prices would encourage firms to expand and hire more employees, despite rising production costs. The stagflation of the late 1970s severely challenged this theory.

In other words, the 1970s was a time of high inflation, rising unemployment, and sluggish economic growth, a scenario that contradicted Keynesian analysis. A different approach was needed. Enter Milton Friedman, who set aside the cost-push inflation explanation for the world economy based on oil supply-shock prices, emphasized the monetary nature of inflation and, having predicted the stagflation that was occurring, counseled a different approach. To get the economically devastating impact of inflation under control, he recommended that the Fed implement a policy that would contract the money supply. Because it would cause a lot of pain, no one had the guts to do this until Paul Volcker became Chair of the Federal Reserve in 1979, serving until August 1987.

How did this policy work? The demand for money is inversely related to interest rates. The higher the interest rate offered on alternative assets, the less money people want to hold, so raising interest rates is a very effective way of contracting the money supply. With Reagan’s support, Volcker raised the interest rate set by the Fed to 20% in 1980 and kept it high until inflation was brought to a standstill. The unavoidable side-effect was to put the economy into a recession for two years, with the national unemployment rate peaking around 10.8 percent in late 1982.

Image Credit: Wikimedia Commons

Once inflation was under control, it was necessary to stimulate the economy to get things going again. In Reagan’s view, government was the source of many of the problems, so limiting its scope and reducing its endless and ever-changing list of regulations was paramount. Stimulation of the economy was to be achieved by lowering taxes on individuals and corporations. The growth of the economy catalyzed by the expectations accompanying fewer regulations, a stable regulatory regime, and lower tax rates, was expected to lead to an actual increase in tax revenues and contribute to deficit and debt reduction. It did, though government spending was not lowered, but shifted from domestic programs to defense to reach a political objective: forcing an unstable Soviet Union to spend itself into oblivion. This objective was also achieved with the collapse of the Berlin Wall in 1989 and the eventual dissolution of Iron Curtain and the Soviet Union itself in 1990-91.

Understanding this history is central to knowing what to do and what not to do in our current inflationary environment, which brings us back to the specter of Modern Monetary Theory (MMT). It is the perennial desire of human beings to have their cake and eat it too. We would like to be able to create money out of thin air and spend it on the satisfaction of our wants and needs without any cost or sacrifice. This is the sugar-plum vision that modern monetary theorists have dancing in their heads and are trying to get dancing in your head. It is a vision of unlimited resources. Economics, however, is the social science of how to make decisions in a reality in which there are limited resources and in which, quite simply, you can’t have your cake and eat it too.

RELATED: What Do Americans Spend the Most Money On?

According to MMT advocates like Stephanie Kelton, governments can create money for whatever they perceive themselves to need because the state cannot go bankrupt (Argentina, anyone?). This would, of course, also be a way for the public sector to buy out the private sector, thus advancing a socialist agenda. Capitalism could not compete because capitalists can’t print their own money, they have to earn it through their own ingenuity. Is it any wonder, then, that Kelton was the chief economic adviser to the Bernie Sanders campaign, or that she’s an intellectual hero of that illustrious bartender from the Bronx, Congresswoman Alexandria Ocasio-Cortez?

Now, to be fair, what modern monetary theorists are really saying is that a country like the United States, whose debts are denominated in their own currency, cannot default, whereas countries like Argentina, whose debts are in foreign currencies, can, and this is why a country like the U.S. can supposedly print money with impunity. But a guarantee against default is not a guarantee against hyperinflation, which will destroy a country, just the same. MMT economists thus counsel taxation to contract the money supply as the cure for inflation. In other words, as prices rise beyond affordability, governments should further limit the financial resources of individuals and corporations, and in the process, of course, further load their own coffers. This is insanity.

There is, therefore, a reason for the pas de deux performed by the U.S. Treasury and the Federal Reserve in which money is loaned into existence: it prevents Congress from having a carte blanche to print money, debauch the currency, and run the country into the ground. As we saw earlier, not just Keynes, but even Vladimir Lenin, understood this. The modern monetary theorists, who are neo-Keynesians on steroids, would do well to take note.

Everyone else would also do well to take note. Caveat emptor. MMT may be telling you what you want to hear—that you can spend money you magically create to your heart’s content and do so with impunity—but it is the economics of fantasy land.

Inadequate Explanations for Generalized Inflation

It should be clear by now that generalized inflation is a monetary phenomenon. Are there any other factors that can contribute to systemic inflation? Let’s talk about cost-push inflation and demand-pull inflation in this context before debunking some diversionary candidates that politicians and bureaucrats use to distract from the government’s mismanagement of the money supply.

Cost-push inflation is a supply-side problem. When the aggregate supply of goods and services is constricted because of increased production costs or some natural event that disrupts the supply chain, cost-push inflation results. In this case, demand remains static but the reduction in supply causes inflation.

Demand-pull inflation is a consumer-driven problem. When aggregate demand for goods outpaces the aggregate supply, prices will rise across the board. This can happen when the economy is growing and consumers feel more confident, or when consumers have more money to spend because unemployment is going down, or because there is an expansion in the money supply (the latter highlighting the fundamental status of the monetary explanation of inflation). In this case, supply remains static and the increase in demand drives inflation.

The inflation we are currently enduring has two primary causes: (1) the wanton expansion of the money supply by numerous governments; and (2) cost-push inflation induced by the supply shock created by government lockdowns universally disrupting supply chains. We will deal with government mismanagement of the pandemic and the supply chain crisis in the second article in this series.

With regard to demand-pull inflation, the reason that demand is up with respect to supply is that supply has been interrupted while demand has remained constant, so there is considerable pent-up demand created by the backlog. It is also the case that many people who had no need of a stimulus check still received one and they have extra money to spend—so the problem here is the increase in the money supply driving increased demand. For the moment, however, I want to focus on various diversionary “explanations” offered by blame-shifting politicians and bureaucrats who would like you to believe that anything and anyone but the government is responsible for widespread inflation.

The first diversionary explanation, and a favorite one of politicians of certain stripe, is that greedy corporations are charging too much. Take Senator Elizabeth Warren (D-Mass), for instance, who was recently schooled by Elon Musk in a tweet war on taxation that she initiated, and who also remarked after hearing the latest inflation numbers that “we can’t overlook the role that concentrated corporate power has played in creating the conditions for price gouging.” Almost all economists disagree, focusing instead on the money supply, supply chain bottlenecks, and increased demand as causes for our current inflationary predicament. Corporations are in business to make profit, yes, but this is true under all economic conditions, not just when inflation is rampant, and it does nothing to explain why inflation is so much greater at some times and places than at other times and places.

Sadly, President Biden seems to favor a version of this diversionary tactic as he now proposes to fix inflation by focusing on corporate greed and increasing corporate competition. This is all window-dressing. It’s not as though antitrust legislation that would take on the contemporary version of Eisenhower’s military-industial complex—namely the Big Government-Corporate Media-Big Tech complex that is seeking to control the flow of information and force conformity of opinion on a republic founded on the freedom of speech—would be a bad thing. This would not address inflation, of course, but it is needed. That isn’t Biden’s focus, however. He’s going after oil companies and other favorite bogeymen of the left. It’s all smoke and mirrors aimed to deflect attention from irresponsible government monetary policy.

- Biden Focuses on Corporate Greed as the Cause and Competition as the Cure for Inflation

- Gas Prices Rise as Biden Administration Targets Oil Companies

Switching to politicians of a different stripe, labor unions are sometimes invoked as catalysts of inflation. While we’ve heard plenty recently about how, for example, teachers unions have been exacerbating the education crisis during the pandemic, we have yet to hear them being blamed for our inflationary woes. Nonetheless, unions do sometime get accused of using their monopoly power to drive up wages, which in turn drive up production costs, which in turn drive up prices. This kind of union-driven wage-price spiral inflation, while it describes some cases, has no general analytical validity.

That this is so is evident from the fact, discussed earlier, that graphical comparisons of the relationship between the quantity of money per unit output with consumer price indices as an inflation indicator, expressed as percentages of their average value over a given period, display a remarkable confluence independent of the country chosen. Consider our earlier examples of this confluence in the United States, Germany, the United Kingdom, Japan, and Brazil from the mid-1960s to the late 1970s: unions are of almost no importance in Japan, they are under government control in Brazil, they have reasonable strength in Germany and the United States, and are very strong in the United Kingdom. In short, unions did not produce the generalized inflation simultaneously experienced in these different countries. Wage increases that exceed corresponding increases in productivity are the effect of inflation, not its cause. It was the expansion of the money supply that caused the inflation.

Low productivity is also sometimes put forward as an explanation for inflation. It is true that there is nothing more important for the long-term economic health of a country than continued improvement in its productivity year over year. There are, however, offsetting factors in this regard. While lower productivity raises business costs for a time relative to unit labor costs that would be offset by raising prices, lower productivity could well be balanced by slower growth in aggregate demand through employee layoffs, reduced business investment, and falling stock prices reducing household wealth and consumption. Beyond this, as we have discussed, changes in output are insignificant relative to changes in the quantity of money. Productivity is an extra on the movie set of inflation; the money supply is the movie star.

Another explanation sometimes put forward by those who would seek to absolve their own government from its responsibility for inflation, is to suggest that inflation is being imported from abroad. In a strict sense, this would mean that inflation in foreign countries is creating inflation in the home country. It is an explanation that had more traction when the major currencies of the world were linked by a gold standard, but this hasn’t been the case since at least 1971. The value of most national currencies floats freely on the foreign exchange market in relation to the supply and demand for that currency relative to other currencies. In a more pedestrian sense, then, a rise in the cost of imports can be caused either by foreign countries charging more for their goods, or by the home currency losing value on the international exchange. The fact that other countries have also been expanding their money supplies and instituting lockdowns that create supply shocks and cost-push inflation, conjoined with similar policies at home that debase the dollar, the ongoing surge in import prices in the United States should not be a surprise.

On the other hand, if a foreign nation is experiencing inflation, the fact that the price of goods is going up in terms of its own currency need not mean that it will export inflation if its currency is losing value in international exchange, for other national currencies will be worth more in comparison. And, of course, if the home currency is losing value, then the reason that imports cost more has nothing to do with foreign countries charging more for their goods. So the only interesting case is when exchange rates are relatively stable, supply and demand for goods is stable, and a foreign country simply starts to charge more for its exports. Unless there is some kind of cartel of nations colluding, however, if the same commodities are available from other countries, the exports of those countries charging more will suffer until their prices are brought into line with the rest of the world. So there is no really interesting sense these days in which inflation is imported, and while inflation often occurs in many different countries at the same time at different rates, it is not really an international phenomenon in the sense that each country lacks the separate ability to control its own inflation.

Finally, let’s revisit the issue of supply shock induced cost-push inflation and consider an historical example. Back in 1973, the OPEC cartel declared significant cutbacks in production and an embargo against the United States and other industrialized nations that supported Israel in the Yom Kippur War. The reduced oil supply raised the price of oil considerably, generated lines that were sometimes miles long at gas pumps in the U.S., and reduced the supply of goods and services available because foreign exports had to be increased to pay for oil. This was a one-time price shock to Western nations, however, that did not create lasting inflation.

Consider how it played out over the next few years in Germany, Japan, and the United States: within five years, inflation in Germany subsided from 7 percent annually to 4 percent in 1979; in Japan it declined from a high of 24.9% in February of 1974 to 3,7% by 1979; but in the United States it declined from 11.05% in 1974 to 5.74% in 1976, then rose again to 11.25% in 1979 and, spurred by a second “energy crisis” associated with the Iranian Revolution in 1978-79, continued to rise to a high of 13.55% by 1980. These huge differences cannot be explained by an oil shock that was common to all three countries. Both Germany and Japan were completely dependent on foreign oil, yet they cut inflation more effectively than the United States, which was only 50-percent dependent on foreign oil during this time. Supply shock induced cost-push inflation had an effect in all three countries, but the United States was the only country that continued to expand its money supply throughout the 1970s, generating what is known in the history of the Fed as “The Great Inflation.”

The lesson for us is that once these overly broad and irresponsible COVID-19 lockdowns are over, the supply chain crisis will resolve, and cost-push inflation will dissipate. But inflation driven by an egregious expansion of the money supply will still be with us if measures aren’t taken to deal with it. Many of us remember James Carville, the incorrigible mastermind behind Bill Clinton’s successful 1992 campaign for the Presidency, who promoted his candidate with the slogan “It’s the economy, stupid!” We can refine that when it comes to the issue of inflation: “It’s the money supply, stupid!” The money supply is the prime player, the one thing that really matters.

This much said, though cost-push inflation will go away when supply chain issues are resolved, it’s going to be with us for a while. In dealing with it and planning beyond it, we need to take a look at how government mismanagement of the pandemic created the crisis along with what changes could and perhaps should come about as a result. We will undertake this task in the second installment in this series.

Why Governments Like Inflation

Expansion of the money supply, and thus inflation, is produced by governments. While this happens in multiple countries for similar reasons, in the United States in particular, it has happened over the course of the last century primarily for three inter-related reasons: (1) rapid growth in government spending; (2) the attempt to create jobs and reduce unemployment; and (3) the attempt by the Fed to manage the money supply and interest rates simultaneously in ways that are inconsistent with controlling inflation.

Government spending doesn’t lead to rapid growth in the money supply and inflation if it is financed by taxation, which allows increased government spending at the cost of less private spending on consumption or investment, or by raising interest rates, which also diverts funds from private uses by making it more difficult for businesses to borrow money or individuals to get mortgages. Needless to say, neither of these approaches is politically attractive, so governments who want to spend more generally do so just by creating more money. This is absolutely inflationary, but it allows members of Congress to spend on their pet projects, buy off political threats, and give placating goodies to their constituents without straightforwardly making them pay for it through raised taxes or interest rates. The inflation that results functions as a hidden tax.

Government also looks good when unemployment is low, so “full employment” is an attractive goal and a useful political mantra. It’s also an ambiguous proposition. The modern world is always changing, with new products appearing and old ones disappearing so the forces of supply and demand endlessly shift. In this environment, ceaseless innovation constantly alters methods of production, and labor mobility is essential. Individuals changing jobs, however, will generally be unemployed for a time in between. Young people entering the work force also take time to find their niche and may experiment with different jobs. Further complications in the labor market are added by minimum wage laws, trade union restrictions, part-time workers, and so on. How does one decide, with a given population in an ever-changing world, what the number of employed people should be that corresponds to full employment?

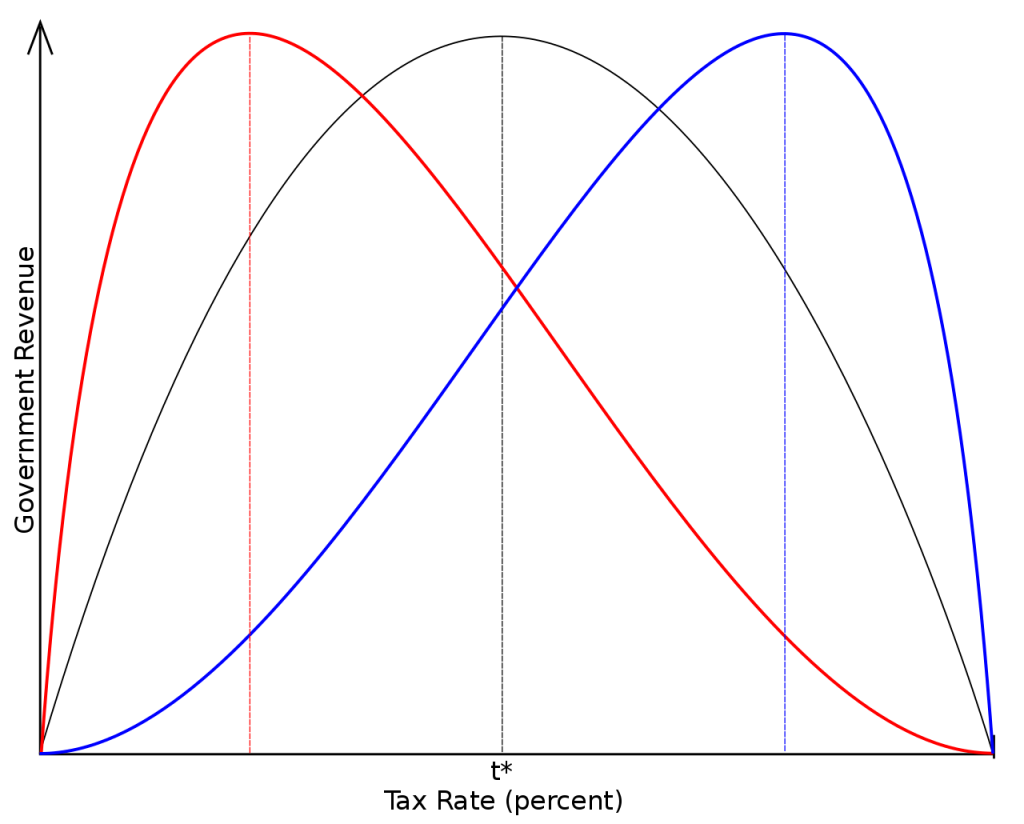

Against this ambiguous and ever-shifting background, government seeks to act in a way that can be represented as reducing unemployment. To this end, government spending can be portrayed as adding to employment, as can lowering taxes. While lowering taxes can actually lead to more tax revenue, as the Laffer Curve illustrates, this only works up to a point. Trying to look good by repeatedly invoking strategies of increased spending and reduced taxes will inevitably expand the money supply and cause inflation. If the Fed creates money by buying government bonds, enabling private banks to increase the volume of private loans to businesses and individuals, this can also be represented as creating jobs, and it also creates inflation. In short, under pressure to take action that can be represented as creating jobs, government fiscal policy and the Fed’s monetary policy both create inflation.

Lastly, the Fed has the power to grow or shrink the money supply and it also has the power to set interest rates. To function in a manner that controls inflation, when it expands the money supply, it should also raise interest rates, and when it contracts the money supply, it should lower interest rates. This is not what the Fed has been doing. Not only has it been keeping the interest rate artificially low for a long time, for the last two years it has purchased treasuries like they’re going out of style, thus vastly expanding the money supply. Both of these actions are inflationary, so guess what we’re seeing? Inflation. As Gomer Pyle would have said, “Soo-prise, soo-prise, soo-prise.”

It should be obvious why the government likes to increase the money supply: it is a way of bestowing government largesse on the plebes while denying there’s any real cost. Let’s pour tons of money into infrastructure, they say, give everyone a stimulus check, and build back better. Indeed, this is what modern monetary theorists are selling, and they’re having an undue influence in the corridors of power because politicians love the idea of a free lunch with an unlimited prospect for buying votes. A wise quote of obscure attribution is relevant here: “A democracy cannot exist as a permanent form of government. It can only exist until the voters discover that they can vote themselves largesse from the public treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the public treasury with the result that a democracy always collapses over loose fiscal policy…”.

The reasons that governments expand the money supply are no mystery. But why would governments, while wringing their hands and acting surprised, actually like the inflation that inevitably results from increasing in the money supply? There are two primary reasons: (1) Inflation functions like a tax that fills the government coffers, but it’s not imposed by raising the tax rate, so it has better optics; and (2) Inflation allows the government to pay off its debts with money it has created out of thin air and without cost to itself, and that money has less value than it did when the debt was incurred. Let’s consider these reasons in turn.

How does inflation function as a hidden tax? One way this happens is that as prices go up, salaries also go up, increasing the amount of tax people pay even though, due to inflation, the person has not seen an increase in real income, because the new higher salary has the same purchasing power as the old salary. For instance, if the standard deduction on tax forms does not increase proportionally with inflation, more of a person’s income will be taxable even though salaries that merely keep up with inflation don’t create more buying power. In fact, any raise at all, even if it doesn’t keep up with the cost of living, leaves the government with more money in its coffers and the individual taxpayer worse off in an inflationary economy. Furthermore, if there is a state and (as in Canada) federal sales tax, then a 10% rise in the price of goods and services gives the government 10% more sales tax revenue every time a consumer buys something. Lastly, far be it from municipal governments to miss out on the windfall—as home values increase, even property taxes will rise accordingly. The bottom line is that inflation always gives the government more tax revenue.

The other aspect of this situation is that it allows the government to pay its debtors with money that has less worth than when the loan was taken. Suppose the government borrows money by selling bonds to the private sector that it promises to pay back with 2% interest per year at maturity. Now suppose the government induces inflation by increasing the money supply, the inflation rate goes to 10%, government tax revenue increases proportionally to inflation, and the currency is worth less (has less purchasing power per dollar). The bond holders who loaned money to the government are left holding the bag. The government still only has to pay back the money it borrowed at an interest rate of 2% per year, but the real monetary value of the bonds has declined by 10%, and the government gets to pay back the debt with 2% interest while it’s making 10% more in taxes—a great deal for the government, while the private sector takes it on the chin.

The Destructive Power of Inflation

I begin by quoting again from John Maynard Keynes’s The Economic Consequences of the Peace (1920): “Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate,but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth” (1920, p.235). In short, rampant inflation is a significant threat to a nation’s economic and political order.

But wait, you say, inflation isn’t all bad. As Keynes points out, it does help some people. All right, let’s take stock of who it helps. It helps those who own real estate and those who have fixed-rate mortgages, at least where these investments are concerned. Property values go up and equity in homes increases for those who have fixed-rate mortgages and won’t have to pay more to continue living where they do. Owners of rental properties have license to increase the rent that they charge in proportion with inflation. Those who borrowed at a fixed rate before inflation hit can pay their loans back with money that’s worth less than when it was borrowed, so these individuals get the same benefit as the government on their borrowed money.

Another benefit for those with money to invest is the higher interest rates available after inflation has taken root. For instance, in the early 1980s when inflation was rampant, Canadian investors could get guaranteed investment certificates for a specified term from a trust company or a bank that were guaranteed to return 100% of the original investment at a fixed rate of interest per year that peaked around 19.5%. How often do you get a no-risk investment that provides that kind of return?

A final potential benefit is reduced unemployment if the assumptions governing the Phillips Curve apply, though this requires that consumers spend more and more jobs get created. If people are spending more because they’re worried that the value of the dollar is decreasing and they want to make purchases before their money loses even more value, then the velocity of money will increase and induce even more inflation, but companies will generate more revenue and, so the reasoning goes, be able to hire more people. If consumers don’t spend more because they’re balking at higher prices and trying to find other ways of coping with inflation, stagflation will result, unemployment will remain a problem or get worse, and an economic recession will accompany price inflation. This happened in the 1970s and early 1980s and it seems likely to happen again in the current environment.

- Record Number of Americans Leave the Job Market in December 2021

- January 2022 Jobs Report Looking Dismal

Given that a significant reduction in unemployment is unlikely, what can we say about those who will benefit from inflation? They are property owners and people who have money to invest. In other words, the people who benefit from inflation are those who are already doing well enough to own their own homes, meet their expenses, and have money left over to invest. If you’re not in this situation, you’re basically up the creek without a paddle. Let’s take stock of the inflation losers.

If you are retired or otherwise living on a fixed income and inflation is rampant, you are losing more and more of your buying power every year. If you have money in low-interest savings accounts or government bonds, they are progressively decreasing in value due to inflation. If you are working and your raise each year does not keep up with the rise in cost of living, you are losing buying power year after year. Furthermore, as we have discussed, if you are receiving a raise and the tax income brackets are not being adjusted for inflation, you’re paying more in taxes as a result of inflation. You are also, due to inflation, paying more in property tax as your home value increases, and more in sales tax for the same things you always buy as the result of cost increases in goods and services.

It gets worse. What if you’re in the market for a new home? Housing prices are skyrocketing putting the kind of home you want—or maybe any house at all—completely out of reach. But even if you can afford a home at the inflated prices, interest rates will be higher too, meaning that the interest on your mortgage payments could be exorbitant. For instance, back in the early 1981, at the height of stagflation, the average mortgage interest rate across the United States was 16.63%. What is more, for those who have substantial credit card debt, the already criminal rates of interest charged by credit card companies head further into the stratosphere. And if you were unwise enough to get an adjustable-rate mortgage on your home before inflation and higher interest rates hit, your monthly mortgage payments may increase to the point where you have to sell your home. If this happens and you’re actually able to sell your home, while you may take some consolation in being able to pocket the extra cash from inflated home prices, you’ll also find yourself having to pay inflated rents. Renters really get taken to the cleaners in an inflationary economy.

Inflation is ultimately a straightforward confiscation of private wealth. The real value of much that is privately owned, from savings and pensions, to bonds and insurance policies, depreciates correspondingly with the purchasing power of the currency, even as government revenues increase by a proportionate measure. It is clandestine theft, silently transferring wealth from the private to the public sector. And it creates great uncertainty. In our current inflationary environment, compounded by ever-changing governmental responses to the pandemic, neither individuals nor corporations have a clear path forward.

For individuals, there is ongoing uncertainty about the future of their employment, the stability of their income, the value of their savings and investments, the future of the dollar, what they will continue to be able to afford, and how they should currently spend or conserve their financial resources. Caveat emptor. For corporations, there is uncertainty about production costs and their ability to maintain their work force, uncertainty about who will continue to buy their products as they are forced to raise their prices, and what sorts of changes will have to be made if their business is to remain financially solvent.

All this economic uncertainty begets tentativeness and chaos as both individuals and corporations struggle to decide what to do protect their financial well-being against the unpredictable effects and destructive power of the Godzilla of inflation.

The Fix: What We Can Expect If Government Comes to Its Senses

The Fed has finally awakened to the inevitability of systemic and lasting inflation. The Federal Reserve will be reducing its Treasury bond holdings, which will contract the money supply, and this will be accompanied by incrementally rising interest rates over the next couple of years. Doing this will cause pain, but there is no painless path out of our current predicament.

- The End of Free Lunch Economics

- Fed Looking to Reduce Bond Holdings

- Fed to Raise Interest Rates Three Times in 2022 to Tame Inflation

These moves are exactly the ones the Fed should be making, and making aggressively, if inflation is going to be reduced and eventually stopped with a lag time on the same order as that on which it started and has been increasing after the wanton expansion of the money supply. We will discuss the details of this and how to mitigate some of the painful effects momentarily, but we need to start with things the government should not do, even though it will be tempted to do them.

Not Price Controls

As inflation threatened to take hold in the early 1970s, President Nixon decided as a pre-emptive strike to institute wage and price controls. The Economic Stabilization Act of 1970, which conferred on him the power to do so, proved to be an unmitigated disaster. Ranchers stopped shipping their cattle to market, farmers drown their chickens because they couldn’t afford to feed them at the prices they were allowed to sell them, myriad other things went awry, and inflation broke out anyway.

Still, there are economic know-nothings out there suggesting that price controls are a good idea and superior to monetary policy as a means of controlling inflation. They are not. As if the lessons of the 1970s weren’t enough, let’s briefly review the basic economic facts that explain why price controls do not work: imposing price floors and, as would be proposed by a government attempt to inhibit inflation, price ceilings, would prevent the market from adjusting the equilibrium price and quantity, skewing the forces of demand and supply, and in the case of price ceilings, creating shortages of goods that induce further inflationary pressures. If suppliers cannot afford to provide goods at the price level set by government, they will simply reduce the amount produced or eliminate production altogether. Meanwhile, consumers are still demanding the good in question while supply is being reduced, so massive shortages are created. This is how government turns the specter of bread lines into reality. To meet the demand, black markets are created where the goods are then sold at illegal prices, usually far above what inflation and market forces would have dictated if government had stayed out of the picture. Imposing price controls is the pinnacle of economic ignorance and a poster child for George Santayana‘s remark that “those who cannot remember the past are doomed to repeat it.”

Not Raising Taxes or Instituting a Wealth Tax

The common wisdom among those who think that filling the government coffers by taxing anything and everything is a good idea, is that reducing the amount of disposable and investable income for individual households through taxation will reduce inflation by reducing both the amount of money in circulation and the demand for goods—as long as the government does not increase its own spending as a result (yeah, right). As we saw earlier, this is a primary strategy proposed by modern monetary theorists for addressing inflation, and while it quite actively lowers everyone’s standard of living and breeds discontent, the rationale is clear enough. Given that every solution to systemic inflation is painful, however, we need to take a closer look at this approach.

As far as raising taxes on corporations is concerned, however, this idea is even more problematic. Taking revenue from corporations that might otherwise be reinvested in their businesses will lower their productivity, create unemployment, and reduce the supply of goods produced in relation to demand, something more conducive to stagflation than reducing inflation. It’s not a viable solution to the problem.

What should we make, then, of the proposal to increase income taxes on private households and sales taxes on consumption to curb demand and reduce inflation? We have spoken about the effects on demand when taxes are raised to combat inflation, but what about other consequences further down the causal chain? While having less disposable income or having to pay more in sales tax will reduce demand and have a deflationary effect, the longer-term effect on prices is far from certain.

If taxation induces a cost-of-living increase and standard-of-living decrease when wages remain constant, it is reasonable to suppose that wage negotiations will focus on neutralizing the tax increase or exceeding it, catalyzing a wage-tax spiral. Studies of wage negotiation in industrialized countries provide evidence for tax-driven bargaining strategies that have led to some governments lowering their taxation rates to moderate wage increase demands. Furthermore, econometric studies focused on the relation between taxation and wages in the United States, Canada, the United Kingdom, and the Netherlands have shown similar correlations. The bottom line is that raising taxes, while having an initial deflationary effect, induces wage negotiations to restore purchasing power that neutralize this effect, so that raising taxes is not, in the long run, an effective means of addressing inflation.

But maybe we should just impose a wealth tax on the ultra-rich—might that have a deflationary effect without adversely affecting the middle and lower classes? Let’s define the concept first: a wealth tax, most often, is levied as an annual tax on the net worth of an individual (or sometimes a corporation) above a certain exemption threshold. It is imposed in addition to any income tax, sales tax, or other existing form of taxation. Might this work to exert deflationary pressure? We need to examine the consequences.

Aside from problems of fair valuation and of unintended consequences for families that have inherited property that has increased in value so much that they could not afford to pay a wealth tax on it without selling it, the disincentives created would cause the burden of the tax to metastasize throughout the whole economy. It would also force a huge regulatory expansion of the IRS to deal with compliance. As argued by economists Douglas Holtz-Eakin and Gordon Gray, a wealth tax of the sort proposed by Elizabeth Warren or Bernie Sanders, for example, would result in the collective imposition of an effective tax of 63 cents on average workers for every dollar of revenue raised and, measured in 2018 dollars, shrink the gross domestic product (GDP) by $1.1 trillion during the first ten years, with a further reduction of $283 billion each successive year. Given a GDP of $21 trillion (in 2018), the erosive effects of the wealth tax on the American economy would advance at an alarming rate. While these effects are certainly deflationary, their overall deleterious character militates against the imposition of a wealth tax as a strategy for fighting inflation, quite aside from its mitigated efficacy in light of the wage-price spiral it would induce.

Measures to Slow the Rate of Monetary Growth

We turn, then, from incomes and fiscal policy to monetary policy as the most effective response to inflation. We have come to a clear understanding that inflation is a monetary phenomenon and that an increase in the quantity of money without a corresponding increase in output is the central cause of inflation; everything else is subsidiary. Similarly, if we seek to cure inflation, the primary strategy must be a reduction in the rate of monetary growth, every other approach is just window dressing. Furthermore, just as it took the better part of two years for substantial inflation to develop, so it will take an equal amount of time exercising monetary restraint before inflation-reducing effects are evident, and this time will not be pleasant, because the cure for inflation has some painful side effects.

Selling Treasuries to the Banks

The Federal Reserve has traditionally used three means of controlling the money supply: setting the reserve requirements for private banks in the fractional-reserve system, setting the discount rate specifying the interest that Reserve Banks charge any eligible financial institution for borrowing funds on a short-term basis, and lastly, conducting open market operations.

Since banks operate as close to the required reserve limit as possible, by raising or lowering the reserve requirements, the Fed can influence how much money banks are able to loan, thus affecting the size of the money supply. Implementing monetary policy goals by this means is uncommon, however.

If a bank is at risk of falling short of having the required reserves, it may borrow money overnight from other banks, which loan it money at the federal funds rate. The demand for reserves is normally very stable and this allows the Fed to influence the federal funds rate by changing the supply of reserves through open market operations. In rare cases where borrowing is disrupted and other banks in the system are unable to provide the needed reserves, the Fed becomes the lender of last resort, lending money to banks at the discount rate, which is set above the federal funds rate targeted by the Fed in its open market operations. Changes in the federal funds rate induce similar changes in other short-term interest rates, which affects the cost of borrowing for individuals and businesses, thus increasing or decreasing the total amount of money and credit in the economy, ultimately affecting the inflation rate and employment levels.

Finally, the Federal Reserve can expand or reduce the money supply by buying or selling treasuries on the open market, which in turn will affect interest rates. When the Fed conducts these open market operations, the money supply will either expand or contract depending on whether treasuries are purchased or sold, respectively. When the Fed purchases bonds on the open market from banks with money that it creates, this injects money into the banking system, thus increasing the money supply. When money is easily obtainable, interest rates will be lower. To contract the money supply as a means of controlling inflation, the Fed sells treasuries to the banks, which takes money out of the financial system as individuals buy these securities out of their bank accounts, thus reducing the money supply and putting upward pressure on interest rates as money becomes more scarce.

The familiarity of the public with these secretive operations of the Fed increased markedly after the financial crisis of 2007-2008 induced by the subprime mortgage crisis and the burst of the housing bubble. To address the economic recession catalyzed by this financial crisis, the Fed pursued a policy of quantitative easing by purchasing longer-term treasuries and, in particular, boatloads of mortgage-backed securities, to increase the domestic money supply, provide private banks with more liquidity, lower the federal funds rate to near zero, and encourage lending and business investment throughout the economy. The Fed also adopted a policy of forward guidance to inform the public of its likely actions and the schedule on which they will be implemented so as to allow the economy to anticipate and adjust gradually to the implementation of policies being pursued.

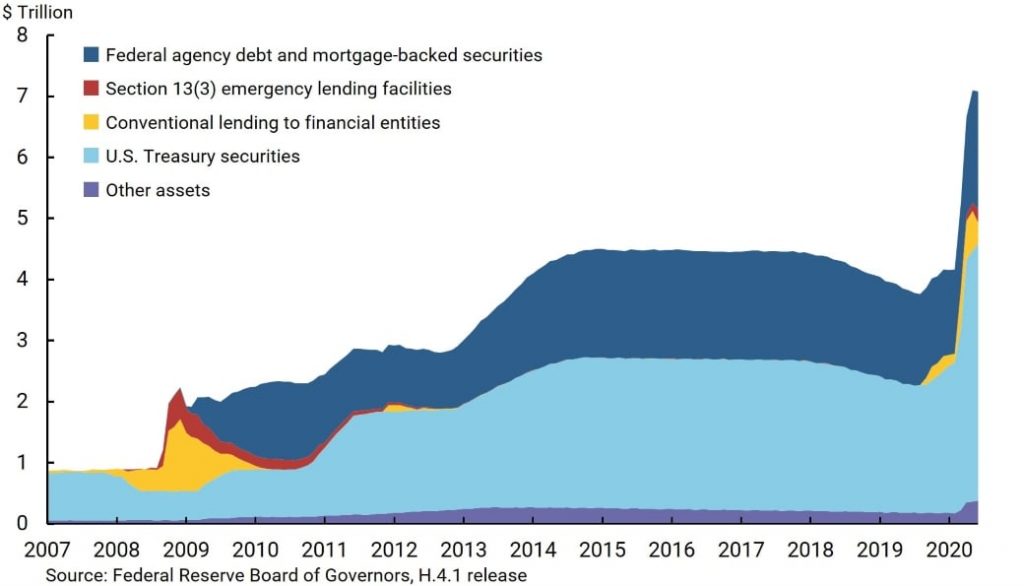

The Fed tried to ameliorate the effects on business and employment of the government lockdowns invoked as a response to the Covid-19 pandemic by using the full range of its monetary policy tools and then some, thus adding trillions of dollars to its balance sheets and vastly expanding the money supply. The traditional tools it employed in an effort to maintain the flow of credit to households and businesses were lowering the target for the federal funds rate to near zero (it was already very low) and then encouraging commercial banks to borrow through the discount window by lowering the discount rate and extending the length of time for paying back loans. In addition to these traditional approaches, the Fed also assisted the government’s “financial assistance” efforts by purchasing huge amounts of treasuries and mortgage-backed securities, creating the money necessary for the U.S. Treasury to be able to issue checks to private households, and then created lending facilities under the rubric of its emergency lending authority with an even broader mandate than the one established for the 2007-2008 financial crisis.

- The Fed has Absorbed Almost All the New COVID Debt

- The Federal Reserve’s Current Balance Sheet (Redux) – Close to $9 Trillion as of Mid-February 2022

Image Credit: Federal Reserve Bank of San Francisco

The Current Balance is Close to $9 Trillion

The result of these expansionary policies was to be expected and is now quite evident: INFLATION. Given that this was the predictable result, the inevitable question is whether these government actions, assisted by the Fed, were necessary, because they not only induced monetary inflation, they induced temporary cost-push inflation through the supply-chain shock resulting from the lockdowns the government mandated as a response to the pandemic. This topic will be taken up the next installment of this series: Pandemic Mismanagement, Supply-Chain Crises, and Cost-Push Inflation.

And the solution to inflation is to reverse the monetary actions that got us here. Rather than buying treasuries and increasing the money supply, the Fed needs to contract the money supply by selling its treasuries and mortgage-backed securities, thus reducing its holdings and pulling back the money it artificially injected into the financial system. Doing this will not have an immediate effect. Much like it took inflation the better part of two years to be set loose, it will take a similar amount of time to be reined in and tamed. Thankfully, the Fed is considering such action now. The sooner it undertakes it, the better.

That this approach is effective and will do what it is intended to do is clear from the example of the Confederacy discussed above and from the effectiveness of Volcker’s actions as Chair of the Fed in the 1980s. It is also evident from what Japan did to tame inflation in the 1970s. The Japanese money supply began growing at increasingly higher rates in 1971 and was topping 25% per year by mid-1973. Lagging behind the increased money supply by several months was a dramatic rise in inflation. This led the Japanese to change their monetary policy in 1973, shifting from a focus on the external value of the yen to its internal value and on reducing monetary growth. With minor exceptions, Japan kept the brakes on monetary growth for five years. Around 18 months after monetary growth started declining, inflation followed did the same, but it took two more years before it dropped into the single digits, where it held constant for two more years before heading toward zero. Of course, Japan experienced lower growth and higher unemployment after it slowed monetary growth, particularly in 1974, but then output began to recover and settle into a very respectable growth rate of about 5% per year. Furthermore, Japan did this without invoking wage and price controls and in the midst of enduring higher crude oil prices. Would that the United States had done the same, but we didn’t learn the lesson until the 1980s.

Higher Interest Rates

A reduction in the money supply will inevitably be accompanied by rising interest rates and vice-versa. As money becomes less plentiful, its value increases, as does the cost of borrowing it. Higher interest rates on other assets also make it less profitable to hold money when investment in these alternatives would yield a higher rate of return.

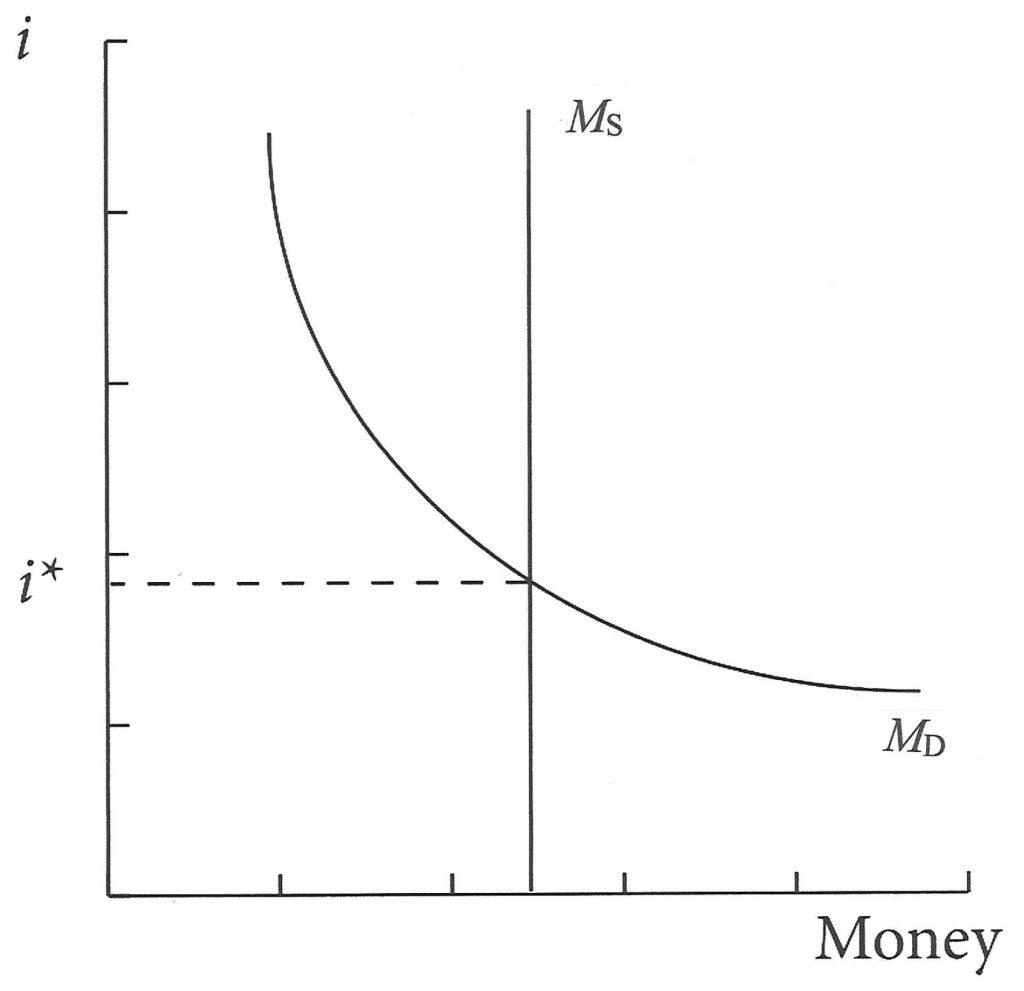

Since inflation erodes the value of loan repayments, as discussed above, economists distinguish between nominal and real interest rates. The nominal interest rate is simply the rate of return in terms of the money borrowed versus the money returned. Real interest rates, however, compensate for inflation by measuring how much stuff you can buy with what is borrowed versus how much stuff you can buy with what is returned. The theoretical value of the nominal interest rate i* is determined by the intersection of the money demand curve MD with the money supply curve MS, as represented in the graph below.

of the Money Supply MS and Money Demand MD Curves

The graph shows the equilibrium nominal interest rate as determined by the money supply function, MS, which is inelastic with respect to the interest rate and hence is represented as a vertical line, and the demand for money, MD, which is a function of the interest rate. As is evident from the downward slope of the money demand curve, the higher the interest rate, the less money people wish to hold. Holding cash, while great for its liquidity, is nonetheless a very bad place to park your wealth when higher interest rates are available in other assets. The interest rate, i*, is the equilibrium interest rate because it is the only one at which the number of dollars that people wish to hold equals the total number of dollars put in circulation by the government. The equilibrium is stable in that deviation from it will be pushed back to it by market forces.

All of this helps us understand why monetary policy works. Interest rates adjust in response to the money supply to get people to hold whatever quantity of money is made available by the government. Let’s talk about treasury bonds in this regard for a moment, because the bond market determines the interest rates.

A bond is a financial asset for which you pay a certain amount of money right now in exchange for a series of payments in the future. These can come as face-value payments, where the value of the bond is printed on the face of the bond certificate and is payable when the bond expires, or as coupon payments that are typically made twice a year until the bond expires (these received their name before computerized records because bond owners would clip off a coupon on the bottom of the bond certificate and mail it in for payment). These treasuries typically expire after 1, 5, 10, or 20 years, but they do not guarantee a rate of return since the rate of return on a bond depends on how much you pay for it right now. For example, if you buy a 1-year zero-coupon $100 dollar bond for $90 right now, then your return in one year will be about a little over 11 percent. Note that since the amount of money you get in the future is always fixed for bonds, the rate of return on a bond varies inversely with how much you pay for it. Higher bond prices mean lower yields and lower bond prices mean higher yields. The price of treasuries thus varies inversely with the interest rate, and recognition of this fact gives the government a very useful monetary policy tool.

Suppose now that the Fed wants to stem inflation. It can initiate the following chain of events:

- It sells treasuries to reduce the money supply,

- The decreased money supply causes interest rates to rise as the price of treasuries falls.

- Individuals and businesses respond to the higher interest rates by taking out fewer loans and reducing their consumption of goods.

The effect of this is to reduce both demand and output, putting a downward pressure on prices that helps to alleviate inflation. Fear of inflation by individuals and businesses also aids this process because inflationary edginess creates the expectation that more cash will be needed to buy things at higher prices, and this creates a demand for money that also drives up interest rates.

Using forward guidance to galvanize anticipatory activity that will smooth out the response to its actions, the Fed has signaled that there will be interest rate increases in March 2022 followed by a reduction of the assets on its balance sheets. In other words, we can expect bond prices to fall, the money supply to shrink, and interest rates to rise. All of this is necessary if inflation is to be halted, but these policy measures will need to be held in place and for a good length of time before the results will be manifest.

Rising interest rates will mean falling bond prices, so the Fed is going to get soaked on the assets it sells—not that it really cares about paper losses in respect of money that it can create at will—but, and here’s the kicker, the government treasuries still have to be paid off when they come due, and an increase in interest rates makes it more difficult for the government to pay its own debts. The federal government has about $22 trillion in debt held by the public on which it paid about $413 billion in interest last year. If interest rates rise, so will the interest payments, and the intractability of all this will only get worse if Congress succeeds in passing the multi-trillion dollar reconciliation and infrastructure bills (thankfully, this seems unlikely).

These aren’t the biggest problems right now, though: much more worrisome is the payment schedule, since 43% of this debt comes due over the next two years. How will the government avoid defaulting? Undoubtedly, by issuing new bonds to pay off the old ones as part of a huge governmental Ponzi scheme. It’s not as though the world will shun American debt, however, despite our staggering fiscal irresponsibility, because much of the rest of the world is in the same predicament. The choice is between American debt and French debt and British debt and Brazilian debt and Canadian debt and Chinese debt and… the list goes on. So it is unlikely that the world will single out American securities as the ones to avoid. The fact remains, however, that this trajectory is not sustainable for America or for the world, and sooner or later, the whole Ponzi scheme will come down like a house of cards—just like it did for Bernie Madoff—if we don’t get our finances in order.

The Man Who Made Off with the Money

The Side Effects and Their Mitigation

Everything comes at a cost, and that includes the mitigation of inflation’s destructive power.The inevitable and painful side effects of ending inflation will be much slower growth and higher unemployment. Because of this, it’s important to emphasize why these side-effects occur, and what might be done to ease them. The reduction in spending that comes from the Fed selling its assets is inevitably interpreted in the broader economy as a reduction in the aggregate demand for the things being produced, and this, after a lapse of time, leads to a reduction in output. The reduction in output means that fewer workers are required and this leads to a reduction in employment. Once these painful changes have been assimilated into the economy, after another length of time, inflation slows.